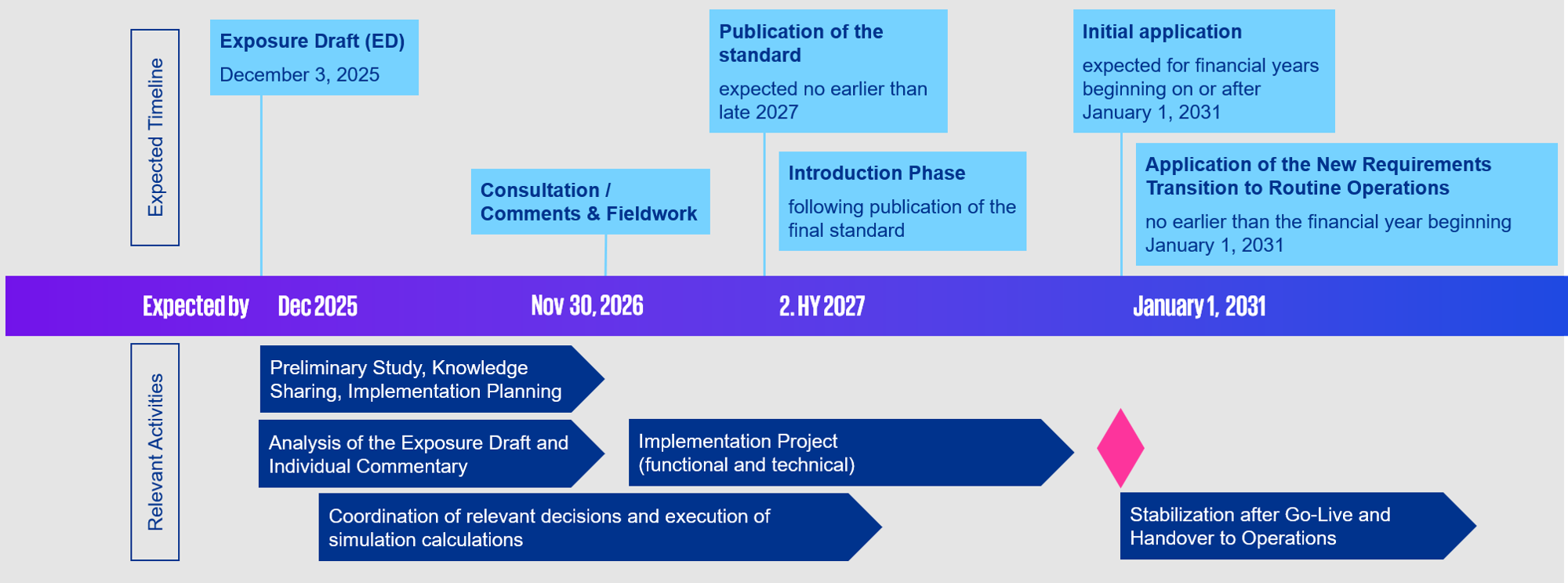

On 3 December 2025, the International Accounting Standards Board (IASB) published the long-awaited exposure draft on Risk Mitigation Accounting (RMA) – which had previously been announced and discussed under the name Dynamic Risk Management (DRM).

This future framework for the financial reporting of (interest rate) risk management (the successor to IAS 39 Portfolio Fair Value Hedges) will fundamentally change the interplay between treasury, risk control and accounting, and has numerous implications. Our experts support companies in preparing for these complex challenges.