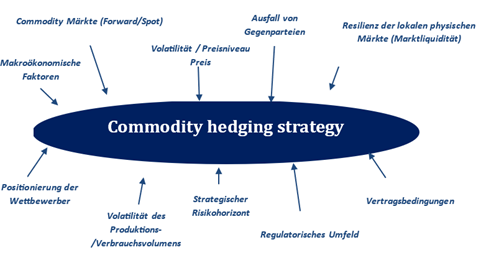

Commodities such as metals, agricultural goods, energy and energy sources are of crucial importance to the global economy. Their prices are highly volatile due to factors such as changes in supply and demand, geopolitical events, currency fluctuations and changes in economic policy (Fig. 1). This volatility leads to unpredictability in production costs, complicates financial planning and liquidity management and has a negative impact on long-term investment decisions, making companies more cautious in uncertain markets. In order to ensure the necessary planning security, it is crucial that companies analyse their exposure to the commodity and energy markets in detail and develop effective hedging strategies. These strategies must be regularly adjusted to take account of geopolitical events, market volatility and regulatory changes in order to minimise financial risks and ensure stability. In addition, inflation affects the purchasing power of currencies and thus the price level of all commodities.

In view of these challenges, it is crucial for companies in the commodity and energy-intensive industries not only to adjust their hedging strategies, but also to regularly review the associated risk strategy. This review should ensure that the strategy is in line with the company's objectives and that all relevant risks are adequately taken into account. In addition, it is important to evaluate the reliability of the risk metrics in relation to the company's performance.

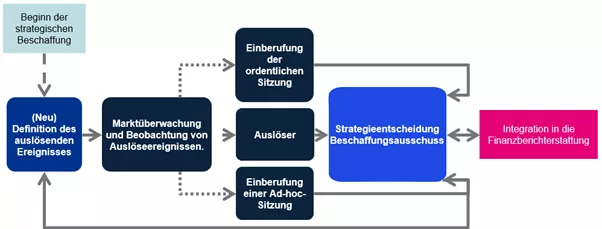

As part of the exposure survey, it is necessary to precisely determine the volume and timing of the commodity risk. Different types of business and possible time delays in risk transfer must be taken into account. Furthermore, the risk-bearing capacity must be defined in order to determine what level of risk is acceptable and which risk measurement methods should be used.

A clear hedging strategy that is regularly reviewed for its effectiveness is also of great importance. This strategy should not only include methods for measuring success, but should also be adaptable in order to be able to react to changes in the market.

Finally, it is crucial to establish clear governance structures that clearly regulate the framework conditions and responsibilities in commodity trading. These structures help to ensure that the risk strategy is effectively implemented and continuously improved.