The operating environment for banks is rapidly changing. Regulatory frameworks are evolving. Credit, liquidity and concentration risks are rising. And increasing geopolitical tensions and tariff pressures are amplifying the potential for volatility. In this environment, is your balance sheet an asset or a liability for your organization?

In today’s market where capital flows to efficiency and innovation, balance sheet inaction isn’t just a missed opportunity – it is a strategic liability.

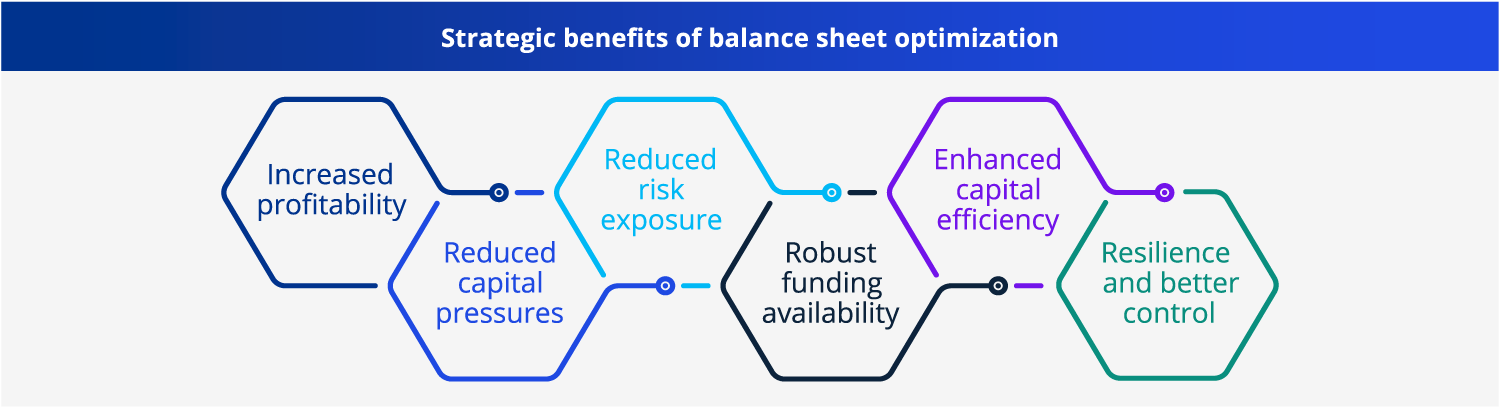

"Banks should be looking at balance sheet optimization not merely as a defensive tactic, but also as a strategic imperative for enhancing bank balance sheet performance and ensuring long-term resilience."

- Navigating uncertainty: The imperative of balance sheet optimization