As climate change affects global mortality and morbidity patterns, actuaries at life insurers and pension funds will edge towards incorporating climate change uncertainty into their long-term mortality models, from scenario analysis and stress testing to reserving and pricing.

Recently, the Royal Dutch Actuarial Association published the latest mortality assumptions for the general Dutch population. As the Actuarial Association emphasizes, it intends to provide the sector with tools for determining mortality assumption rather than just a single mortality table to be used without further assessment. A relevant example for such further assessment is the potential effect of climate change on mortality.

Climate change has gained enormous attention over the past few years, and both common sense and various sources expect climate change to impact mortality. For instance, excess mortality in southern Europe could increase by 6.4% due to extreme temperatures compared to current mortality rates. The Actuarial Association’s mortality table does not yet take such effects into account, nor do benchmark climate change scenarios – such as the recently updated NGFS scenarios – feature explicit mortality assumptions. The most recent guidance from EIOPA on the ORSA scenario analysis for climate risk and industry initiatives, such as those of the Geneva Association, do explore the impact of climate risk on mortality assumptions via case studies. As such, it is the right time to start incorporating climate change considerations in the mortality assumptions of insurers and pension funds.

How to incorporate climate change considerations in the mortality assumptions?

Refining the ‘standard’ Actuarial Association’s Dutch mortality table for its own portfolio experience is a core exercise for any life insurer or pension fund. Such refinement typically focuses on correcting the ‘level’ mortality expectations (i.e., current age-dependent mortality probabilities), whereas

Climate change poses a potential structural break in the mortality trend.

climate change poses a potential structural break in the mortality ‘trend’ expectations (i.e., the development of future mortality probabilities). Since life insurance and pension contracts are very long-term in nature, monitoring for deviations in the mortality trend is essential to the future profitability and thus sustainability of the business model.

To start rethinking the trend expectations for the Dutch mortality table, interesting parallels can be drawn from the method chosen by the Actuarial Association to incorporate a COVID-19 correction:

- COVID-19 caused a correction to the trend of mortality improvements. Similarly, the impact of climate change on mortality will mean a change in the mortality improvement trend. An important difference between COVID-19 and climate change is that COVID-19 was a direct disruption due to the appearance of a new virus, whereas the impact of climate change can occur in very different ways and starts much more gradually.

- Following the analysis, and partially due to underlying expert judgment based on current information, COVID-19 has only a small impact on the mortality assumptions. One might argue that the same holds true for climate change. However, this can only be established after proper analysis, which is the topic of this blog. Furthermore, contrary to the COVID-19 correction, climate change will have a very long-term and chronic effect, amplifying the impact of even small trend changes.

- Ultimately, the COVID-19 correction consists of significant expert judgment on possible scenarios for the further development of the impact of COVID-19 on mortality. This will be no different for climate change, and it only makes sense to think about the potential impact in terms of scenarios and make the assumed expectations explicit. We consider the approach of the Actuarial Association to be good practice in this regard.

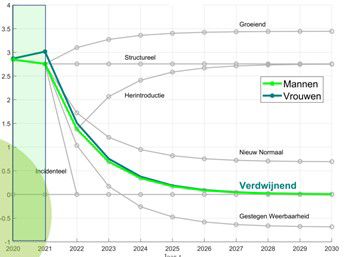

Figure 1: The Royal Dutch Actuarial Association has suggested various COVID-19 'pathways' or ‘scenarios’ for the impact of COVID on future mortality (link). These were developed based on expert judgment. Equally, the impact of climate change on the mortality trend will rely on pathways and require expert judgment to select the appropriate pathway (right).

The Royal Dutch Actuarial Association encourages adaptations to the mortality table for specific portfolio needs and to align with an organization-specific view. The pathway (or scenario) approach is an appropriate method to incorporate the uncertainties posed by climate change, be it acute or chronic physical effects (floods, wildfires, temperature rise, air quality) or the socio-economic context (e.g., is society capable of adapting or mitigating the physical effects). It reinforces the need to create a narrative driven by expert judgment and to explicitly document the chosen narrative. The actuary or modeler should not be too anxious about resorting to expert judgment and academic literature as referred to above. Climate change is notoriously complex and non-linear, involving structural breaks in various trends and looming ‘tipping points’. Expert judgment is unavoidable to assess trend changes, as simply extrapolating a trend from the past into the future may be one of the more unrealistic possibilities and underestimates the uncertainty involved.

Rethinking mortality assumptions for scenario analysis, reserving and pricing

The EIOPA application guidance explicitly mentions mortality assumptions and climate change in the context of the ORSA (or ERB for pension funds), i.e. in the context of climate scenario analysis. From a risk management perspective, the (ORSA) scenario analysis is indeed an appropriate start for understanding the potential impact of climate change on your organization’s mortality assumptions.

However, we would also expect assessments of climate change corrections (and other possible structural breaks in mortality trends) to be part of the sensitivity analysis of the technical provisions. Or that the reserve itself be corrected for the trend that is deemed appropriate for the future. Again, the Dutch mortality table framework facilitates such sensitivity analyses, as it allows analyses at the confidence interval surrounding the best estimate. As such, we would expect climate change to be an explicit consideration for pricing purposes as well, reflecting the increased uncertainty in price setting.

In summary, when various independent sources warn of the implications of climate change on mortality, morbidity and health, the actuary at a life insurer or pension fund should perform climate-focused studies to understand the potential impact of climate change on mortality assumptions for provisioning, pricing and scenario analysis or stress testing.

How KPMG can help

Studying the impact of structural breaks in the mortality trend on your organization is multi-faceted: not only does it require proficiency with mortality modeling, it also requires familiarity with climate change trends and underlying causes, as well as an understanding of expert elicitation to establish assumptions. These are all fields in which KPMG has experts that can rely on multidisciplinary collaboration, both nationally and internationally. Please do not hesitate to contact us to discuss how KPMG can support you in performing such a mortality study, or other challenges to establish the required long-term (ESG) view on your strategy and risk management.

Discover more

Contacts

Senior Manager, Financial Risk Management

KPMG in the Netherlands

Manager, Financial Risk Management

KPMG in the Netherlands

Manager, Financial Risk Management

KPMG in the Netherlands

We will keep you informed by email.

Enter your preferences here.