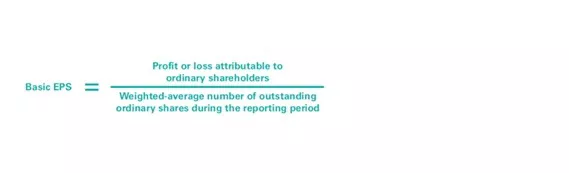

Earnings per share (EPS) have always been the focus of investors, analysts and other stakeholders. It is therefore essential for the reporting of capital market-oriented companies to know the key drivers of this indicator and to manage them appropriately. In accordance with IAS 33, (basic) EPS is calculated by dividing the profit or loss attributable to the owners of the ordinary shares by the weighted average number of ordinary shares outstanding during the reporting period (see Figure 1).

Figure 1: Basic EPS

Source: KPMG in Germany, 2025

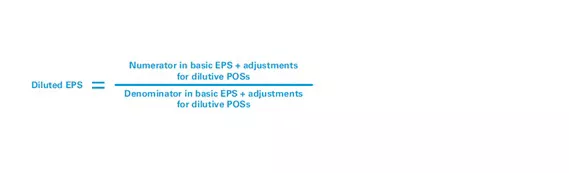

However, this figure does not take into account any dilutive effects from potential ordinary shares (POS). Diluted EPS, on the other hand, includes these effects in both the numerator and the denominator (see Figure 2).

Figure 2: Diluted EPS

Source: KPMG in Germany, 2025

Depending on the form and volume of the programme, share-based payments can have a noticeable impact on the determination of diluted EPS in accordance with IAS 33.1 Companies should therefore be aware of the interactions between share-based payments and the determination of diluted EPS and avoid potential pitfalls in this context. Furthermore, an understanding of which design parameters of share-based payments influence the determination of diluted EPS should be developed in order to be able to implement a remuneration design that is optimally aligned with the interests of shareholders. The form of fulfilment (settlement) and any exercise conditions are of particular importance here.

Type of settlement

IFRS 2 makes a fundamental distinction between share-based payments on the basis of the form of fulfilment (settlement). Although IAS 33 does not explicitly refer to this classification, it only has an effect on diluted EPS if settlement takes place or can take place in genuine equity instruments (equity settlement). However, programmes that only provide for settlement in cash (cash settlement) are not to be taken into account. For share-based payments with a settlement option on the part of the company, settlement in genuine equity instruments is always assumed for the purposes of determining EPS, even if the issuing company classifies and presents the remuneration programme as cash-settled under IFRS 2.

Type of exercise conditions

If options are issued as part of a share-based payment, the denominator of the diluted EPS must generally be determined in accordance with IAS 33 using the treasury share method. Whether and to what extent the option rights are to be recognised under this method depends on the contractually agreed exercise conditions: If there is only a service condition, the options granted are classified as (forfeitable) potential ordinary shares in accordance with IAS 33 and must be recognised under the treasury share method.

If, on the other hand, there are additional market-related and/or non-market-related performance conditions, the options are classified as contingently issuable potential ordinary shares, which must be recognised using a two-stage process. At the first stage, the number of options for which the performance conditions are met on the balance sheet date in question is determined. Only these subscription rights are to be included in the treasury share method at the second stage. However, options for which the performance conditions are not met on the balance sheet date are not taken into account.

Application of the treasury share method

An integral part of the treasury share method (see Figure 3) is to determine the so-called "bonus element" (step iii) and add this to the denominator of the basic earnings per share. The dilution effect results from the difference between:

- the number of ordinary shares that would theoretically have to be repurchased at the average market price in order to fulfil the beneficiaries' entitlements (step ii), and

- the number of forfeitable potential ordinary shares deemed to have been issued.

Abbildung 3: Treasury Share Method

Source: KPMG in Germany, 2025

The assumed proceeds (step i) for options issued as part of share-based payments are made up of two components:

- Exercise price × number of shares, and

- (grant date) fair value in accordance with IFRS 2, if not yet earned.

As a result, these instruments have an increasingly dilutive effect over time - under otherwise constant conditions: The fair value still to be recognised is reduced due to progressive vesting, which also reduces the assumed proceeds. In addition, the dilutive effect depends on the average share price during the reporting period. If this increases, the number of ordinary shares that would theoretically have to be repurchased at the average market price in order to fulfil the beneficiaries' claims decreases and the dilutive effect increases. The exercise price of the instruments granted should also not be neglected: the lower it is, the greater the dilutive effect.

Conclusion

Depending on their specific structure, share-based payments can have a significant impact on the calculation of EPS due to their dilutive effect. It is often initially unclear whether the instruments granted as part of share-based payments should be included in the calculation at all. If this is the case, the application of the treasury share method is often complex and harbours numerous pitfalls. Companies should be aware of this when designing a corresponding remuneration programme.

Our services for you

We are happy to support and advise you on questions relating to the calculation of earnings per share in the case of simultaneous share-based payments and show you the possible effects on EPS when introducing new remuneration systems.

Source: KPMG Corporate Treasury News, Issue 157, August 2025

Authors: Ralph Schilling, CFA, Partner, Head of Finance and Treasury Management, Treasury Accounting & Commodity Trading, KPMG AG

Jan-Philipp Wallis, Senior Manager, Finance and Treasury Management, Treasury Accounting & Commodity Trading, KPMG AG

_

1 Depending on their structure, share-based payments can also influence basic EPS.

Your contact

Ralph Schilling

Partner, Audit, Head of Finance & Treasury Management

KPMG AG Wirtschaftsprüfungsgesellschaft