The Omnibus package proposes changes to the infamous Corporate Sustainability Reporting Directive (CSRD), which requires large and publicly listed companies to report on sustainability, as well as to the EU Taxonomy.

CSRD currently requires large undertakings and listed companies (excluding micro-undertakings to report on sustainability matters.

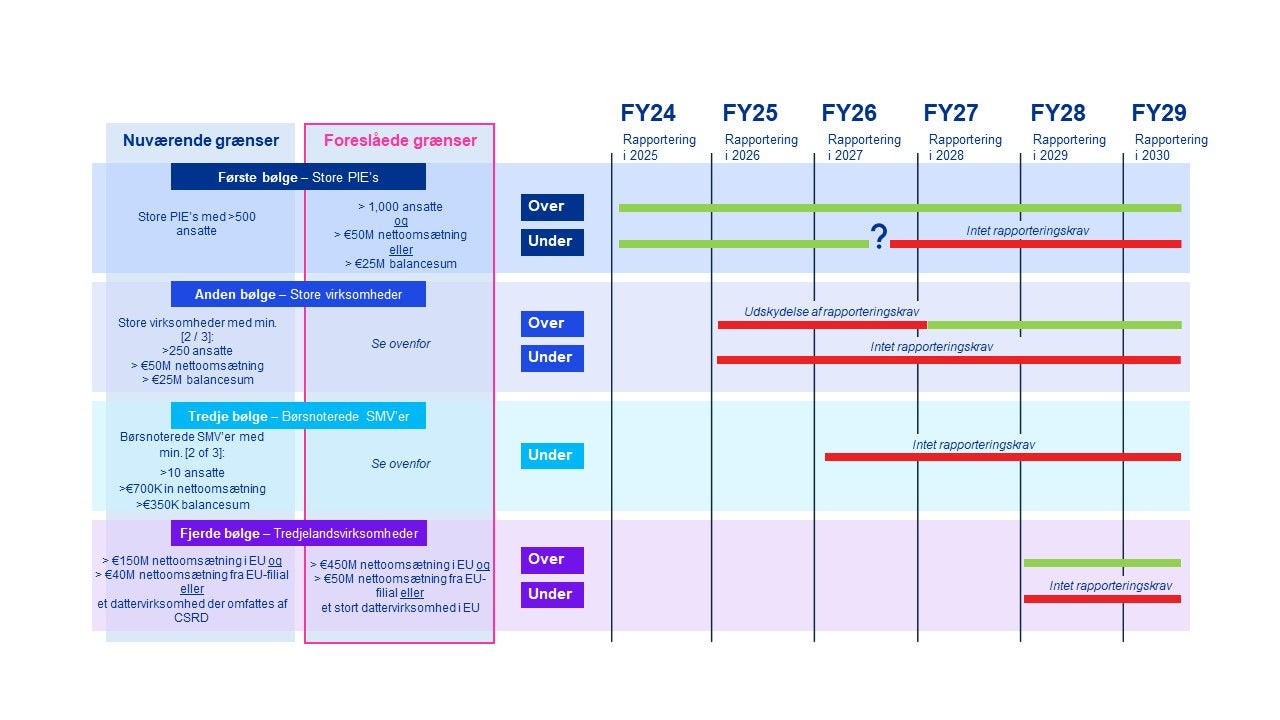

With the Omnibus package, the European Commission commits to reducing the volume and complexity of reporting requirements for all affected companies. Additionally, the package includes significant proposed amendments to the scope of the CSRD and the dates from when companies will be subject to its requirements.

The proposed changes to the scope would mean that only companies with more than 1,000 employees and exceed one of the following thresholds for two consecutive years would be covered:

- Net revenue of €50 million (approximately DKK 391 million); or

- Balance sheet total of €25 million (approximately DKK 195 million).

The timeline is proposed to be postponed by two years for companies that were not already subject to the requirements starting from financial years beginning on or after January 1, 2024.

Companies that fall outside the scope of the CSRD are instead encouraged to report in accordance with the voluntary SME standards issued by the EU Commission. These standards will also set a limit on the amount of information that CSRD-covered companies can require from companies that are not in scope.

The transition from limited assurance to reasonable assurance, as well as the issuance of planned sector standards—such as those for financial institutions—is also proposed to be removed.

Impact on the EU Taxonomy

The requirement to report under the EU Taxonomy, which is currently aligned with the scope of the CSRD, is also proposed to change. Under the new proposal, this reporting would only be mandatory for companies with more than 1,000 employees and a net revenue exceeding €450 million (approximately DKK 3,375 million).