- Belgiums lowered reliance on gas-fired generation means wholesale electricity prices are less closely tied to gas, leaving the economy less exposed to higher and more volatile energy costs.

- Unemployment remains low by historical standards, pointing to a relatively tight labour market. This may support wage growth and provide a buffer to household incomes, helping sustain consumer spending despite rising costs.

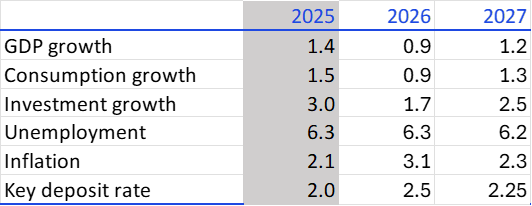

Belgian GDP growth is expected to slow slightly to 0.9% in 2026, down from 1% in 2025, as pressures from a new energy price shock push up inflation, weigh on spending and leads to potential further tightening by the Bank of England, according to KPMG’s latest European Economic Outlook.

Belgium’s growth rate is similar to the Eurozone’s average with Eurozone GDP forecast to grow by 0.9% in 2026 and 1.2% in 2027.

Europe is facing a renewed externally driven energy shock following disruption to the Strait of Hormuz, with higher energy prices and supply chain pressures expected to weigh on growth and push inflation higher across the continent.

Despite this backdrop, KPMG expects most European economies to avoid recession, with resilient labour markets and continued consumer spending helping support domestic demand through the remainder of the year.