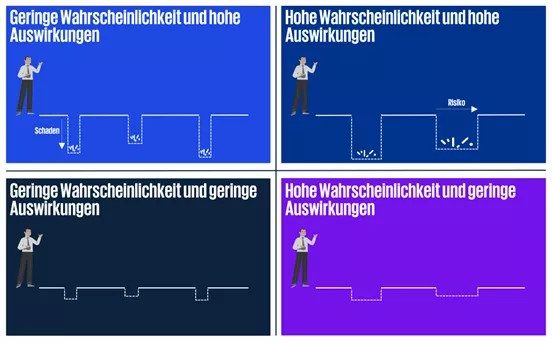

In the top right quadrant, we see a debtor portfolio with a high probability of default and a high loss volume, translated into credit risks. With this type of risk portfolio, insurance seems to be the obvious choice, as bad debt losses are practically pre-programmed. In practice, however, it has been shown that such profiles are recognised by the insurer and are actively managed and excluded through partial underwriting or rejection of individual debtors. Credit insurance is therefore not the best choice for this profile. Instead, the recommendation here is to take a strategic look at the target customer portfolio, expand lower-risk customers and gradually reduce the high-risk positions.

The quadrant at the bottom right represents a profile in which numerous and often regular, smaller structural losses are realised at the same time. In business areas that correspond to such a profile, every default is annoying, but does not jeopardise the existence of the company. The recommendation here is to recognise the easily predictable, minor losses themselves with an appropriate risk margin, provided this can be implemented in the market. In addition, active credit management can counteract the frequency of risk through evaluation with the help of external credit reports in combination with appropriate business consequences, e.g. by obtaining advance payment regulations.

The situation is similar in the quadrant at the bottom left. In this profile, only minor defaults are likely to be realised. Credit management efforts here can be limited to portfolio analysis by sector, country and other structural factors in order to recognise at an early stage if the risk profile changes.

The last quadrant, which combines low probability with high risk volumes, offers the most interesting potential for credit insurance. As the policyholder, you protect yourself against unlikely worst-case scenarios that could jeopardise your company's existence. For the insurer, on the other hand, the economic risks are manageable, as it can offset any insurance benefits that may arise through the diversification effects of its own insurance pool. In this case, the use of credit insurance is economically attractive for both parties and a clear recommendation.