The Court held in a recent case that the taxpayer should be refunded of the excessive tax reserve certificates (TRCs) purchased together with interest despite the final determination of the taxpayer’s appeal in the case is pending. In this news alert, we summarise the Court’s analysis and discuss our observations from the case.

Summary

Background

The Court of First Instance (CFI) handed down its judgement in Besins Healthcare (Hong Kong) Limited v Commissioner of Inland Revenue1 on 28 September 2022.

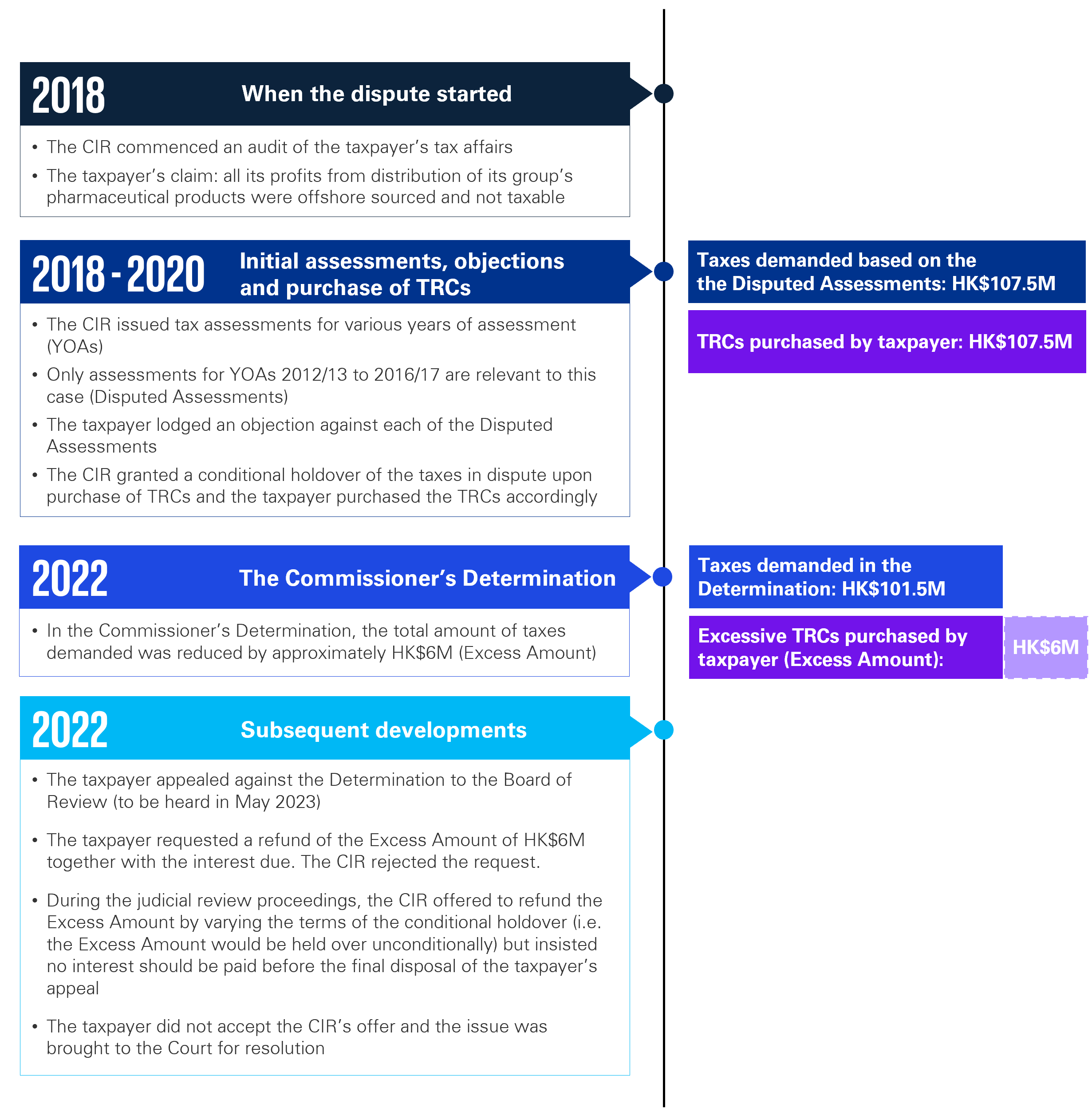

The case concerned a judicial review initiated by the taxpayer on the Commissioner of Inland Revenue (CIR) refusal to refund a sum of approximately HK$6 million (Excess Amount) to the taxpayer. The amount represented excessive TRCs purchased by the taxpayer as a result of a subsequent downward adjustment made by the CIR in his Determination of the taxpayer’s objection. Please refer to the diagram in the Appendix for the key facts of the case.

The issues in dispute

The key issues in dispute are:

- Illegality – whether the CIR has the power to refund or repurchase TRCs under section 71(7)(d) of the Inland Revenue Ordinance (IRO)2 before the substantive tax appeal is finally determined; and

- Irrationality – whether it is unreasonable and/or irrational for the CIR to retain the Excess Amount where there is no principled basis to do so and given he is empowered to vary the terms of the holdover of tax under section 46 of the Interpretation and General Clauses Ordinance (IGCO)3.

The CFI’s judgement and analysis

Below is a summary of the Court’s analysis and comments:

On the issue of illegality:

- The same approach should apply to both the principal of the excess TRCs purchased and any interest accruing on it.

- The phrase “final determination of the objection or appeal” refers to the single endpoint of the process comprising an objection and an appeal under the IRO. This means the single endpoint of the objection (if there is no valid appeal) or the objection and the appeal (if there is a valid appeal). The determination of an objection is not the “final determination” if there is an appeal.

- Therefore, it is not illegal or contrary to the IRO for the CIR to refuse redeeming or refunding the Excess Amount and any accrued interest under section 71(7)(d) of the IRO.

- On the other hand, the CIR has a discretionary power to vary his original holdover order (i.e. cancel, suspend, amend or substitute any holdover order made) as required.

On the issue of irrationality:

- Although the Commissioner’s Determination is not the final position of the case and taxes in excess of the amount demanded in the Determination may potentially be raised by the Board of Review, the Determination reflected the CIR’s view that the Excess Amount is simply not tax payable at the current stage.

- Section 46 of the IGCO permits the CIR to make the necessary amendment to the initial holdover order. It is therefore unreasonable and/or irrational for the CIR to retain the Excess Amount given he conceded himself that he should never have had those funds. It also seems obviously irrational for the CIR not to pay interest at the same time as refunding the principal amount.

The CFI therefore ordered the CIR to (1) vary the terms of the original holdover order (i.e. the HK$6M should be held over unconditionally) and (2) refund the principal sum of HK$6M together with the accrued interest within 21 days.

KPMG observations

This case illustrates that when judicial review proceedings on tax matters are brought to the Court, it is not only the proper statutory interpretation of the material provisions in the IRO that matters. Considerations also need to be given to whether the acts of the Inland Revenue Department (IRD) result in sufficiently serious “unfairness” or “unreasonableness” to taxpayers that justifies judicial interference.

Another potential unfairness to taxpayers in the current objection and appeal process in Hong Kong highlighted by the CFI in its judgement is the huge disparity between the interest rate on TRC payable by the CIR (i.e. currently at 0.175% per annum) and the interest rate on judgment debts payable by taxpayers (i.e. currently at 8% per annum).

Taxpayers with similar situation as in this case (i.e. the tax demanded in a notice of assessment under objection is subsequently adjusted downwards in the Commissioner’s Determination but TRC based on the higher amount demanded in the assessment has been purchased) should consider whether a request for refund of the excessive TRC purchased together with the accrued interest should be made in light of the CFI judgement in this case.

In addition, taxpayers having long outstanding tax disputes with the IRD should explore effective strategies for early settlement of the cases to minimise the financial impact arising from the requirement to purchase TRC (in case of a conditional holdover) or the interest payable upon withdrawal of or failure in the objection or appeal (in case of an unconditional holdover). KPMG has a team of tax experts specialised in tax controversy services who can help to resolve tax disputes on a timely manner and a “win-win” basis.

Key facts of the court case

- The CFI judgement can be accessed via this link: https://legalref.judiciary.hk/lrs/common/ju/ju_frame.jsp?DIS=147562&currpage=T

- In essence, section 71(7)(d) of the IRO states that upon the final determination of the objection or appeal, and after all tax held over which becomes payable has be paid, for any certificate so purchased that has not been accepted as payment, the CIR must repay to the holder of the certificate (i) the principal value represented by the certificate and (ii) the interest on that value.

- Section 46 of the IGCO confers power upon any person to make, grant, issue or approve any proclamation, order, notice, declaration, instrument, notification, licence, permit, exemption, register or list, such power shall include power (a) to amend or suspend, (b) to substitute, (c) to withdraw approval of and (d) to declare the date of the coming into operation, and the period of operation, of such proclamation, order, notice, declaration, instrument, notification, licence, permit, exemption, register or list.

The Court held taxpayers are entitled to refund of excessive tax reserve certificates purchased plus interest in unsettled tax dispute cases

Hong Kong Tax Alert - Issue 19, October 2022