Introduction

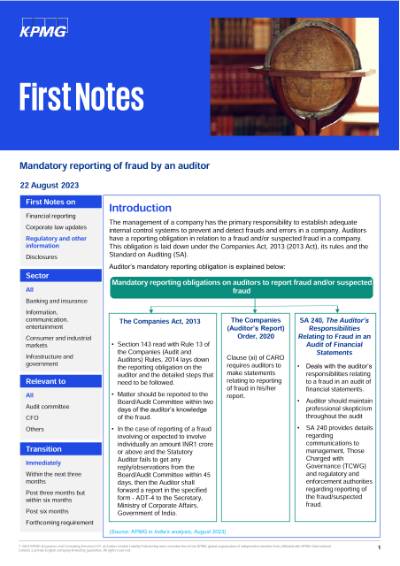

The management of a company has the primary responsibility to establish adequate internal control systems to prevent and detect frauds and errors in a company. Auditors have a reporting obligation in relation to a fraud and/or suspected fraud in a company. This obligation is laid down under the Companies Act, 2013, its Rules and the Standard on Auditing.

New Development

On 26 June 2023, the National Financial Reporting Authority (NFRA) issued a circular (the Circular) to clarify the responsibility of statutory auditors in relation to reporting of fraud in a company.

Some important clarifications from the circular are as follows:

- Mandatory obligation to report fraud by an auditor

- Procedure to report fraud by an auditor

- Auditor not being the first person to identify the fraud

- Resignation by an auditor

- Professional skepticism

In this issue of First Notes, we aim to provide an overview of the above mentioned clarifications provided by NFRA.

To access the text of the NFRA’s circular, please click here.

You can reach us for feedback and questions at aaupdate@kpmg.com.