We commend the HKSAR Government for introducing a patent box tax incentive in Hong Kong. We look forward to the pragmatic and business-friendly implementation of the incentive for it to serve the policy intent of encouraging more R&D activities and IP commercialisation in Hong Kong.

To further enhance the overall IP tax regime in Hong Kong, we recommend that the following issues be considered: (1) introducing a tax deduction for amortisation expenses for intangible assets in general, (2) enhancing the current tax deduction of IP acquisition costs and (3) considering the impact of Pilar 2 of BEPS 2.0 on the patent box tax incentive and the enhanced tax deduction for R&D expenditure.

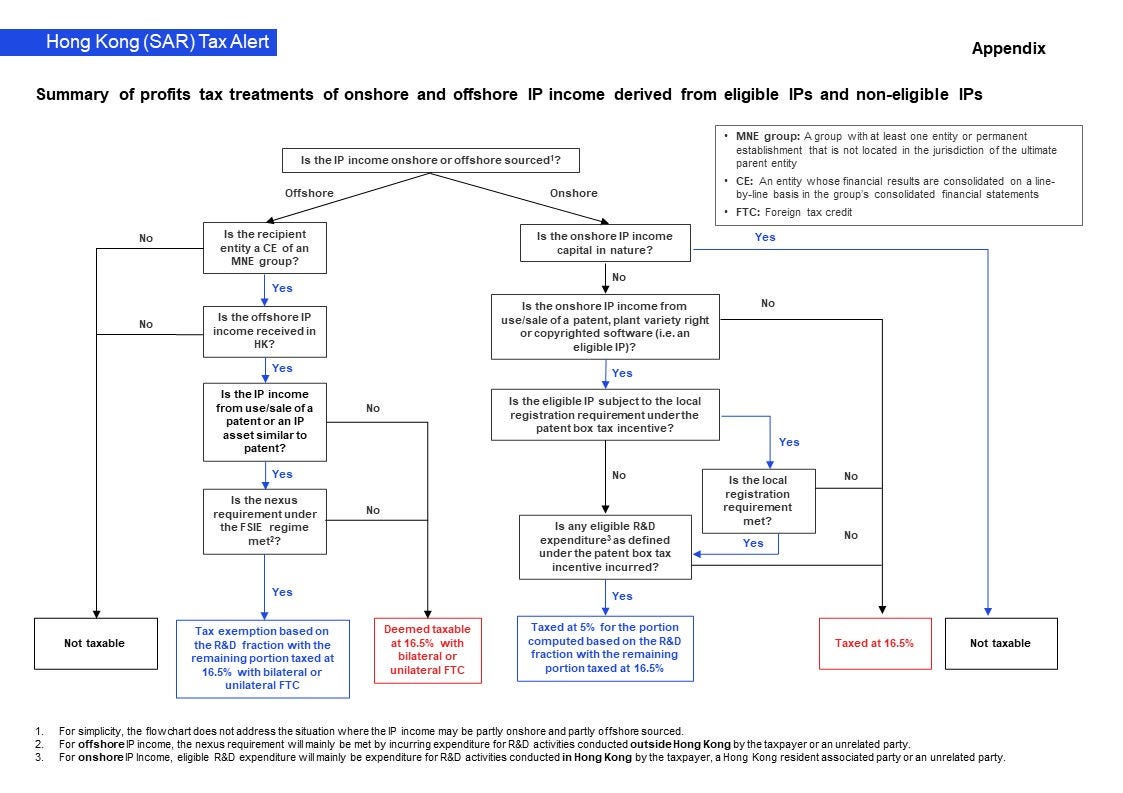

Business groups in Hong Kong that carry out IP development and exploitation activities should consider the different Hong Kong profits tax outcomes for onshore and offshore IP income. The flowchart in the Appendix summarises the respective tax treatments of onshore and offshore IP income derived from eligible IPs and non-eligible IPs under the existing FSIE regime and the proposed patent box tax incentive.