During the panel, we have highlighted several common areas of scrutiny by the IRB during a tax audit and prevailing tax disputes which should warrant further review by taxpayers. Our discussion on these common areas can be broadly summarized and classified as follows:

Income: Issues pertaining to recognition of income, advance income, accruals, and tax law changes, as well as undeclared income concerns, such as gains from asset disposal and rental income. Documentation beyond accounting records, such as license agreements and legal opinions, was highlighted for proving income intention. Additionally, emphasis was placed on whether companies have the necessary SOPs to properly recognize lump sum income over time, considering differing accounting and tax rules.

Expenses: The distinction between advertising and entertainment expenses, particularly hospitality-related costs like food and beverages, can be nuanced. Similarly, sponsorship expenses may involve entertainment elements, necessitating careful evaluation. These considerations underscore the importance of strong tax governance within the company, including the need for proper SOPs and documentation to clarify intentions, beneficiaries, and compliance with tax regulations.

Incentives: Scrutiny surrounding claims of incentives after expiry or without meeting conditions was also addressed, as well as reinvestment allowance claims, disputes arise due to interpretation gaps on terms like "factory" and "manufacturing," insufficient documentation for qualifying projects (i.e. Project Paper), and claims on non-qualifying assets. This emphasizes the need for companies to review their claim of incentives such as Reinvestment Allowance (RA) claims.

Transfer Pricing: Companies face common risk areas in transfer pricing, such as intragroup financing, intragroup services, royalties’ payments, and limited risk entities. It must be prepared to defend the arm's length nature and economic substance of its transactions.

Crucially, good tax governance is a subset of good corporate governance. This involves assessing the organizational process, reviewing its tax risks and mitigating those tax risks, which organizations are encouraged to look into. It is vital to remember that aside from the proper documentation and good governance practices, the end of SVDP 2.0 does not signal an endgame for transfer pricing.

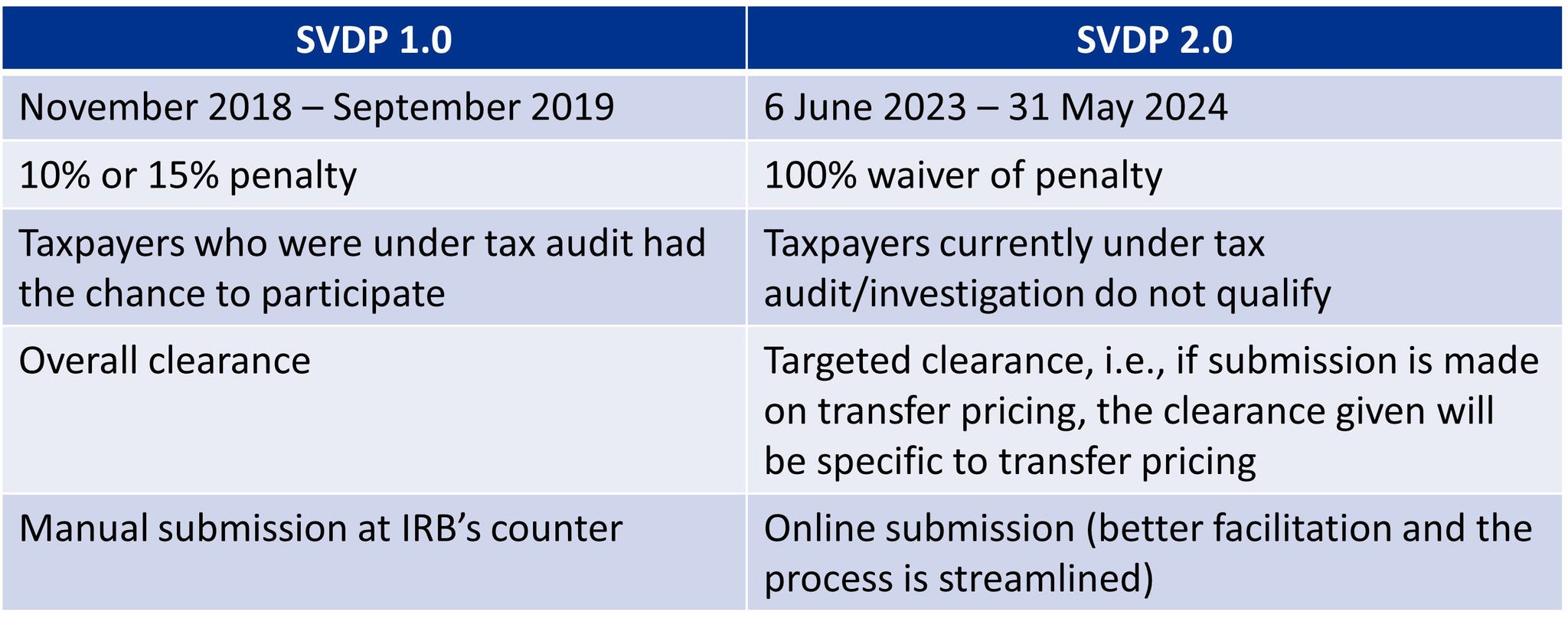

As cooperative taxpayers, businesses can still participate in voluntary disclosure under the existing audit framework. With SVDP 2.0 approaching its conclusion on 31 May 2024, taxpayers are encouraged to seize this opportune moment to assess the potential areas they would like to report and avail themselves of the zero percent penalty rate. With the impending implementation of e-invoicing, now is the ideal time for taxpayers to reassess their tax reporting strategies and ensure compliance with regulatory requirements.