3 min read

Deal activity in Thailand remains vibrant despite the impacts of the Covid-19 pandemic. Key drivers in the financial services space include (1) Continued activity and transactions in payments, fintech and digital ecosystems, (2) Diversification of Thai corporations into the financial services sector, and (3) Funding activities of Asset Management Companies (“AMCs”) as they prepare for greater Non-Performing Loan (“NPL”) flows. We expect activity to remain robust as we start seeing the impacts of digital startups on the broader financial services sector and as banks rationalise their loan portfolios.

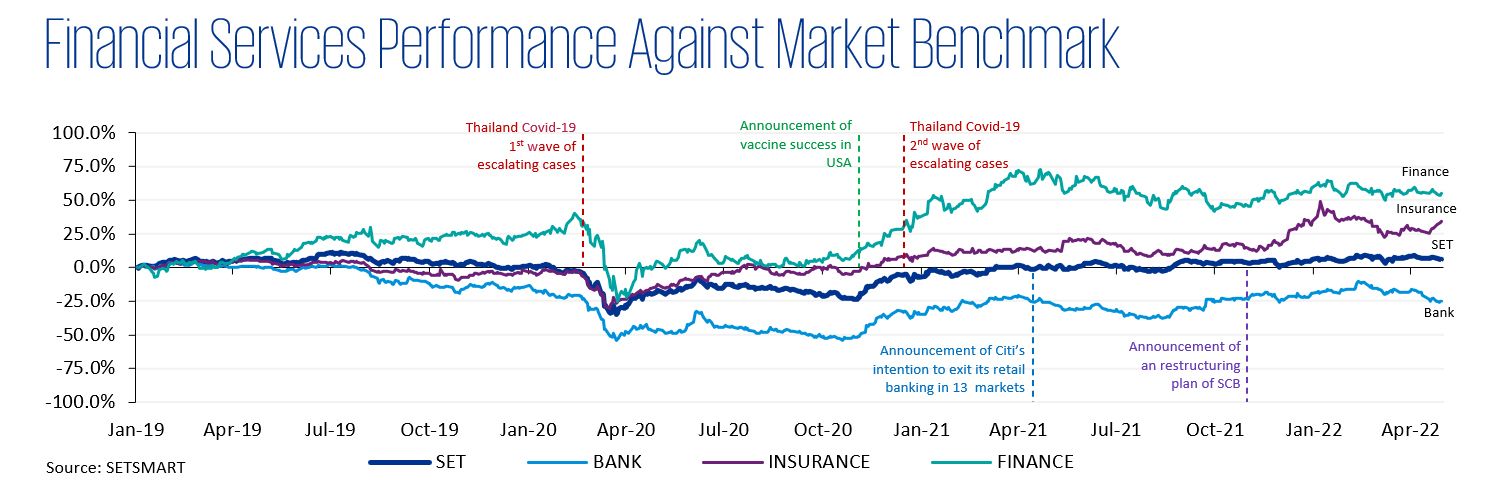

Banking

- Local banks continue to look outwards with Cambodia, Laos, Vietnam, and Indonesia being key markets of focus.

- Citi has reached an agreement to sell its Thai retail banking arm (alongside operations in Indonesia, Malaysia and Vietnam) to Singaporean bank UOB. This may drive further consolidation locally and regionally.

- Siam Commercial Bank has recently announced its “SCB Reimagined” plan to facilitate its transition into a tech driven company. The initiative is expected to drive new ventures and investments. The securities arm of the business is in advanced discussions to acquire a majority stake in digital currency exchange Bitkub (subject to shareholder and regulatory approvals) to support its transition into a Digital Assets broker and ICO portal.

- The BOT has published a consultation paper (February 2022) outlining its plans to reposition the financial sector. The principal policy recommendations include (a) Establishing a virtual banking license, (b) Removing limits on fintech investments by banking groups, and (c) Expanding the scope of NBFI and allowing them access to core infrastructure.

Consumer Finance

- Asset yields have experienced downward pressure stemming from a reduction in regulatory interest caps and softer economic conditions. However, operators with sufficient scale continue to record strong performance.

- Continued consolidation and partnerships (for example, with insurance companies) are key deal themes. The recently announced policy direction of the BOT indicates expansion of the scope of Thai consumer finance businesses.

- Several recent IPOs underscore investor appetite in the space (Ngern Tid Lor, Heng Leasing and Capital, Saksiam Leasing). There have been several transactions for entities holding licenses as investors see consumer finance as an attractive and cost effective entry point into the Thai financial services sector.

Insurance

- Both the insurance and broker segments have seen continued deal activity. Within non-life, health insurance has been a key area of focus (for example, the acquisition of Aetna Thailand by Allianz Ayudhya Capital)

- Partnerships have been a key driver of deals and insurers seek to tap the customer ecosystems of other financial and non-financial businesses to enhance distribution and customer value proposition.

- Life insurance licenses remain sought after with several recently completed acquisitions (for example, Manulife by King Wai Group, and Advance Life Assurance by U City).

- Brokerage businesses are increasingly digitally focused. Larger brokers (such as TQM) have been expanding regionally through deals.

Payments/Fintech/Crypto

- BOT’s consultation paper on the financial sector reiterates the central role of fintech in the Thai financial services sector.

- Investments in the space continue to grow, with completed funding rounds in Ascend Money (e-money, wallet and payments) and Sunday Ins (a digital non-life insurer) topping the 2021 list.

- SCB’s announced deal for Bitkub is slated to become the largest transaction to date in the space on closure.

Asset Management (NPLs and fund management)

- The Asset Management sector has seen a significant uptick, with increasing deleveraging by banks.

- AMCs have been increasingly active in the fund raising market, raising both equity and debt.

- The BOT has encouraged Banks to explore Asset Management JVs to facilitate an orderly deleveraging of their balance sheets. Various tie-ups (such as Banks and AMCs, and AMCs and Corporates) are under discussion, with some having closed recently as the sector prepares for increased NPL flows.

- Based on Bloomberg news, KBANK is considering strategic alternatives for KAsset (estimated valuation of USD 2.0 bn).