KPMG recently conducted a research of the six main locations for Shared Service Centres (SSC) in India (Mumbai, Pune, Bengaluru, Dehli/NCR, Chennai, and Hyderabad) and profiles their suitability and potential for future SSCs based on a range of factors. Key factors influencing the business environment in cities have been investigated, such as the cost of labour, supply of technology and finance talent, degree of saturation, attrition rate, unemployment rate and overall economic growth. This assessment aims provide a holistic view over the strengths and weaknesses of each location, identifying mature, well-established locations as well as up-and-coming locations with great potential in the future.

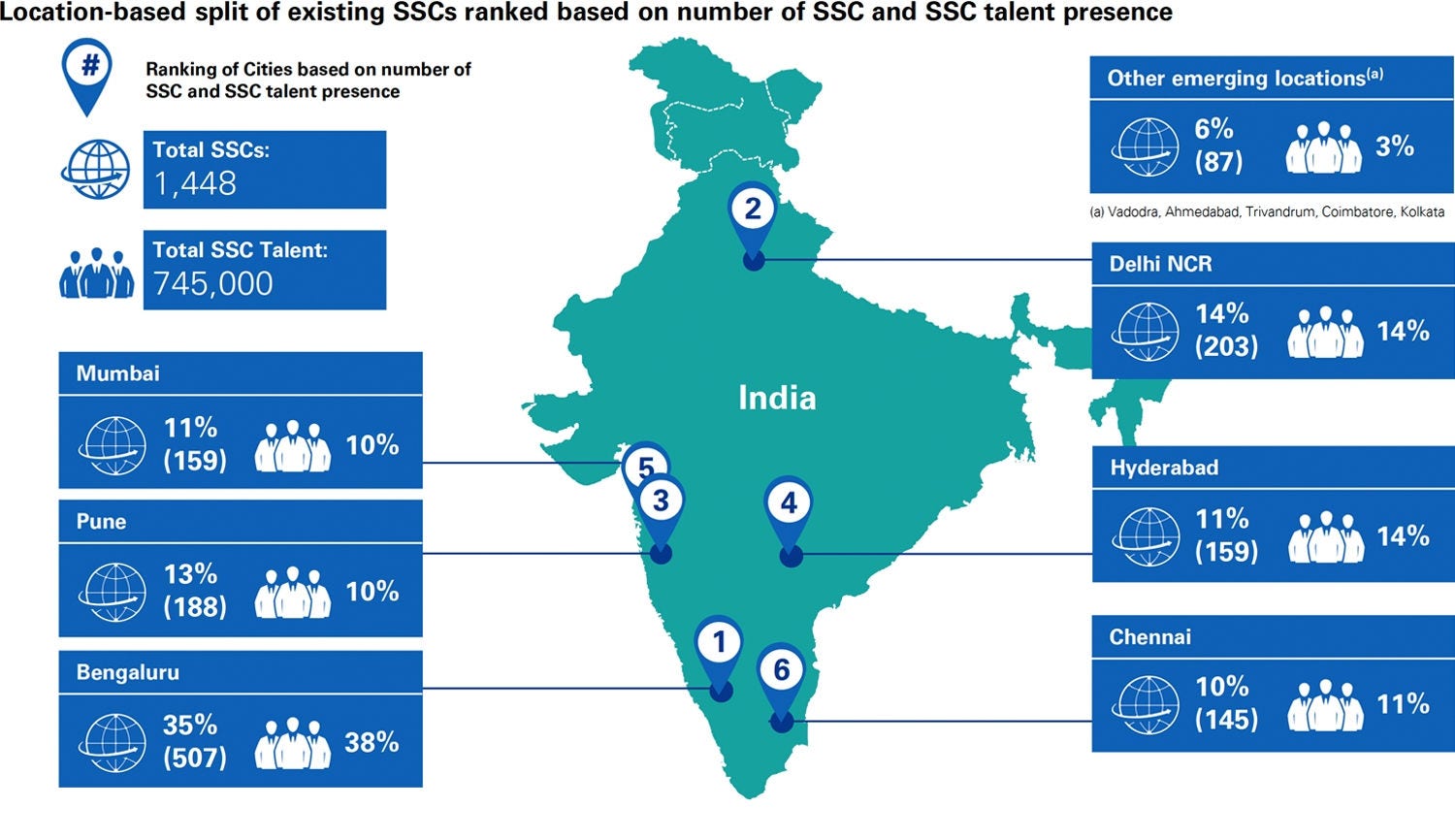

First of all, let us take a look at the existing SSCs. Bengaluru has the highest rate number of SSCs (35 percent) and the largest pool of talent (38 percent). It is traditionally dominated by IT industry, but it is becoming an increasingly popular destination for global in-house solution centres. This is because Bengaluru has established itself as the finance and IT talent hub of India, with a plethora of ranked higher education institutes, generating large numbers of high-quality finance and technology talents every year.

Regional Deep-dive

Bengaluru

- Bengaluru has 13 special economic zones –hosting a variety of companies from various sectors. As per Zinnov, a consulting firm, Bengaluru is a preferred location for shared service centres, especially IT.

- Major BFSI players with FP&A SSCs in Bengaluru: ANZ, AXA, Societe Generale, Swiss Re, Morgan Stanley, HSBC, and Goldman Sachs.

Pune

- Pune recorded a growth of 5 percent among financial professionals in 2016.

- Home to Finance KPOs of SG Analytics, Reval Analytics, Eclerx, Syntel, CRISIL, Credit Pointe, Verve, Value Notes, BNY Mellon, WNS and Algo Analytics.

- Major BFSI players with FP&A SSCs in Pune: Credit Suisse, Swiss Re, Bank of New York Mellon, UBS, and Barclays.

Mumbai

- Employment activity in Mumbai has largely remained positive with strong demand from some sectors, such as financial services.

- Mumbai is still very much India’s economic capital, retaining stability and resilience amid economic flux with many international financial service conglomerates continuing to build headquarters in the city.

- Major BFSI players with FP&A SSCs in Mumbai : UBS, Barclays, Prudential, Deutsche Bank, BNP Paribas, and Citi bank.

Delhi NCR

- In 2016, 12 percent increase in finance professionals was recorded in Gurgaon.

- In recent years, Delhi/ NCR has seen an increase in talent demand in shared services as more MNCs are diversifying their operations to the region, a trend driven by its strong global connectivity and its competitive infrastructure costs.

- Major BFSI players with FP&A SSCs in Delhi NCR: ABN AmroBank, Metlife, Ameriprise, Fidelity International, XL Insurance, HSBC, and Steria.

Hyderabad

- Hyderabad is the capital of relatively new Indian state, Telangana, and is considered as the fastest emerging IT/ITES hub in the country.

- The city enjoys the benefit of lowest employment cost.

- Future supply of finance talent is likely to be adequate with partnerships such as that of Bombay Stock Exchange Limited (BSE), and Telangana Academy for Skill and Knowledge (TASK) to set up a finance centre of excellence.

Chennai

- The capital has abundant and highly skilled labour force; it is politically stable with negligible cases of labour unrest.

- Chennai’s economy primarily banks on technology industry, along with automobile, healthcare and hardware manufacturing industries.

- Major BFSI players with FP&A SSCs in Chennai: Barclays, Standard Chartered, HSBC, and World Bank.

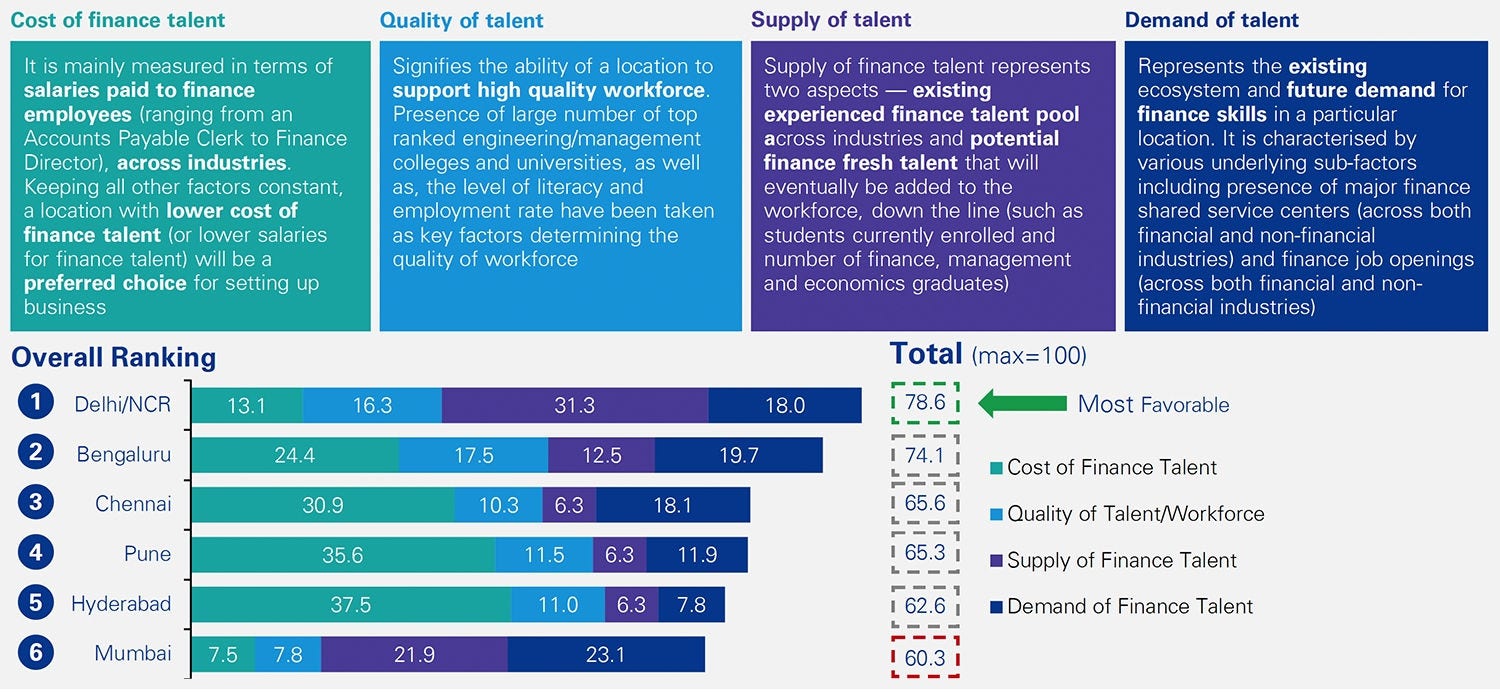

Finance Talent Sustainability Index

Finance Sustainability Index represents the ability of a particular location to sustain a finance business, in terms of generating relevant demand for finance jobs and proving adequate/relevant skilled workforce - all of it at a reasonable cost to the employer.

The four key factors making up the finance sustainability index

Based on the factors considered and weighting assigned, Delhi/NCR emerges as the leading location in the list, with a marginal lead over Bengaluru. Delhi/NCR’s high score in supply of finance talent (accounts for most number of finance graduates and houses various top universities) has offset its low score in cost of finance talent.

Bengaluru is ranked second after Delhi/NCR. However, this location receives better score in quality of workforce available. Bengaluru offer the highest quality of management talent with the presence of 27 MBA colleges ranked, and demand of finance talent and cost of Finance talent.

Chennai rounds up the top three leading location in the analysis and scores moderate on most parameters. It has a good quality of finance talent which can be hired at a reasonable cost. Chennai has emerged as a favorable city in terms of having low unemployment and attrition rates.

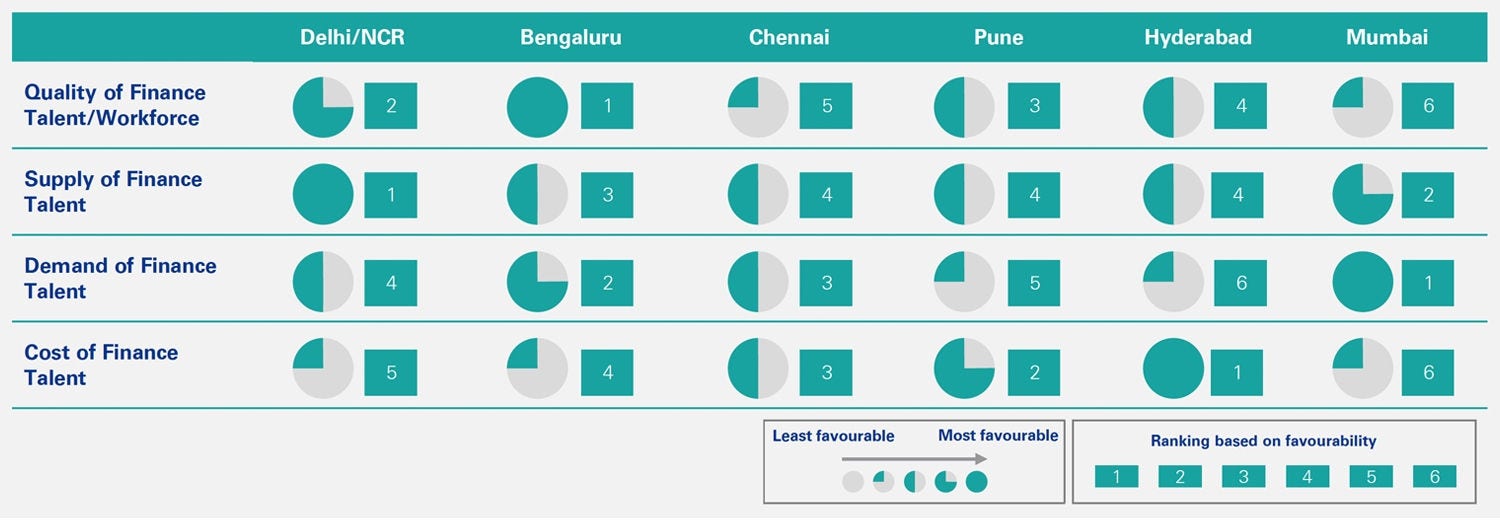

Deep-dive by each factor

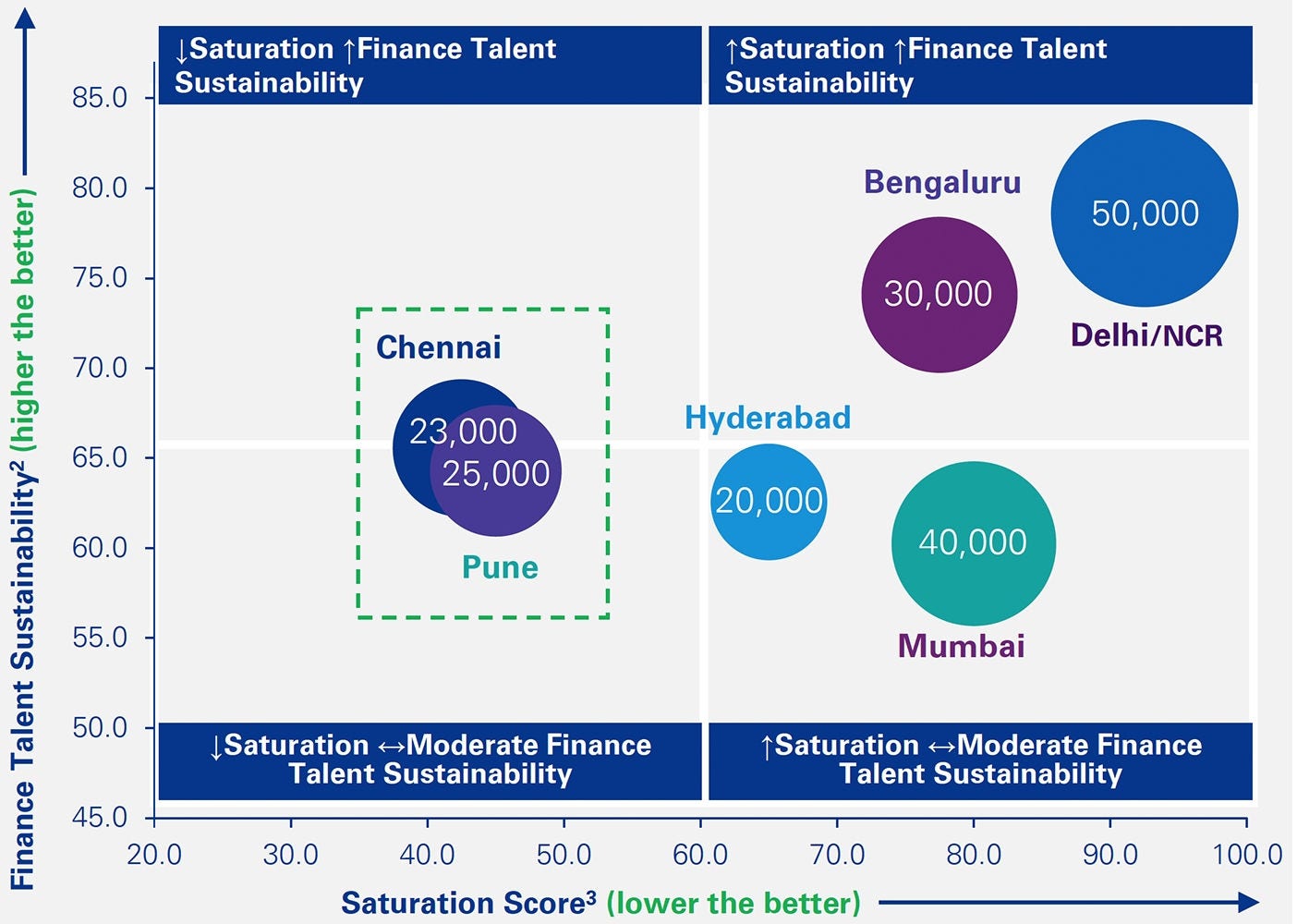

Finance talent sustainability index versus level of saturation

The finance sustainability index is them measured against the level of saturation, which is in turn measured by the supply offinance talent from higher education institutes. The Saturation Score is an important indicator of the long-term potential of the location –the future of finance function amidst the current industry-wide movement would involve a highly educated workforce, proficient in data science, business planning, with the strategic thinking skillsets from an MBA degree, possessing the analytical and numerical abilities from a strong engineering background.

The presence of a motivated, highly educated and nimble workforce would endow the location with the potential to build a future-proof finance organisation where its workforce can be retrained in the face of technological revolution, and is capable of undertakinghighly efficient centralised operational activities as well as core value-adding activities. Being well-supplied with high-quality talent also benefits the recruitment and retention of the workforce.

Key observations

Chennai and Pune have emerged as preferred locations in terms of the level of saturation and ability to sustain finance talent, mainly driven by — relatively low attrition rates, moderate finance costs, high demand to supply ratio (for finance skills) and a good presence of finance SSCs in thecity.

Both Chennai and Pune have a low level of saturation, as compared to other cities, but Pune’s ability to sustain financial talent is comparatively limited, despite its estimated finance graduates being marginally higher than Chennai. Moreover, as the cities are emerging and have low saturation, there exists a scope for them to grow further (as opposed to limited scope for Mumbai and Delhi).

Note (1): Size of bubble represents estimated Finance / economics & BA graduates per year (Higher the better)

Though Delhi has the highest Finance graduates relative to other cities and also fares well on the Finance Talent Sustainability Index (Rank 1), but the city seems saturated — especially in terms of having high finance costs and low demand is to supply ratio of financial skills.

Mumbai has emerged as the most unfavorable location both in terms of finance talent sustainability and level of saturation, mainly due to high costs of finance talent. Also Mumbai faces a huge challenge from other Financial serviceindustries.

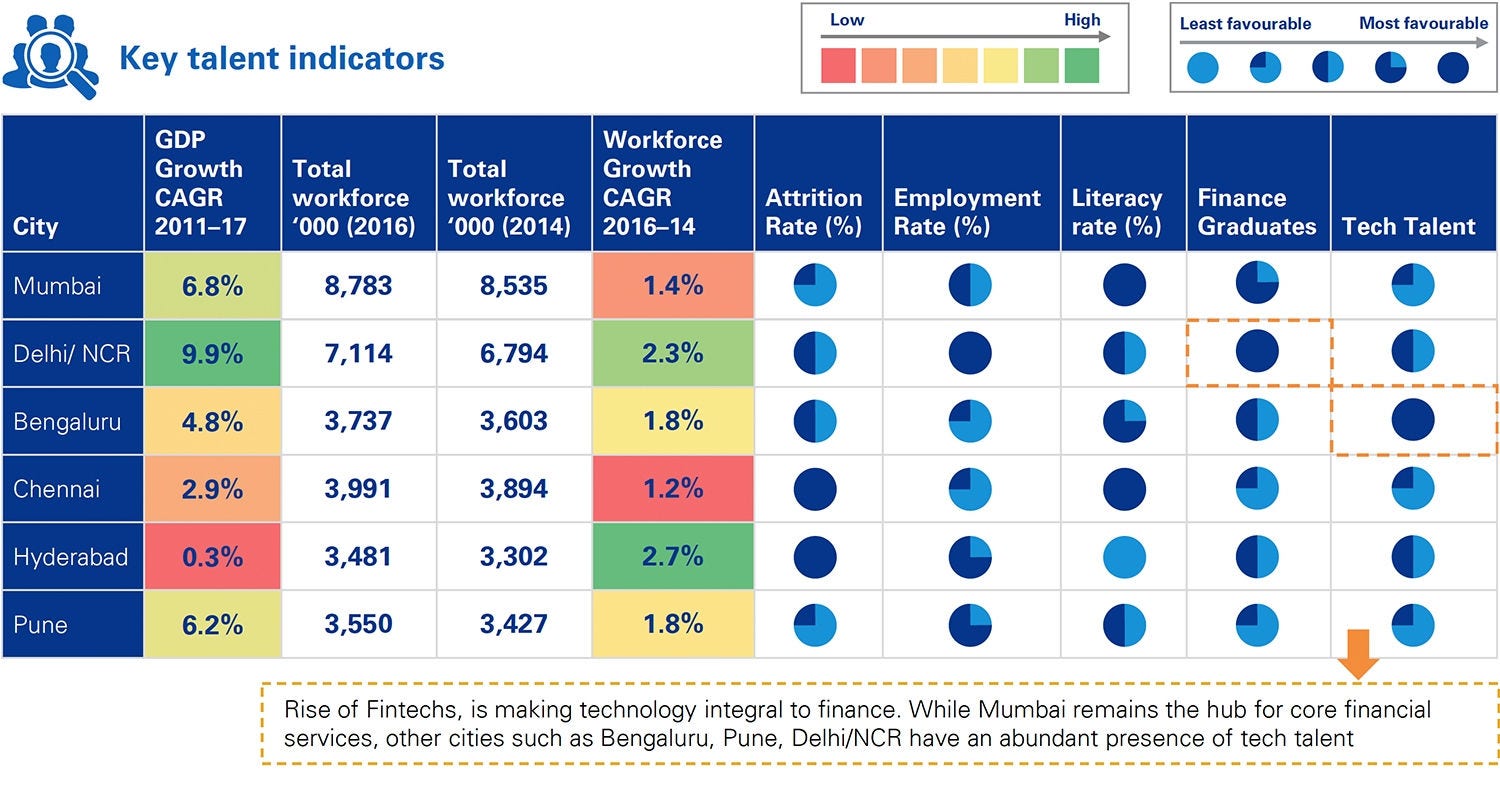

Key productivity and economic indicators

Several economic and economic indicators are investigated here. The economic growth factor reflects the overall confidence levelin the economic and political stability in the region –strong economic growth can be an indicator for business-friendly policies, efficient infrastructure, hub for attracting talents and prosperity of business activities. The growth in workforce can indicateboth presence of higher education institutes and the location drawing talents from other parts of the country. The employment rateshows the demand v.s. supply of labour in the region. Literacy rate indicates the availability of primary education in the region can be an indication the overall level of income inequality of the local population, thereby reflecting the social and political stability of living in these regions. The presence finance graduates and tech talent shows the region’s supply of much-needed skillsets for afuture finance function under technological developments.

Pros and cons of locations considered:

| Location | Pros | Cons |

|---|---|---|

| Delhi/NCR |

|

|

| Bengaluru |

|

|

| Chennai |

|

|

| Pune |

|

|

| Hyderabad |

|

|

| Mumbai |

|

|

Summary

Taking into consideration all the investigated criteria, Delhi NCR and Bengaluru are the most mature locations. They have the best supply of high-quality finance talents, strong economic growth which indicates social and political stability. The downside of these two locations is their high cost of labour and their high levels of saturation, which means the cities would become increasingly more expensive to attract and retain top talents.

Chennai and Pune are two up-and-coming locations with great potential. Chennai has good supply of finance talent at reasonable cost (30 percent lower than Mumbai), low attrition rate and low unemployment rate. Pune is also reasonable in cost and its good connectivity to Mumbai means that despite its relatively low supply of finance graduates (half of that of Delhi NCR), it can potentially attract talents from Mumbai. Recently, many companies such as KPMG and Wipro have set up shared centres in Pune, and therefore it has potential to develop into the next major regional SSC hub.

Hyderabad’s cost is the lowest (25 percent lower than Dehli NCR), and it has presence of good higher education institutes, supplying the market with engineering and MBA graduates. However, its maturity for SSC process is low, and its literacy rate is the lowest, which could be an indication for low human capital and social stability, and modest potential for future economic growth.

Mumbai, despite being India’s economic capital and well-supplied with finance talent, is the least favourable of all locations surveyed. It has high market saturation, relatively low presence of tech talent, very high cost of talent and high attrition rates. The demand for finance talent from other industries puts extra pressure on SSC in this saturated location.

Our accounting and finance insights

Something went wrong

Oops!! Something went wrong, please try again

Get in touch

Discover why organisations across the UK trust KPMG to make the difference and how we can help you to do the same.