This issue of InfoCourier covers the following topics:

- Deferral of deadlines for reporting cross-border arrangements

- Amendments to the Aliens Act, the Higher Education Act and the Study Allowances and Study Loans Act

- Summaries of court judgments: Failure to declare VAT on sales

Please feel free to contact KPMG’s tax advisers with any queries you may have.

We hope you are enjoying reading it!

Deferral of deadlines for reporting cross-border arrangements

An amendment to the Tax Information Exchange Act entered into force in January 2020, transposing the revised EU Directive on Administrative Cooperation into the Estonian law. With the revised directive, EU member states agreed on mandatory automatic exchanges on certain tax arrangements to increase the transparency of tax planning.

As a rule, the information must be reported by tax advisers or other persons who have provided the services related to the reportable arrangement. In some circumstances, however, the reporting obligations may fall on the client or the taxpayer instead.

Information must be disclosed about three types of cross-border arrangements:

- arrangements with potential implications for taxation;

- arrangements that may help to avoid exchange of information on financial accounts;

- arrangements that may help to hide ultimate beneficial owners.

An arrangement is reportable if it meets at least one of the criteria established by the regulation of the Minister of Finance. Another regulation provides a list of information that must be disclosed to the tax authority.

It is important to note that the reporting obligation relates to direct taxes (primarily income tax). Value-added tax, custom and excise duties, social security contributions and state fees fall outside the scope of the Directive and the Tax Information Exchange Act.

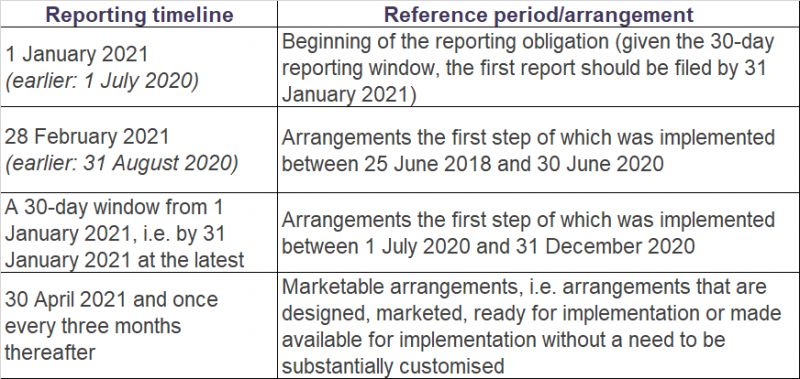

The Act initially provided that reporting was to begin on 1 July 2020, and for arrangements implemented between 25 June 2018 and 30 June 2020, the reporting deadline was 31 August 2020. Under EU Directive 2020/876, however, certain deadlines for the filing and exchange of information were deferred because of the COVID-19 pandemic. On 12 November 2020, the Riigikogu similarly adopted amendments to the Tax Information Exchange Act, deferring the reporting deadlines by six months.

More information on amendments to Tax Information Exchange Act is available here (in Estonian).

Further information: Tax Advisor Ave Rego averego@kpmg.com

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia

Amendments to the Aliens Act, the Higher Education Act and the Study Allowances and Study Loans Act

A bill on amending the Aliens Act, the Higher Education Act and the Study Allowances and Study Loans Act passed the first reading in the Riigikogu at the end of October. The proposed bill would tighten the terms on which non-EU nationals can stay, study and work in Estonia.

If the bill becomes law, third country nationals can engage in short-term employment only if they have been issued a long-term visa (“D” visa). Family members of those in short-term employment will no longer be issued a visa on the same terms.

New minimum wage requirements will be set for foreign nationals engaged in seasonal work, who must receive a wage corresponding to at least the average gross monthly wage in Estonia (according to the most recent data published by Statistics Estonia) in the sector, based on the Estonia Classification of Economic Activities (EMTAK). The wage paid for unskilled seasonal work should correspond to at least 80 percent of the average gross monthly wage for that sector. The length of period during which a seasonal worker can work in Estonia is also reduced (temporarily until 30 April 2022) to 183 days within a period of consecutive 365 days (now: up to 270 days).

Regulations concerning stays for study purposes will also be tightened. According to the bill, the family members of foreign nationals who take up studies in Estonia may no longer be issued long-term visas, with the exception of the family members of doctoral students. The spouse of third country students with temporary residence permits may not be granted a residence permit earlier than two years after the beginning of studies.

More information on the bill amending the Aliens Act, the Higher Education Act and the Study Allowances and Study Loans Act is available here (in Estonian).

Further information: Tax Advisor Einar Rosin erosin@kpmg.com.

Summary of court judgments

Summary of District Court judgment in administrative matter no. 3-19-1890 (15 September 2020).

Payment of personal expenses out of company accounts

The district court agreed with the tax authority’s position, expressed earlier in administrative matter no. 3-16-2055, that the refurbishment, furnishing and gardening expenses associated with a house and lot recorded on the company’s accounts and tax records are unrelated to the company’s business and the taxable turnover, as these expenses have been incurred for the benefit of a member of the board (and shareholder) of the company and the family members of the board member. The court also upheld the tax authority’s view that the expenses which, by agreement between the parties, were offset against lease payments payable to the board member, should be considered lease payments and thus subject to tax. The board member also run other personal expenses through the company accounts, which increased the financially measurable benefit for the board member (and shareholder), i.e. the value of the house and lot, while reducing the value of the company’s assets. The court agreed with the tax authority’s position that these expenses should be classified as dividend distributions.

The tax authority made a liability decision addressed to the board member responsible for the tax arrears. Rejecting the claim for the revocation of the liability decision (administrative matter no. 3-19-1890), the court pointed to several significant facts and circumstances:

- If a legal representative of the company has caused tax arrears intentionally or as a result of gross negligence, they will be held liable, jointly with the company, for this part of tax arrears.

- As regards the intentionality of the board member’s conduct, the court found that intent can be established in this case mainly based on subjective elements, i.e. awareness of the unlawfulness of the conduct and the will to bring about an unlawful consequence. The main factor pointing to intent was the fact that the claimant had sole control over the company during the period when tax arrears were incurred.

- As the tax arrears were a result of an intentional act on the part of a member of the board, the five-year time limit applies for making a tax assessment.

- Using the services of a professional accountant increases the plausibility of the assumption, on the part of the board member, that accounting is carried out in an accurate and compliant manner and does not require constant attention and oversight. It does not, however, relieve the board member from the obligation to be informed about the company’s accounts, even though it does not fall within the board member’s scope of responsibility.

More information on the judgment is available here (in Estonian).

Further information: Tax Advisor Ave Rego, averego@kpmg.com