The legislation to introduce a patent box tax incentive in the Hong Kong SAR (Hong Kong) was enacted on 5 July 2024. This means that from the year of assessment (YOA) 2023/24 onwards, taxpayers can elect to enjoy a 5% concessionary tax rate for Hong Kong-sourced taxable profits derived from use or sale of eligible intellectual property (IP), subject to fulfilment of the specified conditions.

Summary

The Inland Revenue (Amendment) (Tax Concessions for Intellectual Property Income) Ordinance 20241 (the Ordinance) was gazetted on 5 July 2024. The Ordinance introduces a patent box tax incentive in Hong Kong that offers a 5% concessionary tax rate for Hong Kong-sourced taxable (i.e. non-capital) profits derived from the use or sale of eligible IPs, subject to certain conditions. The incentive applies retrospectively from YOA 2023/24.

For more details of the patent box tax incentive as set out in the draft legislation (the Bill) previously released2, please refer to our Hong Kong SAR Tax Alert – Issue 4, April 2024.

The Legislative Council formed a Bills Committee to scrutinise the Bill gazetted and invited submissions on the Bill3. The HKSAR Government subsequently provided its responses to the submissions received4 and proposed an amendment (as a Committee Stage Amendment)5 to the Bill based on the comments received (see discussion below).

The amendment to the Bill

In our submission on the Bill, we highlighted that the originally drafted Bill would give rise to a seemingly unintended outcome. Specifically, the transitional arrangement6 for computing the R&D fraction when insufficient records are kept by taxpayers would apply to eligible IP income accrued during the whole basis period for YOA 2023/24 for taxpayers with an accounting year-end date of March 31, but only part of the basis period for YOA 2023/24 for taxpayers with other accounting year-end dates.

In response to the comments received, the government put forward an amendment to the Bill to clarify that the transitional arrangement applies to the three-year period from the first day of the taxpayer’s basis period for YOA 2023/24 (instead of 1 April 2023) to the last day of the taxpayer’s basis period for YOA 2025/26 for all taxpayers, regardless of their accounting year-end dates. The amendment has been incorporated into the final legislation enacted.

Key clarifications/updates in the government’s responses

1. Copyrighted software as eligible IP

Eligible IP for the purposes of the patent box tax incentive includes a copyright subsisting in software under the Copyright Ordinance in Hong Kong or the law of any place outside Hong Kong. While registration of copyrighted software is generally not required under the Hong Kong or foreign law, the government indicated that the copyrighted software must fall within the scope of the relevant legal protection for it to be regarded as an eligible IP and that further guidance and illustrative examples on this will be provided.

Giving the relatively wide application of copyright software in different industries, it would be helpful if the guidance could shed light on what information / evidence is required from taxpayers to satisfy the IRD that the software “fall within the scope of the relevant legal protection” given that such copyright / protection is usually acquired automatically when an original work is generated.

2. Cost-sharing arrangement (CSA)

Similar to the IRD’s current assessing practice for deduction of R&D expenditure under a CSA7, where a taxpayer has undertaken part or all of the underlying R&D activities under a development CSA, the taxpayer’s share of R&D costs under the CSA could qualify as eligible R&D expenditure incurred by the taxpayer for the purposes of the patent box tax incentive, subject to certain conditions.

The IRD plans to provide relevant guidance and illustrative example on its website or in a Departmental Interpretation and Practice Note on the application of the incentive under a CSA after the law is enacted.

3. Family of eligible IPs

The government confirms that the patent box tax incentive does not adopt the product-based approach set out in the OECD’s BEPS Action 5 report. In cases where a taxpayer’s R&D activities generate a family of eligible IPs, taxpayers would be required to apportion and allocate the relevant R&D expenditure to each of the eligible IPs on a just and reasonable basis. The pros of this apportionment approach is it may offer greater flexibility to taxpayers in allocating the R&D expenditures to different IPs whereas the cons is there could be considerable uncertainty on what is regarded by the IRD as a “just and reasonable” basis and what taxpayers have to do to discharge the burden of proving the apportionment is just and reasonable. More guidance on this from the IRD would be welcomed.

KPMG Observations

We commend the HKSAR Government for introducing the patent box tax incentive in Hong Kong. We look forward to the business-friendly implementation of the incentive and timely issuance of practical guidance on its administration.

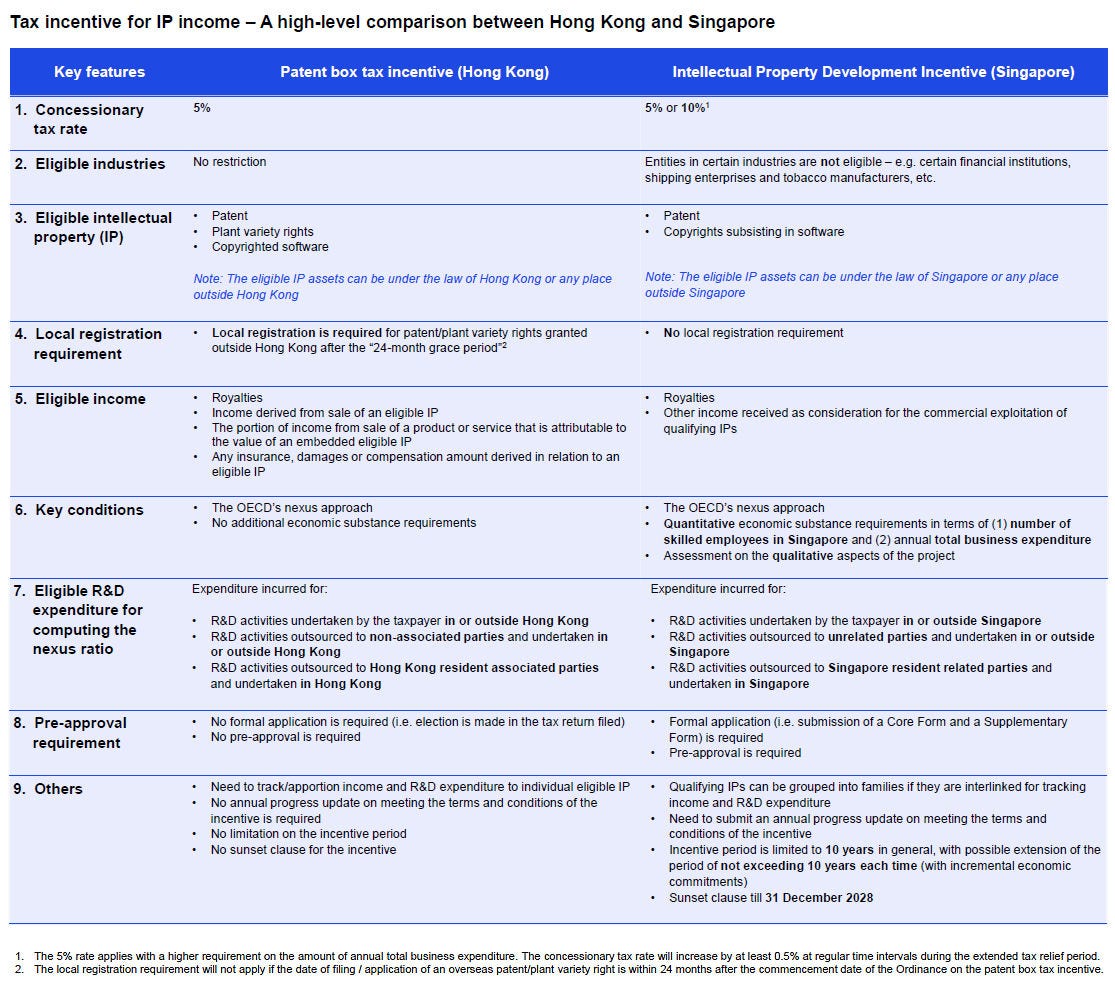

We set out a high-level comparison between the patent box tax incentive in Hong Kong and the Intellectual Property Development Incentive (IDI) in Singapore in the Appendix. As can be seen from the comparison, the incentive in Hong Kong is more competitive in a number of aspects - e.g., a lower concessionary tax rate (in certain circumstances), a wider scope of application, no economic substance requirements (other than the nexus requirement), no application, pre-approval or renewal requirements, and no sunset clause for the incentive.

Business groups in Hong Kong that carry out IP development and exploitation activities should consider whether they can benefit from the patent box incentive in Hong Kong and whether any restructuring of the IP holding structure or business operation models would be necessary. They should also stay tuned on the guidance and illustrative examples on the incentive to be issued by the IRD.

1 The Ordinance can be accessed via this link.

2 The Bill can be accessed via this link.

3 KPMG is one of the parties that made a submission on the Bill. Please refer to this link for all the submissions received.

4 The government’s responses can be accessed via this link.

5 For details of the amendment to the Bill, please refer to this link.

6 Under the transitional arrangement, a taxpayer can elect to compute the R&D fraction based on the total eligible R&D expenditure and total non-eligible expenditure incurred by the taxpayer in respect of all IP assets during a 3-year rolling period, and there is no need to track and link the expenditure to individual eligible IP.

7 The IRD’s assessing practice for R&D tax deduction under a CSA is set out in paragraphs 87 to 97 of DIPN 55.

Appendix

The patent box tax incentive in Hong Kong comes into operation

Hong Kong SAR Tax Alert - Issue 7, July 2024