The existing CBA regime

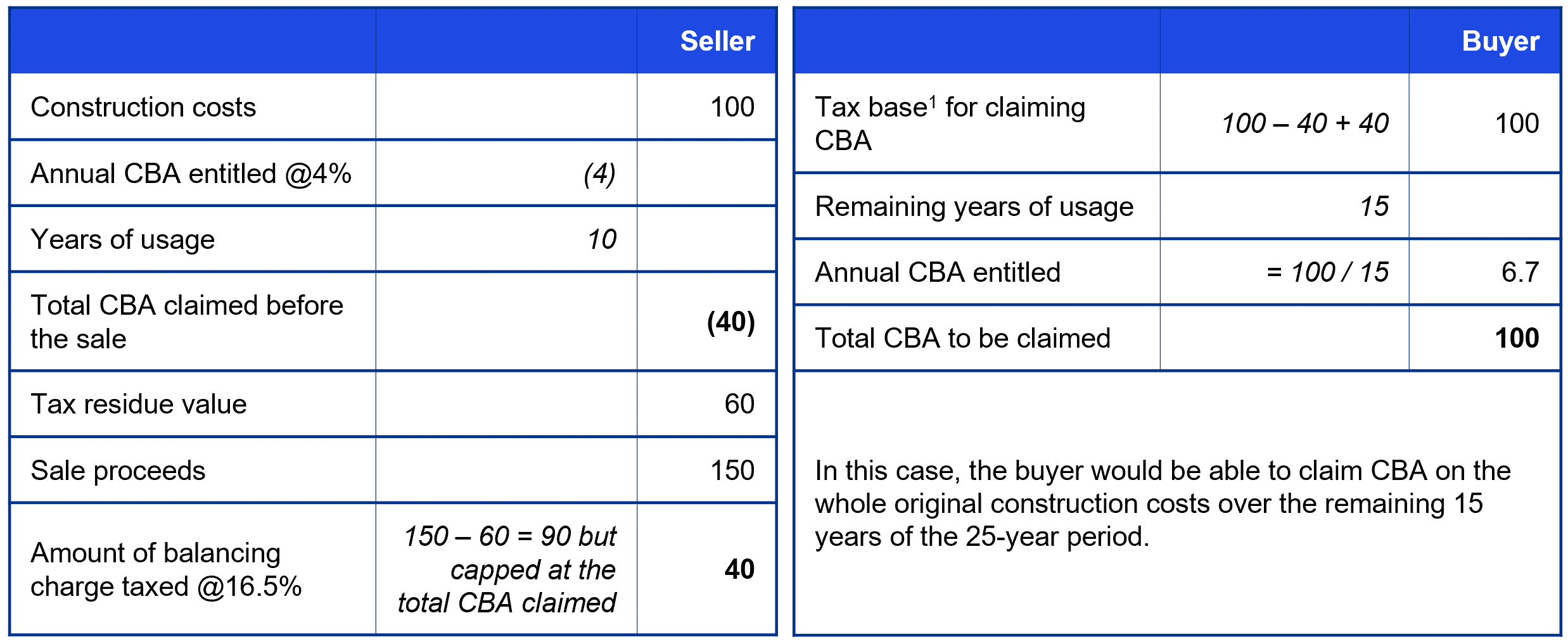

Under the current CBA regime, annual allowances at 4% of the construction costs of a commercial building are granted to Hong Kong taxpayers as a tax relief for the construction costs incurred. The annual allowances can be claimed by taxpayers over a maximum period of 25 years starting from the YOA in which the building was first used or YOA 1998/99 (for commercial buildings constructed prior to YOA 1998/99).

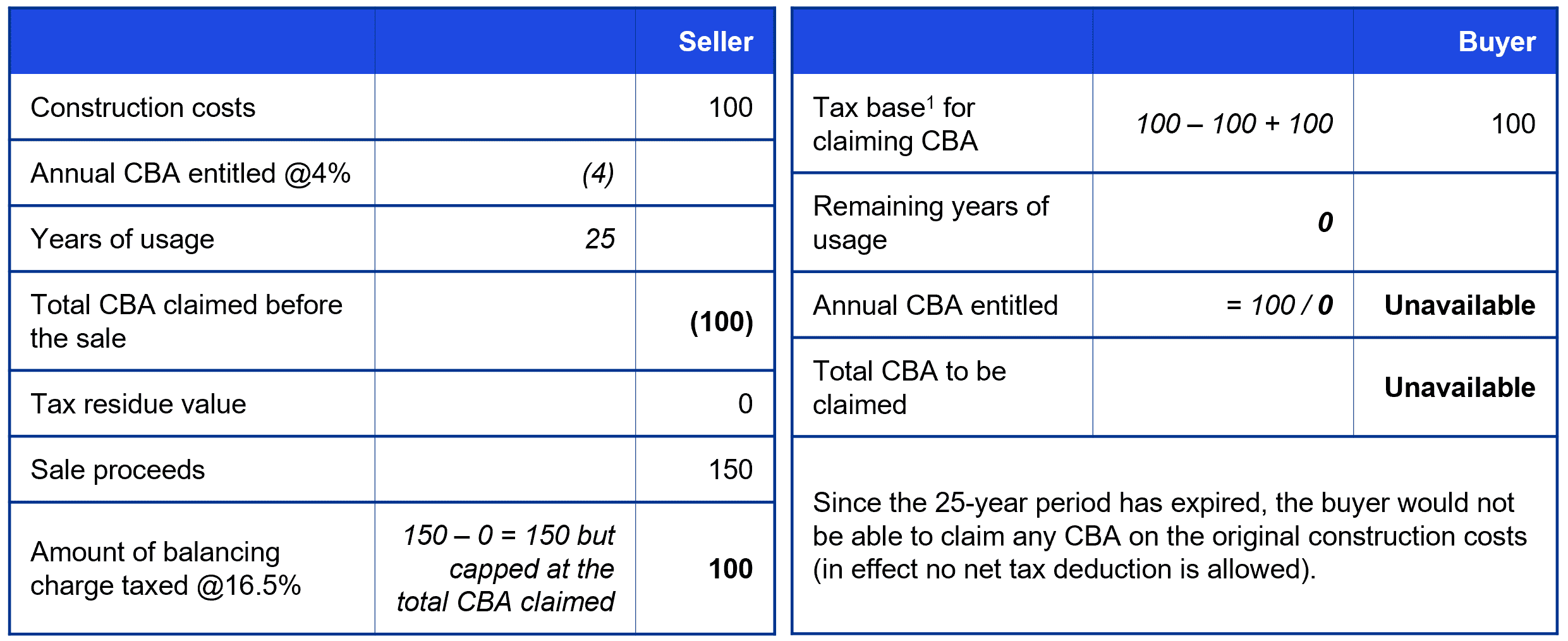

When a taxpayer subsequently sells a commercial building and the amount of consideration received by the taxpayer is greater than the tax residual value of the building immediately before the sale, the excess is taxable as a balancing charge, subject to a cap of the total CBA previously granted. The balancing charge effectively represents a claw-back of the CBA previously allowed to the taxpayer.

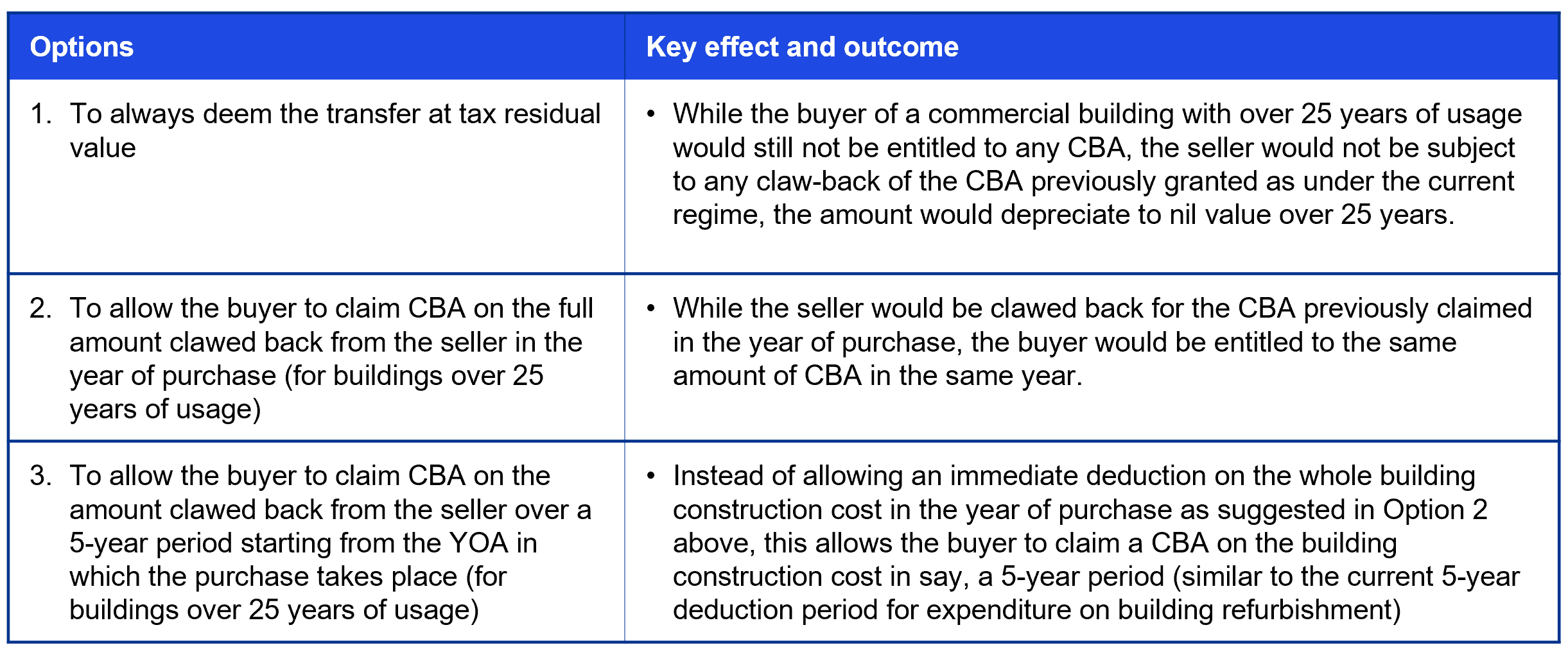

Correspondingly, the buyer can claim CBA on the tax residual value plus any balancing charge in respect of the building acquired for the remaining year(s) (if any) within the 25-year period. However, no CBA would be granted to the buyer if the commercial building has been put in use for more than 25 years – that is when the 25-year period has expired.

Property owners and investors will need to fact this issue into their investment modelling going forwards.

In our view, it is a peculiar outcome that gives rise to an issue of fairness to taxpayers. This has become an imminent issue for commercial buildings that were constructed before YOA 1998/99 as for these buildings, the counting of the 25-year period started from YOA 1998/99 and will expire by YOA 2023/24 (i.e. YOA 2023/24 will be the last YOA in which CBA on such buildings can be claimed).