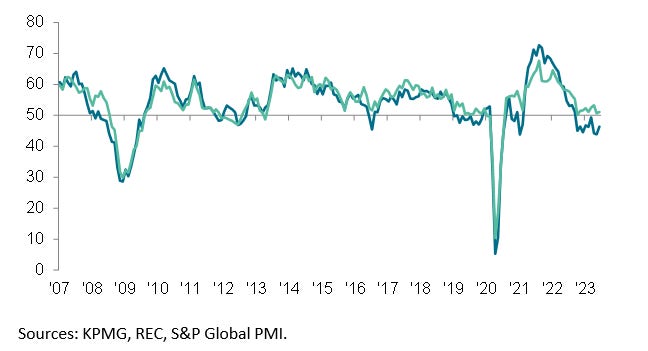

Candidate supply rises rapidly in June

The hiring slowdown and company layoffs impacted staff availability, which rose for the fourth straight month in June. Moreover, the latest upturn in overall candidate numbers was the sharpest recorded since December 2020, with both permanent and temporary staff supply expanding at accelerated rates.

Starting pay increases at softest rate since April 2021

Latest data revealed further marked increases in both starting salaries and temp pay at the end of the second quarter. Panel members frequently mentioned that the rising cost of living and competition for skilled staff had pushed up starting salaries and temp wages. That said, remuneration for both permanent and temporary staff rose at the slowest rates for over two years in June.

Continued…

Vacancy growth eases to 28-month low

Overall vacancies continued to rise in June, but the pace of expansion softened for the fourth month in a row. Furthermore, the rate of growth was the softest recorded since the current sequence of rising staff demand began in March 2021. Underlying data indicated that a slower uptick in permanent vacancies offset a quicker rise in demand for short-term staff.

Regional and Sector Variations

Permanent placements fell across all four monitored English regions bar the North of England in June, which registered the first upturn since February.

London saw the steepest increase in temp billings of all four monitored English areas. The North was the only region to register a decline.

Demand for workers continued to rise across both the private and public sectors at the end of the second quarter. Stronger rates of vacancy growth were seen across the board compared to May, with the exception of permanent roles in the private sector. Notably, the latter saw the softest rate of expansion since February 2021. Meanwhile, the strongest rise in demand was signalled for permanent public sector staff.

Permanent staff vacancies expanded in eight of the ten job categories monitored by the survey in June. The steepest increases in demand were seen for Hotel & Catering and Blue Collar. Job openings meanwhile fell in the IT & Computing and Retail sectors.

The majority of monitored sectors recorded greater demand for temp workers during June, led by Hotel & Catering by a wide margin. IT & Computing and Construction were the only job categories to register lower vacancies for short-term workers.

Comments

Commenting on the latest survey results, Claire Warnes, Partner, Skills and Productivity at KPMG UK, said:

“The sharp upturn in candidate availability this month – the highest for two and a half years – is a big concern for the economy reflecting the effects of a sustained slowdown in recruitment along with increasing redundancies across many sectors.

“Employers are also tending towards temporary hires, given lingering economic uncertainty. And yet, the labour market remains reasonably resilient, with notable demand for skilled workers, both permanent and temporary, across a multitude of sectors this month.

“The evident mismatch between open vacancies and the skills of available candidates needs to be addressed urgently and a concerted focus on upskilling and reskilling is long overdue.”

Neil Carberry, REC Chief Executive, said:

“There is a risk of seeing an element of Groundhog Day in June hiring, with permanent billing easing again and firms still turning to temporary staff in the face of uncertainty. But there was quite a lot of change in the shadows of the headline data. There was a significant step up in the number of candidates looking for a new permanent or temporary role. This is likely driven by people reacting to high inflation by stepping up their job search, and by some firms reshaping their businesses in a period of low growth. It’s no surprise, therefore that the rate at which wages are rising has dropped again.

“Despite these trends, the labour market remains very tight. There are still broad skills shortages, with accountancy, construction, teaching and nursing among those sectors struggling to find and retain workers. This is despite the supply of candidates across the job market having risen for four consecutive months. Earlier this month, the government published its first ever NHS Workforce Plan, which acknowledges significant staffing issues while not getting to grips with the NHS being really bad at building partnerships with staffing partners such as agencies.

“The growth in vacancies for temps and permanent staff in hotel & catering and blue-collar jobs, and for temp positions in retail, suggest businesses anticipate that people are still prepared to spend their wages on goods and services despite the fall in their purchasing power and the wider cost-of-living crisis. This is backed by anecdotes from REC members noting that the warm weather in June was a significant driver of demand.

“Long-term progress rests on the UK being a great place to invest. A strong industrial strategy with people at its heart would help overcome labour and skills shortages, acknowledging the wide range of choices that people have about how they work. Progress should start with action on skills and immigration, but also accelerating steps on childcare, transport and back-to-work support, as set out in the REC’s Overcoming Shortages report.”