The operating environment for banks is rapidly changing. Regulatory frameworks are evolving. Credit, liquidity and concentration risks are rising. And increasing geopolitical tensions and tariff pressures are amplifying the potential for volatility. In this environment, is your balance sheet an asset or a liability for your organization?

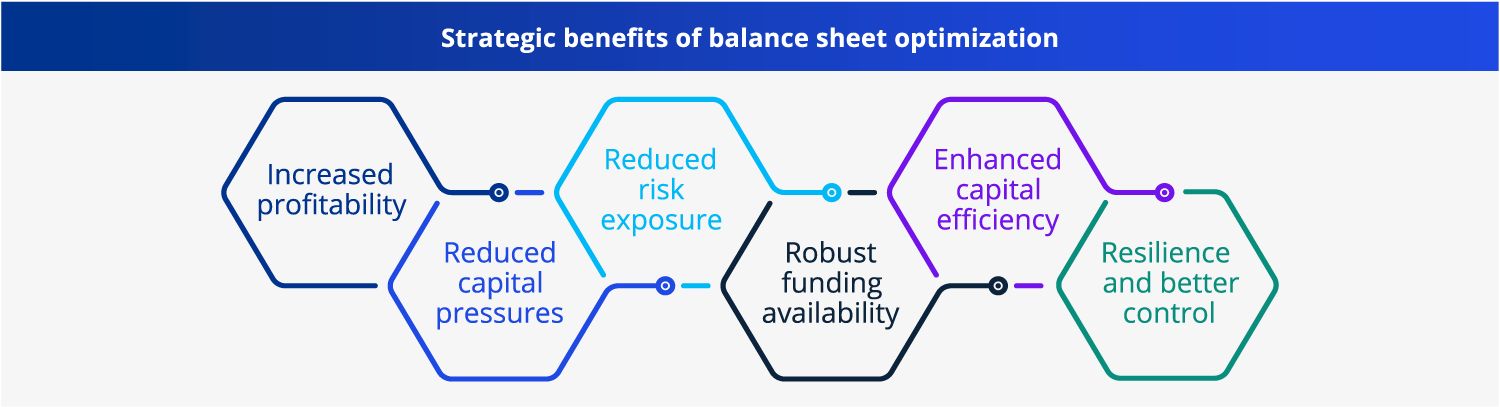

In today’s market where capital flows to efficiency and innovation, balance sheet inaction isn’t just a missed opportunity – it is a strategic liability.

"Banks should be looking at balance sheet optimization not merely as a defensive tactic, but also as a strategic imperative for enhancing bank balance sheet performance and ensuring long-term resilience."

- Navigating uncertainty: The imperative of balance sheet optimization

In an environment defined by investment needs, rapidly evolving risks, and continuous pressure on profitability due to competition and stabilization of the interest margin, banks must manage and use their available capital with precision. In Belgium - as in Europe - proactive balance sheet optimization ensures capital is allocated effectively and risks are strategically retained or transferred, helping banks to sustain their return on equity.

Key focus areas

The leading banks are focusing their attention on four key areas to drive effective balance sheet optimization.

Embedding capital-sensitive performance measures

Integrating performance metrics that are sensitive to capital intensity to optimize capital usage and improve returns.Accelerating balance sheet velocity

Accelerating the reallocation of financial resources to optimize capital deployment and improve ROTE.Centralizing control and allocation

Empowering/creating central roles for decisions on resource management to ensure efficient and agile capital deployment and redeployment.- Adopting dynamic balance sheet modeling

Considering the current balance sheet and potential shifts in the asset-liability mix driven by anticipated market changes or strategic initiatives.

“In response to growing financial and regulatory pressures, banks should focus on four critical areas for effective balance sheet optimization in order to strengthen financial positioning, improve profitability and build a more agile and adaptive institution.”

- Banks navigating uncertainty: The imperative of balance sheet optimization

Getting started

Ready to get going? Here are four key tactics many banks are now using to drive balance sheet optimization:

- Cash securitization

- Action: Transfer part of a pooled asset portfolio to an external Special Purpose Vehicle (SPV), enabling a full derecognition from the originator’s balance sheet (though the originator may continue as loan servicer).

- Benefit potential: Enables banks to address both funding and capital requirements by selling multiple tranches of notes, thereby achieving full-stack optimization.

- Synthetic securitization

- Action: Transfer of credit risk of a pool of exposures using credit derivatives (like credit default swaps) or guarantees, while the loans stay on the balance sheet.

- Benefit potential: Allows banks to release capital tied to high-risk assets, particularly through significant risk transfer (SRT), thereby enhancing redeployment flexibility.

- Mergers & acquisitions

- Action: Expansion of banks through a combination with another bank or non-bank lender.

- Benefit potential: Helps banks enter new asset niches and diversify product offerings, thus expanding the commercial offering and ROTE potential beyond existing constraints.

- Forward flow/Originate to distribute

- Action: Originate loans with the intent to sell or transfer to third parties (such as investors or securitization vehicles), rather than holding to maturity.

- Benefit potential: Increases balance sheet velocity through partnerships with counterparties (such as private credit investors, insurers and asset managers), enabling banks to scale origination without proportional capital retention.

Explore

Connect with us

- Find office locations kpmg.findOfficeLocations

- kpmg.emailUs

- Social media @ KPMG kpmg.socialMedia