For many companies, the time has come to report on sustainability matters by adding Environment, Social and Governance (ESG) themes to the financial statements. The obligation to report on these topics stems from the European Green Deal and is laid down in the Corporate Sustainability Reporting Directive (CSRD). The standards, as part of the CSRD, are integrated into the European Sustainability Reporting Standards (ESRS).

First observations 'from sustainability to sustainability reporting'

For large EU Public Interest Entities, the time has already come to report on sustainability matters. As a result of the EU Omnibus* developments, for large unlisted companies, the obligation to meet the CSRD requirements has been postponed until 2027 (reporting in 2028).

Over the past period, while performing Assurance and Advisory services, we observed that companies are struggling to gather the necessary information in a timely manner. Our key observations to date:

- Documents that were indicated internally to be available turn out not to be in place or documents are not of an adequate level.

- Documents are not mutually consistent.

- Documents are emailed internally to a single contact person for sustainability reporting, as a result of which other colleagues have no insight into this documentation.

- Required information is stored in multiple server locations that are not accessible to those involved in creating the sustainability report.

- An overall overview of open actions/tasks and open questions to internal action holders and progress on these actions is missing or is incomplete.

- The deadline for internal delivery of the concept sustainability report and underlying documentation to management/the board is not met.

- The deadline for delivery of the final concept of the sustainability report and underlying documentation to the auditor is not met – with all its consequences.

Recognizable? Then consider using the KPMG CSRD Process Monitoring Manager.

Roadmap towards CSRD Reporting

Depending on a number of factors, as of financial year 2024 (reporting in 2025) or – based on the latest Omnibus proposal* communication – 2027 (reporting in 2028) companies are required to add ESG information to their regular financial statements. KPMG has developed a step-by-step plan to 'walk organizations through' how to meet the reporting requirements from the CSRD (on time).

The number of topics to be reported on in the annual report is determined by the requirements in the ESRS and by the mandatory Double Materiality Assessment (DMA). The Key Performance Indicators (KPIs) and (strategic) objectives to be reported on, are determined based on the established reporting framework.

How to gather the required information for ESG reporting?

A question that many organizations do not yet know how to answer. After all, for traditional annual financial reporting, processes and measures of internal control have been set up to ensure that all information is available on time internally. Timely delivery of information as part of the annual audit is therefore likely to happen.

However, the information needed to meet the requirements in the ESRS and the DMA is of a different nature. This may include:

- policy documentation;

- converting strategies into concrete objectives (KPIs);

- calculation models;

- templates as a starting point for annual reporting;

- evidence to support presented values;

- information from individual branches and departments; and

- information from the value chain.

Many organizations have not established a formalized process to collect and monitor information on the abovementioned requirements. This creates the risk that information and documentation will not be available or will not be available on time internally, resulting in a lack of time to perform an initial internal audit, insufficient quality and a late delivery of the PBC to the auditor. With all the consequences this entails.

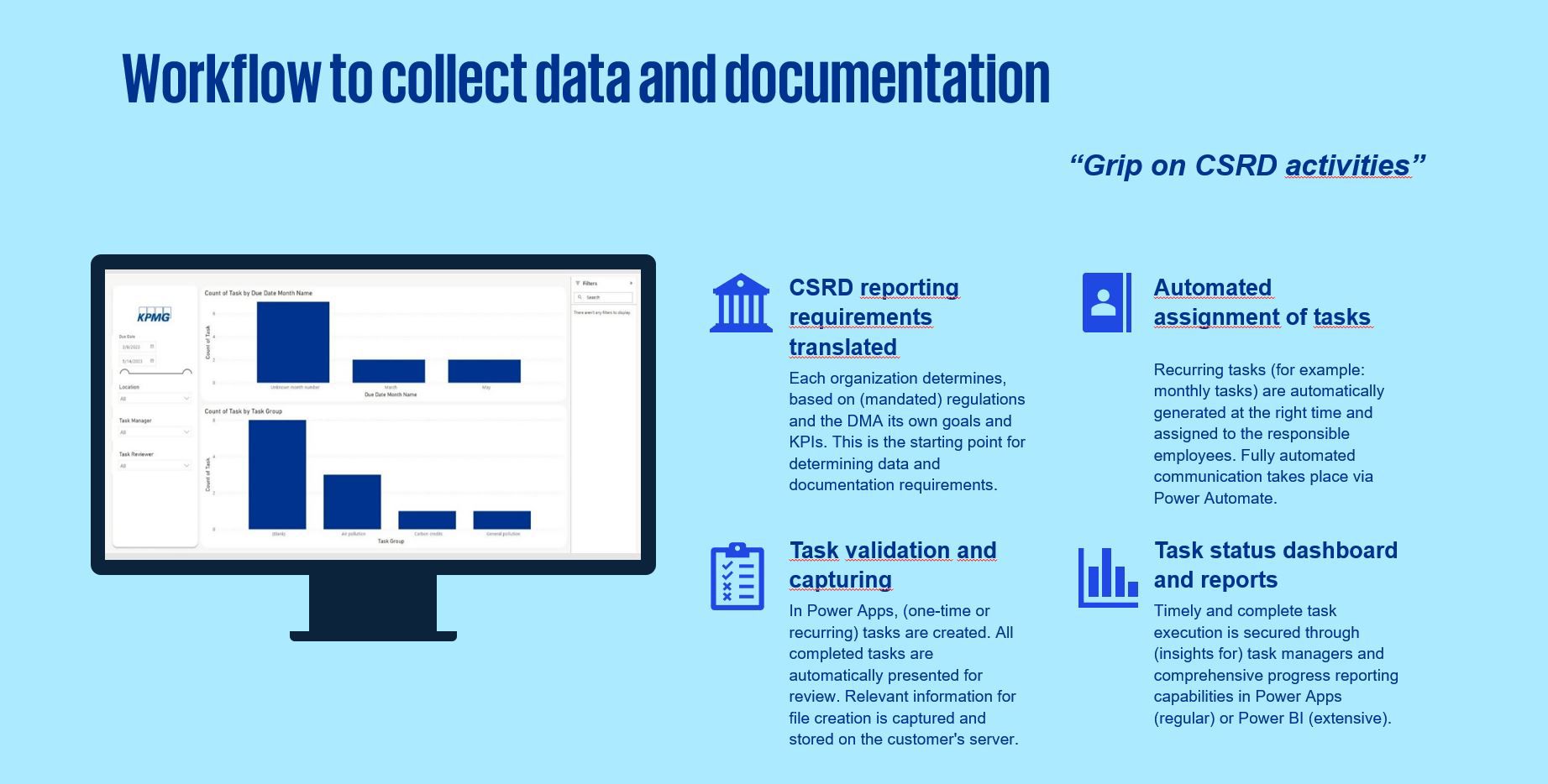

Process management solution for sustainability reporting

The KPMG CSRD Process Monitoring Manager is a process management solution for sustainability reporting based on the Microsoft Power Platform, and developed by KPMG. The configuration combines Microsoft Power Apps, Power Automate and Power BI to help companies get a handle on the activities required in the information collection process. For the purpose of internal communication, a link to Microsoft Teams and Outlook has been set up. By applying this configuration, the process of collecting the required information is set up (more efficiently) and a timely collection of the required documentation is ensured. The configuration includes the ability to (automatically) create one-time and/or periodic tasks.

Application of the integrated review functionality ensures that the required quality of the collected information and documentation is already established during the collection process before these are stored on the customer’s server location. By using Power Automate, fully automated progress reports can be sent to final managers– and reminders for task performance. The dashboarding functionality in Power BI allows the progress of the process to be monitored, focusing – where desired – on individual companies, departments, functions, etc. This is designed to be customer-specific.

* The European Commission released the Sustainability Omnibus proposal on 26 February 2025, bringing significant updates to sustainability regulations. These updates cover the CSRD, EU Taxonomy and the Corporate Sustainability Due Diligence Directive (CSDDD), aiming to streamline EU regulations and to reduce administrative and financial burdens while maintaining transparency and accountability under the CSRD. Despite these changes, sustainability remains a central focus for businesses striving to maintain transparency and credibility.