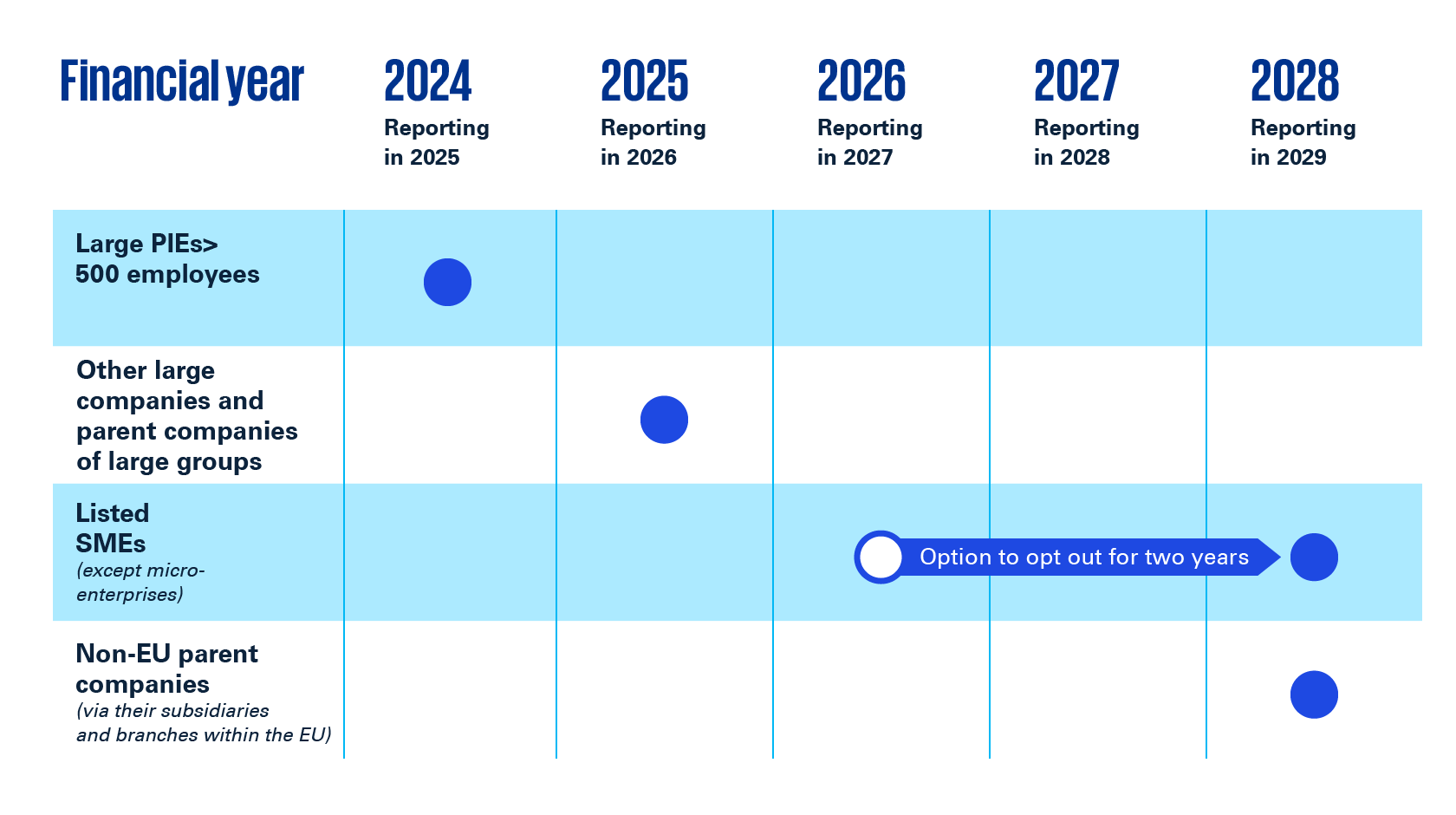

On 13 October 2023, the legislative proposal, which primarily aims to implement the EU's Corporate Sustainability Reporting Directive (CSRD), was submitted for public consultation. The proposal also implements an EU delegated directive that adjusts the thresholds for micro, small, medium and large companies and groups.

The proposal, which amends more than 10 different laws, will make it mandatory for certain companies to prepare a comprehensive sustainability report and include it in the company's management report when presenting the company's annual report. At the same time, the sustainability report must be digitally labelled and accompanied by a limited assurance auditor's report.

Initially, sustainability reporting must be carried out in accordance with the European Sustainability Reporting Standards (ESRS), which contains more than 1,000 data points across 12 standards in the areas of environment (E), social (S) and governance (G). However, the companies covered are only required to report on the data points that they consider material based on a double materiality assessment. This means that each company must only report on those matters that it considers to have a material impact on its external environment and/or its own finances.

The European Commission is also expected to adopt specific standards that will apply to SMEs and third country entities, as well as a number of sector-specific standards, including for the oil and gas, transport, energy and textile sectors, among others.

The draft standards are being prepared by the European Financial Reporting Advisory Group (EFRAG), which is scheduled to publish the first draft of the SME standards in April 2024. You can read more about EFRAG's work on developing sector-specific standards here.