The Sustainable Finance Disclosure Regulation is here The Sustainable Finance Disclosure Regulation is here

The Sustainable Finance Disclosure Regulation (SFDR) will bring a binding transparency framework for European sustainable investment products and a certain harmonization on the definition of what constitutes such products. Even if many Swiss financial institutions may not be directly in the scope of the requirements, they will feel the push towards more transparency from their clients and should learn from the struggles of their European peers.

What it’s about

The Sustainable Finance Disclosure Regulation (SFDR) is the first of many regulatory initiatives originating from the EU’s 2018 Action Plan for Financing Sustainable Growth. It aims at clarifying the duties of financial institutions regarding the integration of sustainability considerations into their investment decisions, while also promoting transparency.

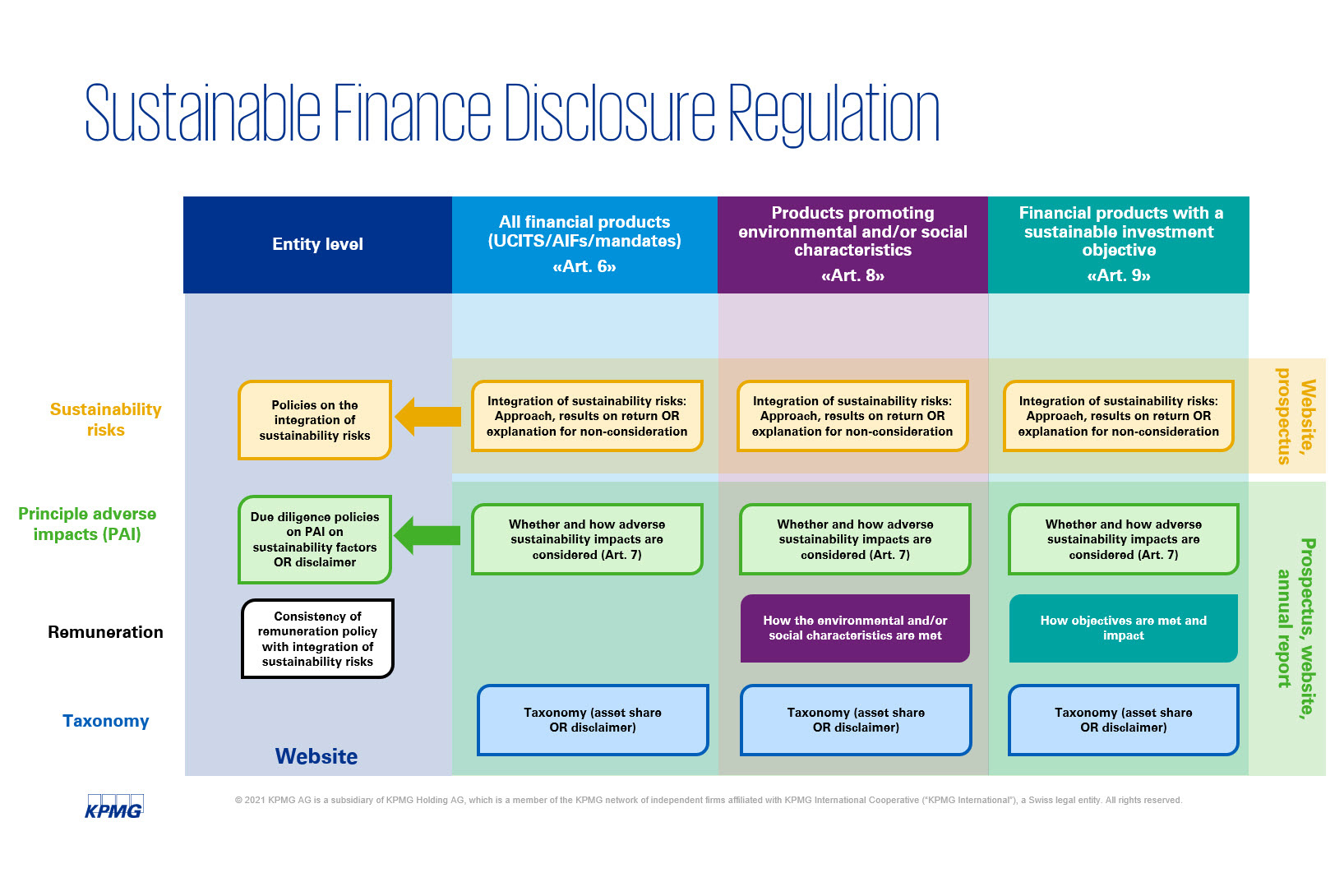

The broad range of both entity and product-level requirements coupled with very ambitious deadlines make the SFDR implementation one of the top priorities for companies concerned. What is important to note is that SFDR does not mandate specific approaches to sustainable investing. However, it does raise the bar for money managers who are looking to market their products explicitly as “sustainable” or as “impact investing” products. Our chart provides an overview of the disclosure requirements for different types of products.

How Swiss financial institutions are impacted

The SFDR applies to financial market participants and financial advisers in the EU. The former includes Alternative Investment Fund managers, UCITS Management Companies or investment firms managing portfolios on behalf of clients (MiFID II). The SFDR requirements may also be relevant to third country firms (such as Swiss Managers of EU-domiciled investment funds). As such, careful consideration of the SFDR is important not only for Swiss financial institutions with EU-subsidiaries.

The degree of legal uncertainty regarding the scope of application of the requirements to non-EU firms (namely non-EU managers of funds marketed or domiciled in the EU) remains substantial. It has even moved the European Securities Authorities (ESAs) to write a letter to the European Commission on 7 January this year seeking clarification on the scope of the disclosure requirements and some other ancillary questions. However, in practice, Swiss money managers may find that the strict legal context doesn’t matter so much.

For example, where an EU Management Company (ManCo) or Alternative Investment Fund Manager (AIFM) has delegated portfolio management to a Swiss fund manager, the disclosure obligations may formally lie with the ManCo or AIFM, but the delegated manager will likely need to contribute substantially in order to source all the data.

Finally, any Swiss fund manager or manager of segregated portfolios with EU investors is likely to receive requests to deliver the relevant data under SFDR for their portfolios, in particular where such EU investors are in scope of SFDR themselves, such as pension funds or insurance companies. The investors will require such data to prepare their own disclosures.

Why Swiss Financial Institutions should take action now

Leaving aside the strict legal or contractual context, there is a strong case for Swiss asset managers to at least take some inspiration from the SFDR requirements. While there is currently no equivalent Swiss regulation, it is becoming ever more apparent where the journey is headed – both in terms of the regulatory and societal (including investor) expectations.

First and foremost, there is growing demand for transparency on non-financial matters. The indirect counterproposal to the Responsible Business Initiative (RBI) requires firms (including all regulated financial institutions) to prepare non-financial disclosures, covering environmental concerns, in particular CO2 targets, social and labor issues, human rights and the fight against corruption. See our blog on the RBI here.

In January 2021 Switzerland became an official supporter of the Task Force on Climate-related Financial Disclosures (TCFD). The Federal Council formally recommends companies across sectors to voluntarily implement this reporting standard and is deliberating on making this recommendation binding. The recent FINMA consultation concerning the disclosure of climate-related financial risks by systemically important banks and large insurance companies is a further step on the path to increased climate-related transparency. Find out more about TCFD in our recent blog.

Another core concern of the regulator is the risk of “greenwashing”, stemming from the rising tide of products marketed as sustainable. The State Secretariat for International Finance (SIF) is expected to present a proposal to the Federal Council by fall 2021 on legislation to prevent greenwashing. At present the topic of ESG-integrated advisory services is still largely dealt with in the self-regulatory realm by players such as the Swiss Banking Association and the Asset Management Association. We have highlighted the 2021 regulatory trends in our recent blog.

For the financial services sector the SFDR constitutes a robust framework to address both transparency issues surrounding environmental and social considerations as well as greenwashing.