The Vietnam Ministry of Finance (“MoF”) released a new Draft Corporate Income Tax Law for public consultation on 11 June 2024 (“New Draft Law”). One of the key potential changes included is a major revision to the basis of taxation for transfers of Vietnam capital in the form of shares in non-public joint stock companies or invested capital in limited liability companies, whether directly or indirectly.

Current Application vs. Proposed Change

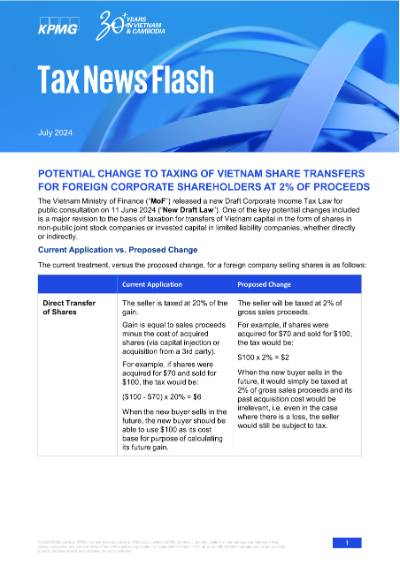

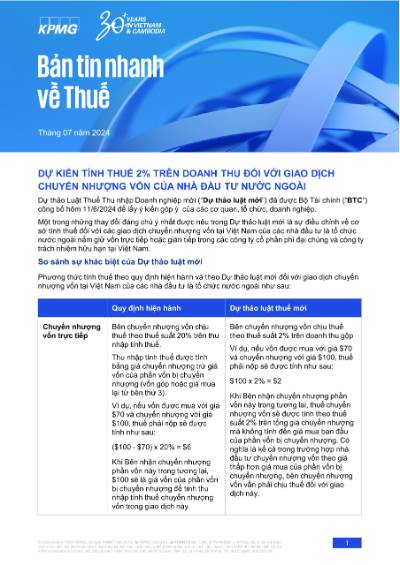

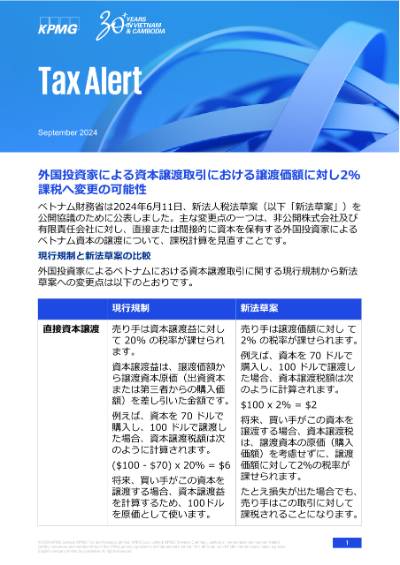

The current treatment, versus the proposed change, for a foreign company selling shares is as follows:

| Current Application | Proposed Change | |

|---|---|---|

| Direct Transfer of Shares | The seller is taxed at 20% of the gain. Gain is equal to sales proceeds minus the cost of acquired shares (via capital injection or acquisition from a 3rd party). For example, if shares were acquired for $70 and sold for $100, the tax would be: ($100 - $70) x 20% = $6 When the new buyer sells in the future, the new buyer should be able to use $100 as its cost base for purpose of calculating its future gain. |

The seller will be taxed at 2% of gross sales proceeds. For example, if shares were acquired for $70 and sold for $100, the tax would be: $100 x 2% = $2 When the new buyer sells in the future, it would simply be taxed at 2% of gross sales proceeds and its past acquisition cost would be irrelevant, i.e. even in the case where there is a loss, the seller would still be subject to tax. |

| Indirect Transfer of Shares (i.e., the shares of a foreign company are sold which has an underlying Vietnamese subsidiary or subsidiaries) |

There is currently no regulatory guidance on the method of revenue attribution or cost calculation. It is generally interpreted that the same calculation method as is used for a direct transfer of shares should be followed. From the buyer’s perspective, it is not clear whether the acquisition amount on a reported indirect transfer may be used as the cost base for its future sale if such sale occurs at a different layer in the corporate holding structure. |

The seller will be taxed at 2% of the amount of gross sales proceeds that are attributable to the underlying Vietnam subsidiary or subsidiaries. |

KPMG Comments

This is a welcome potential change in the respect of providing a clearer and simpler tax implication for foreign corporate sellers. This is particularly the case for indirect transfers, where there can be significant controversies around calculating the gain on the transfer with different corporate layers. If this new basis of taxation is passed, some of these complications will be removed. On the other hand, this potential change may result in an additional tax liability being incurred for transactions undertaken solely for restructuring purposes and/or those that are undertaken at a financial loss.

Having said the above, the New Draft Law has not yet provided a detailed definition of indirect transfer that includes reasonable limitations on its application to offshore transfers. For example, there is still no exclusion provided for sales of listed shares on foreign stock exchanges or for transfers undertaken for internal group restructuring purposes.

Finally, despite this potential change being included in the New Draft Law, it is not absolutely certain that it will pass into the final version of the law as it is still subject to comment and further rounds of consultation with the relevant authorities and business community in Vietnam.

Please contact KPMG should you require further discussion on this matter.

Download to your device here

Stay informed

Subscribe to our Tax and Legal Update newsletters for more insights and updates on the latest legislation

Subscribe here Opens in a new window