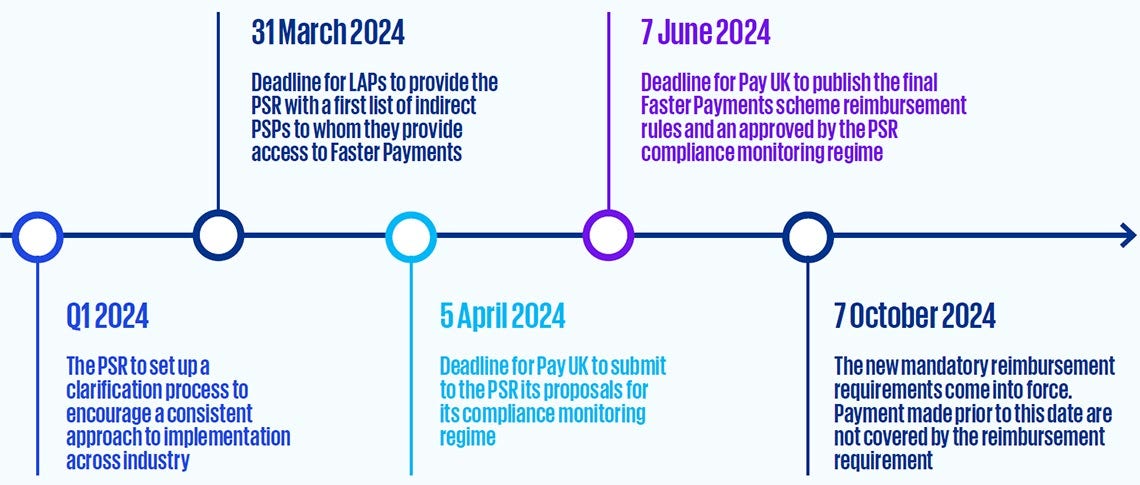

What does the APP legislation mean for PSPs?

The UK’s Financial Conduct Authority (“FCA”), defines a vulnerable customer as “somebody who, due to their personal circumstances, is especially susceptible to harm, particularly when a firm is not acting with appropriate levels of care”. The FCA outlines four categories of vulnerability in its determination, namely, health, life events, resilience and capacity.

Under the new legislation, reimbursement will be extended to various participants:

- Consumers (those acting for purposes other than trade, business, or profession).

- Micro-enterprise (with less than 10 employees and annual turnover and/or annual balance sheet less than £2m).

- Charities (with annual income less than £10m).

Exceptions arise when victims are complicit in the fraud or have demonstrated gross negligence. Sending PSPs can extend reimbursement windows when additional information is necessary for claim assessment, and they have the flexibility to implement a maximum reimbursement level, apply a claim excess, and set time limits, with a minimum of 13 months.

The legislation promotes additional supports for vulnerable customers, especially in the context of assessing whether gross negligence was a contributing factor to the loss. This signals the continuing move to protect such customers, requiring a heightened awareness by financial institutions of consumers’ personal circumstances.

With the ongoing consultation of the Consumer Protection Code and an updated and modernised Code on the way, it is likely that similar legislation may be introduced in Ireland. PSPs in Ireland can look to the UK to build a framework which can proactively address similar regulation should it be introduced here in the coming years.