19 May 2026

Corporate tax: United States’ special status increases pressure on Switzerland

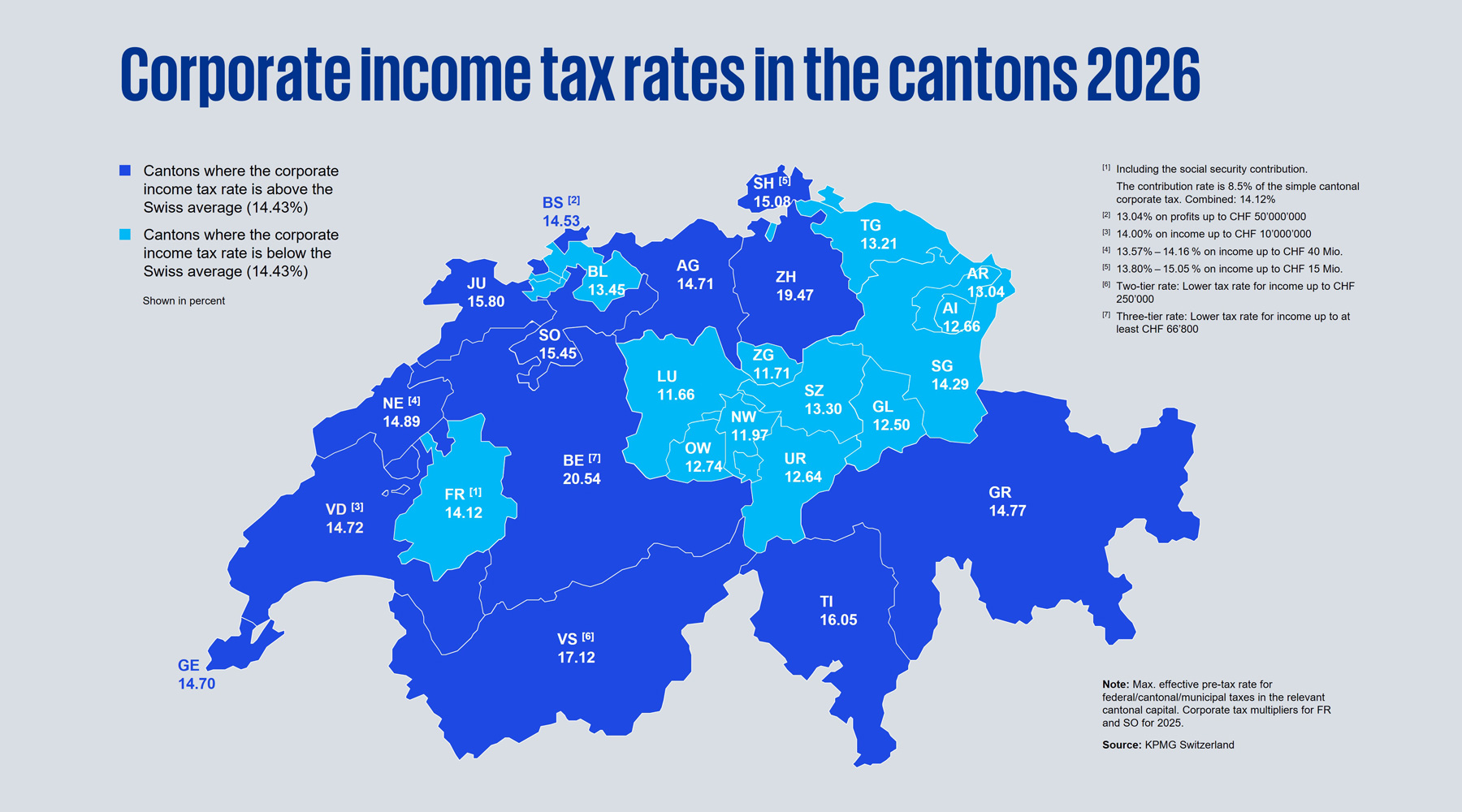

On average, corporate tax rates for businesses in Switzerland increased slightly year over year – from 14.40 percent to 14.43 percent.

A corporate tax rate cut sees Lucerne pull ahead of Zug as the canton with the lowest tax rate, reclaiming the top position for the first time since 2019.

Further amendments to the global minimum tax, most notably in connection with the side-by-side system used by the US, pose risks for Switzerland as a location.

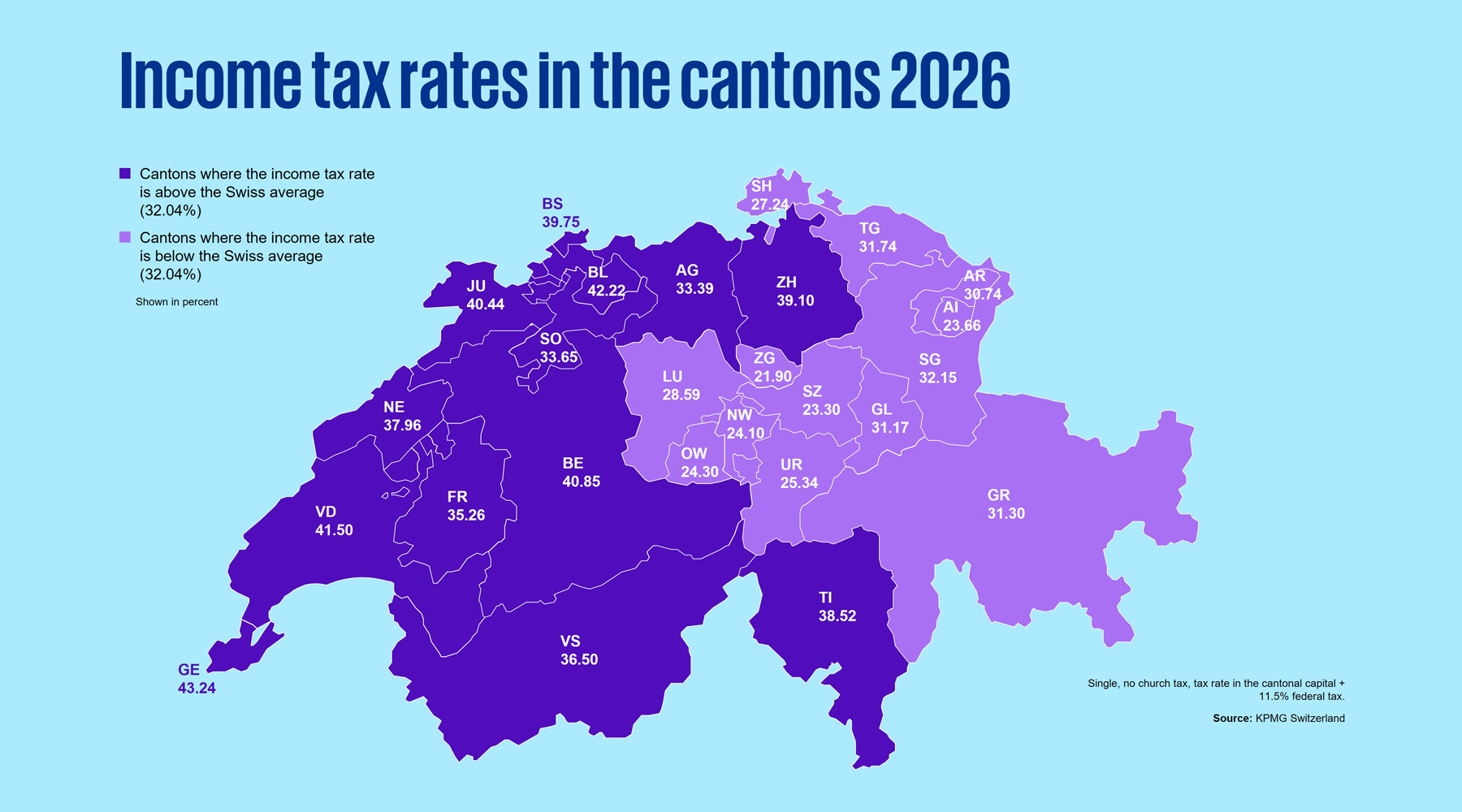

The average top tax rates for private individuals fell slightly, from 33.15 to 33.04 percent, compared to 2025.

Switzerland would like to protect its tax base and ensure compliance with the international tax framework by implementing the global minimum tax. At the same time, it competes for investment with countries like the United States that have not yet implemented the OECD’s framework and instead apply a different set of tax rules. The special status conferred on the United States puts greater pressure on Switzerland as a location. These are some of the findings presented in KPMG’s Swiss Tax Report 2026, which compares corporate and income tax rates from more than 50 countries and all 26 Swiss cantons.

Corporate tax rates – cantons adapt

A clear international trend is emerging among ordinary corporate tax rates. While many countries – including Switzerland – have made substantial cuts in the past few years, the introduction of the global minimum tax has put a damper on this trend in low-tax jurisdictions like Switzerland. In fact, several cantons have now raised their corporate tax rates in order to protect their tax base.

After increases in Geneva and last year’s introduction of progressive rates in Schaffhausen and Vaud, Basel-Stadt has also temporarily raised the tax burden for large corporations from 13.04 to 14.53 percent on profits of over CHF 50 million. These amendments aim to shift the effective corporate tax rate closer to the minimum tax of 15 percent and thus reduce the top-up tax, 25 percent of which must be paid to the federal government.

Lucerne pulls ahead of Zug

Overall, Switzerland’s average corporate tax rate has remained largely stable compared to the previous year and stands at 14.43 percent in 2026; this is slightly higher than in the previous year (14.40 percent), with the increase mainly attributable to the corporate tax rate hike in Basel-Stadt.

After lowering its corporate income tax rate from 11.91 to 11.66 percent, Lucerne has advanced to first place in a cantonal comparison, overtaking Zug (11.71 percent), which now ranks second. The cantons of Bern (20.54 percent) and Zurich (19.47 percent) are ranked lowest.

Compared with other countries around the world, Switzerland taxes companies at a low rate, especially in Central Switzerland. Those cantons still rank higher than classic low-tax jurisdictions such as Ireland (unchanged) and Cyprus, which has raised its tax rate from 12.5 to 15 percent. Traditional offshore domiciles remain attractive, with some offering an ordinary corporate tax rate of 0 percent.

Fig. 1: Cantonal corporate tax rates for businesses at a glance

Fig. 1: Cantonal corporate tax rates for businesses at a glance

Erosion of location-based tax advantage

The abolition of tax privileges under the TRAF reform and implementation of the global minimum tax have largely eliminated Switzerland’s ability to differentiate itself through low tax rates. “Due to developments in the international corporate tax landscape, we’ve been observing a creeping erosion of Switzerland’s tax advantage over the past few years. Since the level of corporate tax rates is becoming less important, countries are increasingly turning to alternatives like tax credits and subsidies,” says Stefan Kuhn, Head of Tax and Legal at KPMG Switzerland.

The global minimum tax has changed the general conditions and prompted a few cantons – such as Grisons, Basel-Stadt, Zug, Lucerne and even Schaffhausen – to launch projects aimed at improving their cantons’ attractiveness as a location, especially through the introduction of tax credits and subsidies. Instruments of this nature are also being discussed in other cantons.

United States’ special status creates additional pressure

The US government explicitly spoke out against the OECD minimum tax in 2025 and negotiated a special arrangement with the OECD in early 2026. This compromise, also known as the side-by-side solution, excludes US corporations from central minimum tax instruments (Income Inclusion Rule (IIR) and the Undertaxed Profits Rule (UTPR)), while domestic minimum top-up taxes (DMTT) still apply.

This is likely to give US corporations a competitive edge and means that the existing US tax system will continue to be used alongside the OECD tax regime, resulting in two different tax regimes applying side by side. Good tax planning will allow US corporations to circumvent top-up taxes, even if they are taxed at a rate of less than 15 percent in the US or in a third country without a domestic top-up tax.

Since many US corporations have established operations in Switzerland, the side-by-side approach poses risks for the country as a business location. Over the medium term, US corporations could potentially restructure their operations, relocate parts of their activities abroad, or reduce – or even forgo – future investment in Switzerland.

Mitigating risks through location policy

Switzerland only has limited room for maneuver in the context of the OECD minimum tax. The OECD prohibits selective levying of the minimum tax exclusively on companies that would otherwise be subject to a top-up tax abroad but not on subsidiaries of a US corporation.

While the OECD’s newly adopted substance-based tax incentives represent a new instrument to prevent pure profit shifting and benefit countries that focus more strongly on substance, Switzerland – as a small domestic market with many international headquarters – is likely to benefit less than other countries.

“This means Switzerland must monitor international developments and continually reconsider whether to levy the national top-up tax or opt out of the OECD framework,” says Kuhn. Levying this tax may allow it to safeguard its domestic tax revenue, but it would also make Switzerland less attractive to US corporations. Choosing not to levy the national top-up tax, on the other hand, may boost the country’s attractiveness to US corporations, but Switzerland would also have to reckon with a tax base loss and legal uncertainties.

“To stay attractive, Switzerland should use the tax-related measures it has at its disposal to take targeted steps to boost its attractiveness as a location while also continuing to strengthen the non-tax-related conditions,” says Olivier Eichenberger, Corporate Tax expert.

Income tax rates decline slightly – major cantonal differences remain

Average income tax rates in Switzerland have dropped slightly, from 33.15 to 33.04 percent, compared to 2025. The biggest cuts were made in the cantons of Ticino (-0.96 percent), Aargau (-0.88 percent) and Zurich (-0.61 percent). While most cantons left their rates unchanged, there were also a few increases, such as in Jura (+1.44 percent) and Neuchâtel (+0.27 percent).

Geneva still has the highest top income tax rate. Despite the cut made in the previous year, the canton’s rate of 43.24 percent in 2026 is still higher than that levied by Basel-Landschaft (42.22 percent), Vaud (41.50 percent) and Bern (40.85 percent). The lowest tax rate is found in the Canton of Zug at 21.90 percent, followed by Schwyz (23.30 percent) and Appenzell Innerrhoden (23.66 percent). The place of residence can therefore still have a noticeable impact on high-income taxpayers.

Fig. 2: Income tax rates of Swiss cantons at a glance

Fig. 2: Income tax rates of Swiss cantons at a glance

For more information and the detailed study, please go to: www.kpmg.ch/swisstaxes

For further information, please contact:

KPMG Switzerland is a leading service provider in the areas of Audit, Tax & Legal, and Advisory & Consulting, with more than 2,600 employees. We operate in 10 locations throughout Switzerland and one in Liechtenstein. Our clients benefit from our tailored solutions and our strategic alliances with technology partners that support our audit and non-audit services alike. In the 2025 financial year, KPMG Switzerland generated net sales of CHF 561.6 million. We operate in 138 countries and territories with more than 276,000 partners and employees working in member firms around the world.