AASB 9 Financial

There has been an increase in entities obtaining relief from their obligations under loan agreements. Whilst the relief can take many different forms, here we illustrate how a borrower accounts for a waiver of loan repayments.

Scenario

Company D has a loan from a bank with the following key terms as at their 30 June 2021 reporting date:

- carrying amount immediately prior to waiver is $1,000,000

- 3 years remaining on the loan

- monthly interest payments of $5,000 with $1,000,000 principal due on maturity

- effective interest rate of 6% p.a. (monthly interest of 0.5%).

In response to financial difficulties suffered during the COVID-19 pandemic, Company D secures a loan repayment waiver from its bank effective as at 30 June 2021. Under the terms of the waiver, interest payments for the months of July, August and September 2021 are waived. There is no payment to be made by Company D to compensate for the relinquished payments.

Questions

Interpretive response

Company D is released from the obligation to make payments for the months of July, August and September 2021 and as such the part of the loan relating to these payments is derecognised1.

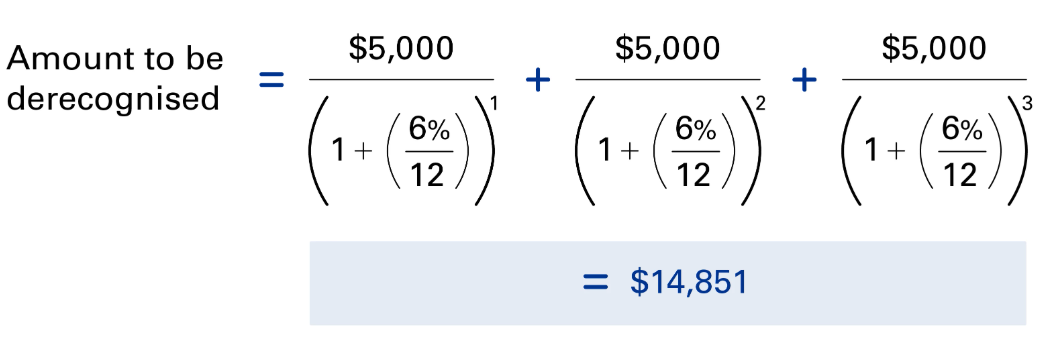

The part of the liability derecognised is calculated by discounting the forgiven cash flows at the original effective interest rate. This amounts to $14,8512.

The change in the carrying amount of the loan is recognised immediately as a gain in profit or loss.

This accounting applies whenever payments are waived, for example, interest only payments or payments of both principal and interest.

Footnotes

- Because this is a derecognition event, Company D does not assess whether the waiver represents a substantial modification of the loan.

- The change in the carrying amount is calculated as follows:

Getting technical

AASB 9 states that “an entity shall remove a financial liability (or a part of a financial liability) from its statement of financial position when, and only when, it is extinguished – i.e. when the obligation specified in the contract is discharged or cancelled or expires.” [AASB 9.3.3.1]

A creditor may forgive certain specifically identified cash flows of a financial liability with no amendment to the remaining cash flows or to any other instrument entered into with the creditor.

AASB 9 requires the difference between the carrying amount of the financial liability (or part thereof) that has been extinguished and the consideration paid to be recognised in profit or loss. [AASB 9.3.3.3]

Get in touch

More financial instruments Q&A

- How does a borrower account for a waiver of loan repayments?

- How does a borrower account for loan repayment holidays obtained during the COVID-19 pandemic?

- When do loan modifications result in derecognition?

- How does a borrower account for a modification to a prepayable fixed rate loan?

- What is the impact of modifying a floating rate loan?

- How do new costs and fees impact modification accounting?

- Does the effective interest rate change with non-substantial loan modifications?

- How does a borrower account for loan renegotiation costs?

- How are unamortised transaction costs accounted for on loan modification?