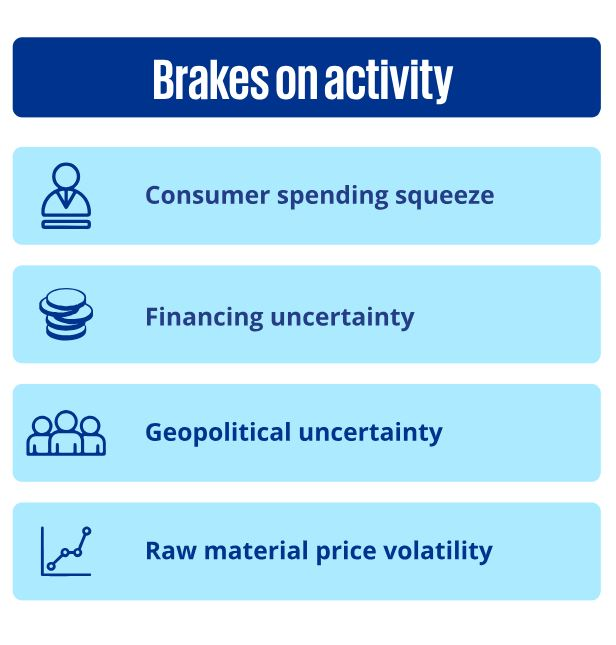

Investors do not like uncertainty. And 2023 was a year rife with it. Inflationary pressures, rising interest rates and slowing discretionary spending put pressure on consumer and retail companies alike as margins were squeezed and growth slowed. At the same time, geopolitical and economic uncertainty – combined with rising financing costs – put a damper on dealmaking. Uncertainty ruled.

The global C&R M&A market contracted 4 percent year-over-year to reach 5,340 deals worth US$174 billion with a more significant 27 percent decrease in deal value year-over-year, reflecting a particular slowdown in large transactions. The decrease in volume was fueled by slow activity in Europe (which fell 11 percent year-over-year to 2,136 deals) and ASPAC (a 4 percent decline year-over-year to 1,855 deals) which, together, make up 75 percent of all deals worldwide.

The decline in value was largely due to a 26 percent decrease in the number of large deals (more than US$100 million) in the sector. Meanwhile, Private Equity investments – which usually contributes more than 15 percent to all deals in the sector – saw volumes drop 4 percent as dealmakers refocused onto the mid-market.

Amongst sub-sectors, food and beverage (both brand owners and retailers) saw 2% decline year-over-year M&A activity, contributing 39 percent to deal volumes, on the back of the continuing activity in the health & wellness sub sector. Consumer products M&A declined by 4 percent year-over-year with just 1,193 deals. Retail deals suffered the highest volume declines, contracting 6 percent, led by a 56 percent decline in deals involving eRetail (internet and catalog retailing), likely due to some perceived mismatches between valuations and profitability.

Many of the factors that sowed uncertainty in 2023 are starting to stabilise, we expect the latter half of 2024 to deliver a slight uptick in M&A activity in the sector. Some expect interest rates to start falling in the second half of the year which should make deals more attractive. Other indicators are also improving – the Food Price Index, for example, trended downwards throughout 2023, which should help alleviate some of the margin pressure for some companies. Additionally, there will a lot of pressure on Private Equity (PEs) to do deals who sit on a nearly US$2.5 trillion dry powder and have been quiet over that last 18-20 months.

Pockets of strong activity are also expected. Some categories – such as luxury goods, pet care, and beverages (particularly health and wellness drinks) – are expected to be of higher interest to strategic and financial investors. Divestments will also drive activity as companies sell categories that are environmentally unsustainable or unhealthy. Expect divestment activity in the gum, confectionary and carbonated drinks segments, for example.

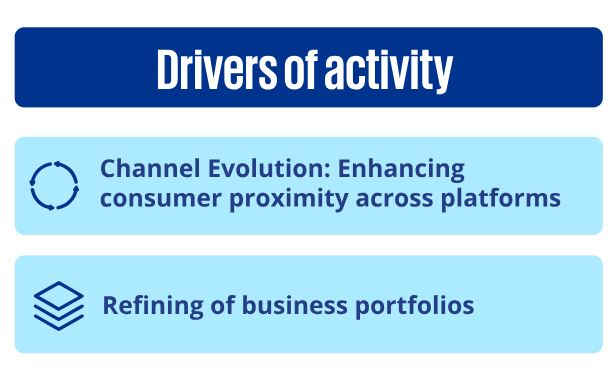

The pursuit of omni-channel capabilities is expected to continue to be a driver of M&A activity with online businesses look to interact with their customers in physical store settings, while brick-and-mortar entities leverage digital capabilities to better understand and predict consumer behavior. You should also expect to see an increase in the volume of spin offs, carve out and distressed assets coming to market as players refine their portfolios.

However, KPMG professionals are not forecasting an end to uncertainty in 2024. Far from it as there may not be any notable changes before Q2/Q3 2024. Indeed, you should expect to see continued geopolitical and economic uncertainty as many countries (more than half the world’s population) hold elections and as inflation proves more stubborn than expected. These have traditionally acted as brakes on M&A activity, and we expect this to be the case in 2024.

In this environment, dealmakers and investors will need to move cautiously. KPMG professionals help consumer and retail organisations on the buy side and sell side to create sustainable and quantifiable value through the deal process. Contact a KPMG firm to find out how the team can help your organisation grow through uncertainty, or contact a leader in your local market listed below. Additional support and guidance for this outlook provided by Amit Bhandari, Lorenzo Brusa, Fernando Fernandes, Michael Habboush, Chiaki Tani, Jose A. Zarzalejos Buesa, and Mayanka Sharma.