This article was first published in the Q3 2023 issue of the SID Directors Bulletin published by the Singapore Institute of Directors.

Within a span of 14 years, Bitcoin has grown from a niche product to a financial asset class on its own. Created after the Global Financial Crisis in 2009 and leveraging blockchain (a type of distributed ledger technology), Bitcoin was the world’s first decentralised digital currency.

Bitcoin is a cryptocurrency, a virtual currency designed to act as money and a form of payment outside the control of any one person, group, or entity – thus removing the need for thirdparty involvement in financial transactions. It has become so mainstream that several large institutions and retailers accept Bitcoin as payment for goods and services.

Although proponents of Bitcoin tout it as a safer, long-term alternative to banks and traditional currencies, the lack of clear regulations around the digital asset has led to traditional players approaching it with apprehension. Meanwhile, cryptocurrency enthusiasts have been driving developments at a breakneck speed in this space. Although the digital asset sector has experienced volatility in recent years, it has expanded rapidly. According to a report in CNBC, the digital asset market reached a record-high US$3 trillion (S$4 trillion) market capitalisation in late 2021. Subsequently, the digital asset market saw a decrease of over US$2 trillion due to rising interest rates and some high-profile digital asset incidents. Even so, in Fidelity Digital Assets’ 2022 Institutional Investor Digital Assets Study, 74 per cent of 1,052 institutional investors surveyed indicated plans to buy or invest in the space in the near future.

As a nascent technology that is increasingly reshaping the financial markets, directors on boards may need to think about the potential implications of digital assets for their organisations. What do they need to consider when venturing into the market for digital assets, whether for investment or integration into business models?

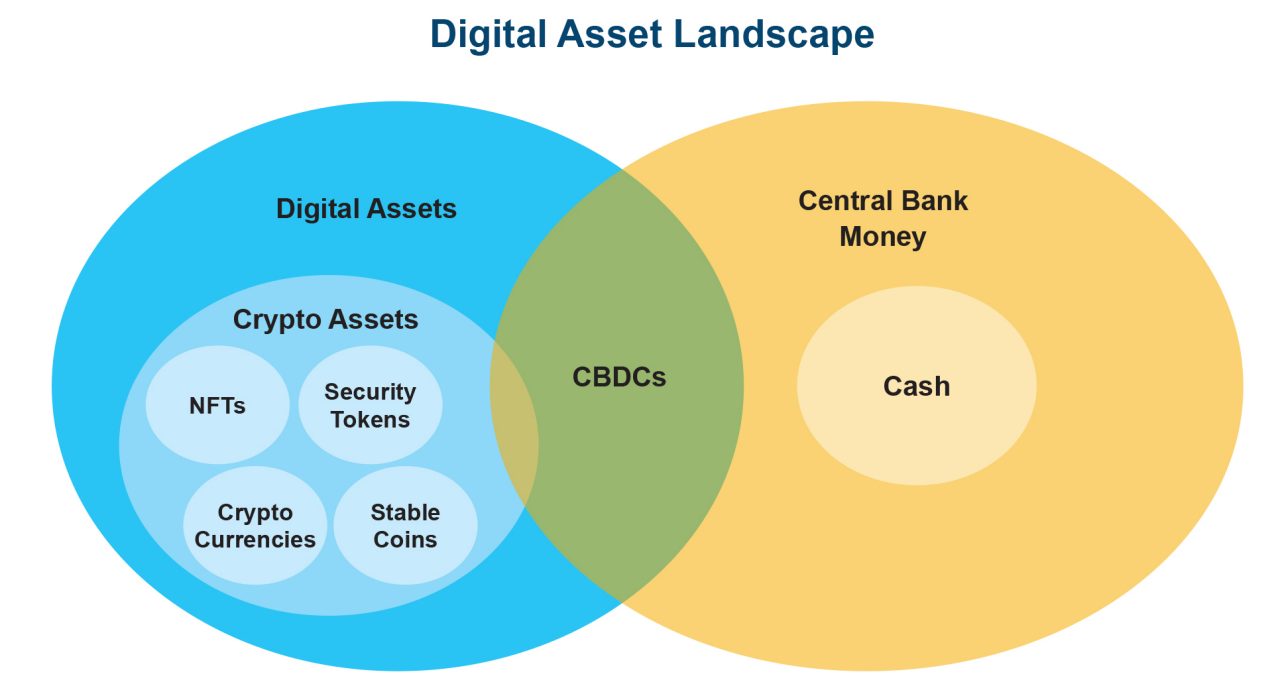

Digital asset landscape

While cryptocurrencies are one of the most widely-known use cases of blockchain technology, other sub-categories of blockchain- based digital assets have emerged over the years.

Other than cryptocurrencies like Bitcoin and Ether, physical assets such as art, real estate or securities have also been tokenised through the use of blockchain. Today, cryptocurrencies are just one part of the entire digital asset ecosystem.

Terminologies such as “stablecoins” and non- fungible tokens have made their way into the modern-day lexicon and are often used interchangeably to describe digital assets. See box “Types of Digital Assets” for those built on blockchain.

The box “Digital Asset Landscape” illustrates the types of digital assets and how they fit together in today’s business landscape.

- Stablecoins. These are virtual digital assets with a value pegged to a real-world fiat currency like the US dollar or Singapore dollar. Stablecoins are usually managed by private enterprises. They typically maintain a reserve of fiat currency or a portfolio of underlying assets equal to the token’s circulating supply. They provide a stable exchange value, typically at a 1:1 ratio to a fiat currency. Some of the more well[1]known stablecoins include Tether and USD Coin.

- Central bank digital currency (CBDC). Similar to stablecoins in terms of the underlying concept, CBDC governing authorities are different. While private enterprises manage stablecoins, CBDCs are a new type of digital money issued by central banks as an alternative to physical money. CBDCs typically do not have any assets backing them, except that their value is fixed by the issuing central bank and is thus equivalent to the country’s fiat currency. Wholesale CBDCs are primarily used for institutional trade finance, while both consumers and businesses use retail CBDCs to facilitate payment transactions.

- Non-fungible tokens (NFTs). Representing ownership of a unique digital item, an NFT is a certificate that authenticates ownership of a virtual asset, similar to a physical deed poll. NFTs are used in inventory management and digital identities, popularised in the art and music world. In business, NFTs are more commonly used in supply chain management, where the technology is applied to track and trace every stage of the supply chain, from procuring raw materials to the final point of sale. This can provide valuable insights for businesses looking to refine their supply chains.

- Security tokens. These allow assets such as stocks or real estate to be broken up into virtualised tokens. This makes them more accessible to retail investors and increases the liquidity of these assets.

- Cryptocurrencies. In general, cryptocurrencies represent any digital store of value and can serve as a medium of exchange stored on the blockchain. This includes Bitcoin, Ethereum and Binance Coin.

Source: Q3 2023 SID Directors Bulletin by the Singapore Institute of Directors

Popularity

The proliferation of blockchain technologies and the growing interest in digital assets are driving the development of Web 3.0. In the next phase of the internet, it is envisaged that users will be increasingly connected and have access to their data over a decentralised network.

In Web 3.0, users have ownership rights over the content they have created and the digital assets they have purchased. All asset ownership information is stored on public blockchains, making these assets “portable” and even transferable. The value of these assets can be stored, verified and transacted independently of third parties.

Although recent headlines have highlighted the challenges faced by some stablecoins and the collapse of well-known crypto exchanges, interest in digital assets continues to grow. This enduring enthusiasm can be attributed to the immense potential of digital assets in transforming the financial and technology landscape. As a result, the adoption of digital assets continues to be an exciting prospect for many.

Demand for digital assets is growing not just among private individuals but also among family offices and institutional investors. A 2022 study by KPMG China and Aspen Digital found that most family offices and high net worth individuals in the countries surveyed indicated an interest in digital assets.

Asset recovery

The volatility in the value of digital assets continues to be a key concern for institutions and investors. Although blockchain technology is designed to be more secure and resistant to attacks due to its decentralised and distributed structure, it is not entirely immune. Research by blockchain data platform Chainanalysis estimated that approximately US$3.8 billion worth of cryptocurrency was reportedly stolen worldwide in 2022.

While the blockchain is a shared, immutable, fully transparent ledger, recovering stolen digital assets can be difficult. Tools like crypto mixers combine transactions on the blockchain to facilitate anonymous transactions, making it nearly impossible to trace these digital assets.

Moreover, not all exchanges obtain customer information or respond to requests for information on the customer, which can complicate investigations. Even if the wallet is traced, there is a possibility that the jurisdiction may have data privacy rules or is unable to supply information about the final location of the digital asset.

Given these challenges, taking steps to prevent attacks is critical, especially in securing client confidence for organisations and businesses dabbling in cryptocurrencies.

Role of directors

Despite the risks above, the use of blockchain technology and digital assets continue to increase because of the potential to improve efficiency, convenience and transparency of processes.

For example, digital assets can streamline operations by improving data collection, cutting out intermediaries and increasing the liquidity of assets. NFTs, blockchain, smart contracts and cryptocurrencies are also seen as a big game- changer as society moves towards virtual reality.

Digital assets are becoming increasingly ingrained in the world we live in, especially as we move into the next internet era, and these developments will fundamentally transform business models across sectors. Business leaders will ultimately need to understand how their organisations should adapt and evolve as these technologies and digital assets transform industries and consumer behaviour. The board of directors, especially, plays a crucial role in the following areas.

As crypto and digital assets gain widespread acceptance, directors need to assess how these may impact their existing strategies, from operational matters to risk and regulatory matters. Management should provide the board with timely, detailed information on product and market developments, including identifying and assessing current and emerging risks, such as cyber threats.

The board should establish clear policies and procedures for investing in digital assets. Investment policies should include guidelines around risk tolerance, types of assets suitable for the company’s strategy and how the risks will be managed. Given that supply and demand are driving the value of digital assets, boards will need to articulate and be firm about their risk tolerance for these volatile assets.

The board should thoroughly review all decisions related to digital assets and ensure they align with the company’s policies and objectives. The board has to assess and decide on the need to establish or enhance internal risk policies, processes, procedures and controls for digital assets and payments, such as customer due diligence, anti-money laundering and counter-terrorism financing programmes.

Investing in digital assets can be risky, so the board of directors should work closely with the company’s executive team to identify and manage those risks. This includes staying current with regulatory changes, assessing capabilities, developing risk and compliance frameworks around digital assets, and ensuring that the company’s investments are diversified. In addition, digital asset companies and their customers are prime targets for cyber criminals.

Investing in digital assets can be subject to a variety of regulatory requirements. The board of directors should work with the company’s legal and compliance teams to ensure all investments comply with applicable laws and regulations. What are the regulatory and tax implications of engaging with digital assets and blockchain technology? This is especially important for global companies based in multiple jurisdictions, all with their own set of regulations for digital assets.

The board has a responsibility to communicate the company’s digital asset strategy to shareholders. The strategy should include clear action items, processes and the chain of command, especially in times of crisis. It also includes providing regular updates on the company’s investments in digital assets, including any gains or losses.

In summary, the board of directors has a critical role in overseeing a company’s strategy in digital assets. By setting clear policies, managing risk, ensuring compliance, communicating with shareholders and maintaining confidentiality, the board can help ensure the company’s investments in digital assets are secure. When handled with care and appropriate due diligence, digital assets have a high potential to generate good returns and can be aligned with the company’s broader objectives.

The authors are from KPMG Singapore. Antony Ruddenklau is Head of Financial Services, and Tea Wei Li is Partner, Governance, Risk and Compliance.

Related content

Our people

Antony Ruddenklau

Partner, Head of Financial Services, Global Head of Fintech and Innovation, Financial Services, KPMG International and Head of Payments, Asia Pacific

KPMG in Singapore