The significance of the EBA prudential transition plan in the financial sector

In recent years, environmental, social and governance (ESG) considerations have gained increasing prominence in the financial sector. Climate change, societal expectations, and regulatory pressure all encourage institutions to view these dimensions not only as a business opportunity but also as sources of potential risk.

In our August FRR newsletter, we already highlighted that the EBA’s new Guidelines on the management of ESG risks – EBA/GL/2025/01 – set out detailed requirements for the identification, measurement, management and monitoring of risks, as well as for the development of transition plans. In this newsletter, we take a closer look at the content requirements, legal basis and practical application of the prudential transition plan (CRD transition plan).

The requirement for prudential transition plans is set out in the Capital Requirements Directive (CRD VI, (EU) 2024/1619). The management body bears responsibility for drawing up and monitoring a comprehensive transition plan, which must contain quantifiable targets and intermediate milestones for identifying, managing and monitoring the short-, medium- and long-term financial risks arising from ESG factors. According to Article 87a CRD VI, national competent authorities – in Hungary the MNB – will be required to assess the “robustness” of such plans in the context of the SREP, i.e. their effective integration into the risk management framework.[1] During this assessment, the supervisor will examine, inter alia, the institution’s sustainability-related product offering, transition finance policies, loan origination practices, as well as ESG-related targets and limits.

At the core of the prudential transition plan are the institution’s strategic objectives, which must be consistent with EU and national climate policy targets – including the Union’s commitment to achieve Net Zero 2050. The plans must:

- be structured along short-, medium- and long-term horizons,

- contain quantifiable targets, milestones and indicators,

- apply scenario-based analyses modelling the impact of physical and transition risks over at least a 10-year time horizon,

- at governance level, ensure management body oversight and a control framework organized along the three lines of defence,

- and be fully integrated into the ICAAP and ILAAP frameworks.

Section 6.4 of the EBA Guidelines sets out the key elements of the plan in detail, while the Annex provides a supporting table with examples and possible indicators. Although flexible in their application, these elements often serve as de facto benchmarks for supervisory assessment.

In practice, a prudential transition plan is not a template document but requires institution-specific approaches:

For large commercial banks, the focus is on portfolio decarbonization, adjustments of lending policies, and the development of green financial products.

For credit institutions specialising in SME financing, simplified ESG monitoring systems – for example, proxy-based approaches – may be appropriate.

For smaller institutions, the EBA Guidelines provide for proportionality, including simplified content requirements.

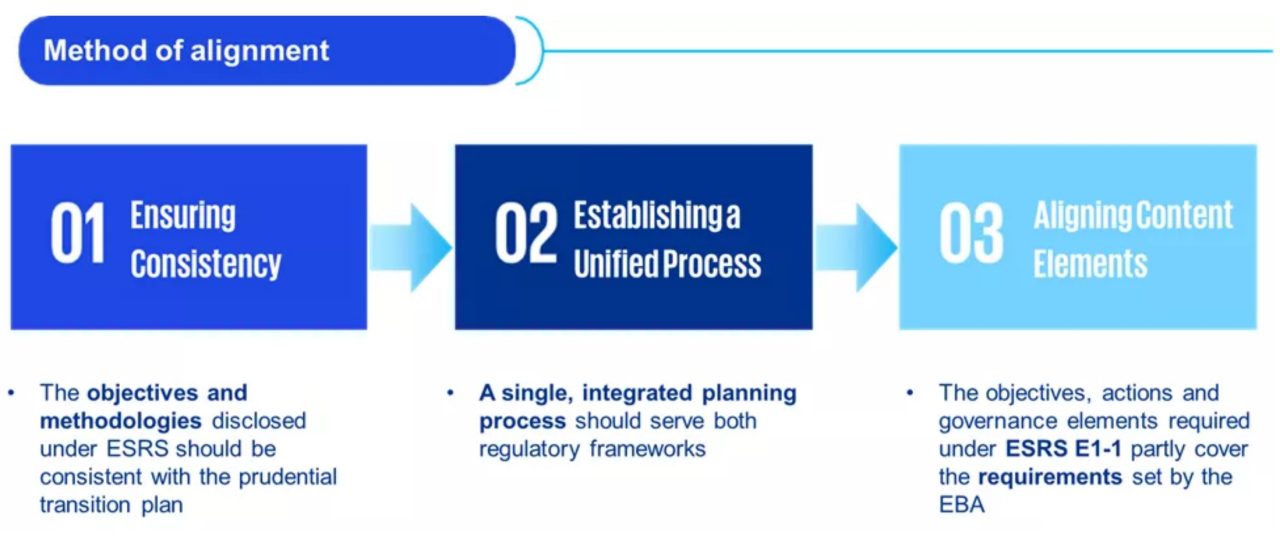

The prudential transition plan is not a public document. However, certain elements – particularly objectives and metrics – may overlap with sustainability reporting obligations under the CSRD, such as climate-related disclosures under ESRS E1-1.