Taiwan and Singapore maintain close economic and trade relations. According to statistics from the International Trade Administration of the Ministry of Economic Affairs, Singapore was Taiwan’s eighth‑largest trading partner in ROC Year 114, with bilateral trade totaling USD 53.4 billion. As of the end of December last year, cumulative Taiwanese investment in Singapore amounted to approximately USD 32.5 billion, while Singaporean investment in Taiwan reached approximately USD 12.7 billion.

However, the original Taiwan–Singapore Tax Agreement (“the Original Tax Agreement”), which entered into force in 1982, was Taiwan’s first comprehensive income tax agreement and has been in place for over four decades. In light of the significant development of bilateral economic and trade relations, the revised agreement has been announced to come into effect (“the Renewed Tax Agreement”), which is substantially updated by reference to the OECD and UN Model Tax Conventions, with a view to providing tax relief measures that better reflect current commercial realities in both jurisdictions and to creating a more favorable tax environment for bilateral trade and investment.

Key revisions under the Renewed Agreement include a comprehensive reduction in maximum withholding tax rates, the removal of exclusions denying tax exemption for management service fees, clarification of the definition of service permanent establishments (“PE”), and the granting of taxing rights to the source jurisdiction over capital gains derived from the transfer of immovable property, assets attributable to a PE, and certain unlisted shareholdings. In addition, several preferential provisions have been introduced, such as rules under which qualifying Collective Investment Vehicle (“CIV”) deriving income from the other jurisdiction may be treated as a resident and beneficial owner of one jurisdiction and thereby eligible for treaty benefits. Overall, these amendments are expected to effectively reduce the tax costs of cross‑border investments between Taiwan and Singapore and further strengthen the foundation for bilateral economic cooperation.

Reduction of Maximum Withholding Tax Rates on Passive Income

The Renewed Tax Agreement introduces substantial improvements to withholding tax on dividends, interest, and royalties. While the Original Tax Agreement contained nominal rate caps, the actual benefits were limited. For example, Taiwan’s statutory withholding tax rate on dividends is 21%, yet the Original Tax Agreement did not provide a reduced rate for dividends paid to Singapore residents. Likewise, the 15% withholding tax cap on royalties under the Original Tax Agreement was less favorable than the 10% cap commonly found in other Taiwan comprehensive tax agreements.

This demonstrate that the level of tax relief offered under the Original Tax Agreement was less competitive than those available under Taiwan’s other comprehensive tax agreements. Under the Renewed Tax Agreement, the maximum withholding tax rates for dividends and royalties have been reduced to 10%, and a new 10% rate for interest has been introduced, bringing the Taiwan–Singapore Tax Agreement in line with other modern Taiwan tax agreements. These changes are expected to materially reduce the tax burden on cross‑border transactions and further enhance economic and investment exchanges between Taiwan and Singapore.

Management Support Service Fees May Now Qualify for Business Profits Exemption

Multinational enterprises often centralize management functions in regional headquarters to improve operational efficiency across the group. Singapore has long been one of the preferred locations for Asia‑Pacific headquarters which frequently provides management support services to Taiwan affiliates, thereby charging cross‑border service fees for such activities. However, under the Original Tax Agreement, the definition of “Business Profits” expressly excluded income derived from “the management, control or supervision of the trade, business or other activity”. As a result, management service fees paid by Taiwan entities to Singapore group companies generally could not qualify for exemption under the business profits article of the Original Tax Agreement.

The Renewed Tax Agreement removes this exclusion and aligns with other Taiwan comprehensive income tax agreements. This change is expected to substantially reduce the tax exposure associated with cross‑border management services and provide multinational groups with greater flexibility in determining service‑provider location.

Qualifying Collective Investment Vehicles Are Eligible for Tax Agreement Benefits

Another important improvement is the explicit inclusion of qualifying CIVs within the scope of entities eligible for benefits under the Renewed Tax Agreement. A CIV that meets the criteria defined in the Renewed Agreement will be treated as a resident and the beneficial owner of income sourced from the other jurisdiction. This allows CIVs to enjoy preferential withholding tax rates for dividends, interest, and similar income.

Under the Renewed Agreement, a qualifying CIV in Taiwan refers to publicly offered mutual trust funds, securities investment trust funds, futures trust funds, real estate investment trusts, and any other investment fund, arrangement, or entity that the authorities of Taiwan and Singapore jointly agree to recognize as a CIV.

The introduction of this rule helps resolve long‑standing issues frequently encountered by cross‑border investment funds, trusts, and other pooled investment vehicles regarding the determination of “resident” and “beneficial owner” status for treaty purposes. It ensures that qualifying CIVs may continue to assert their eligibility for treaty benefits. This revision is expected to significantly enhance tax efficiency in capital market transactions between Taiwan and Singapore.

Clarification of Service Permanent Establishment and Extension of the Construction PE Threshold

Under the framework of a tax treaty, where a foreign enterprise derives business profits through PE in Taiwan, such profits cannot enjoy the business profits exemption. In addition, most comprehensive tax agreements define PE not only by reference to a physical place of business, but also through a service permanent establishment, which is deemed to exist when a foreign enterprise furnishes services in the other territory through its employees for a specified duration. For example, under the Taiwan–Korea Tax Agreement, a service PE is constituted where: “the furnishing of services, including consultancy services, by an enterprise through employees or other personnel or persons engaged by the enterprise for such purpose, but only if activities of that nature continue (for the same or a connected project) within a territory for a period or periods aggregating more than 183 days in any twelve-month period”

However, the Original Tax Agreement did not include a definition for a service PE, which had resulted in practical uncertainties. The Renewed Tax Agreement introduces an explicit service PE provision aligned with the approach adopted in most of Taiwan’s comprehensive tax agreements. Consequently, when Singapore enterprises dispatch personnel to Taiwan to provide services, the applicable thresholds and conditions are now clearly defined. This enables enterprises to effectively utilize the business profits exemption and appropriately reduce the tax burden associated with cross‑border services.

Furthermore, under the Original Tax Agreement, a construction PE would arise where supervisory or consultancy activities relating to building, installation, or assembly projects exceeded six months. Under the Renewed Tax Agreement, this threshold has been extended to more than nine months. This change enhances flexibility for deploying cross‑border project personnel and is expected to improve the overall efficiency of project execution.

Other Key Amendments

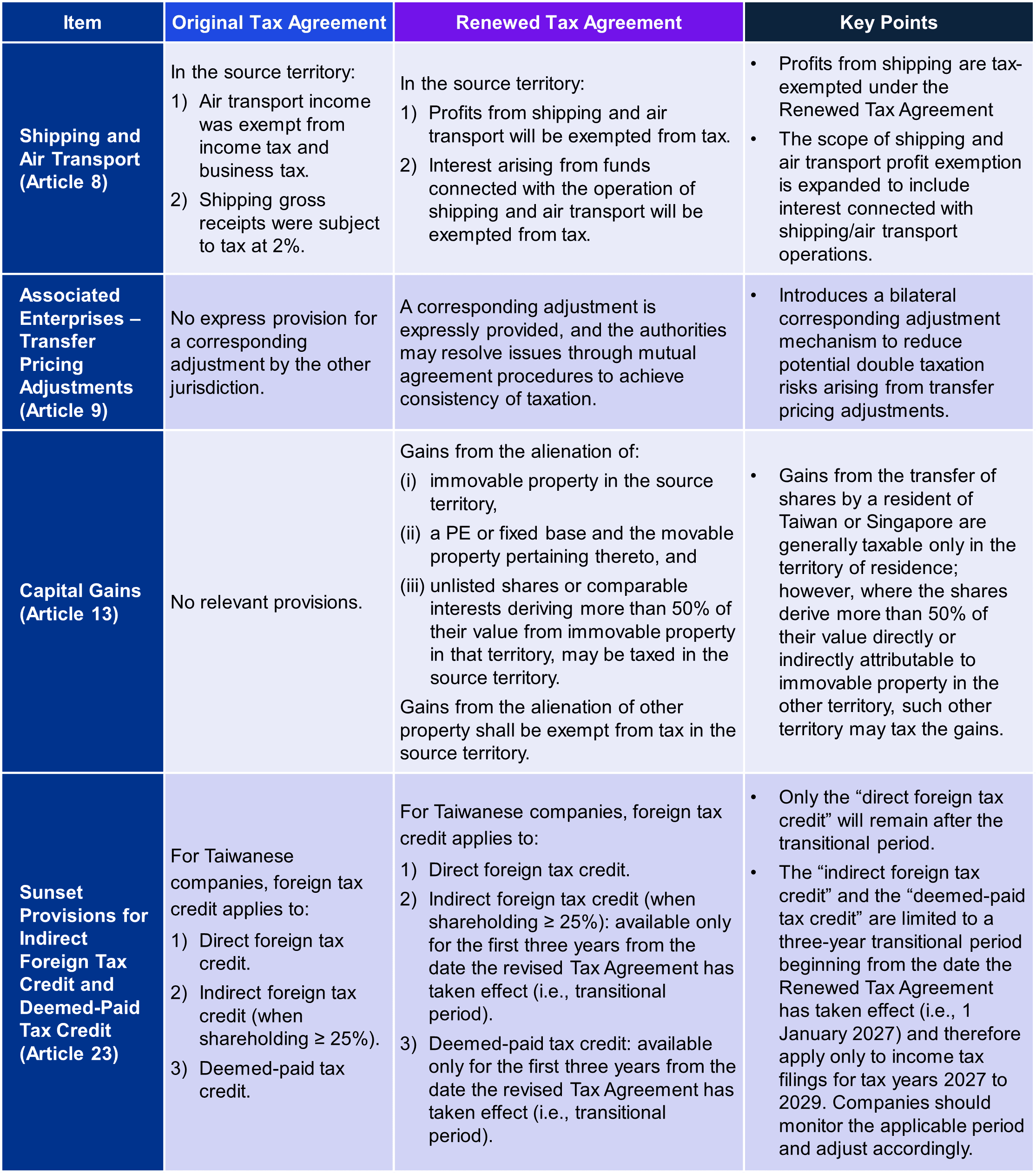

In addition to the major revisions described above, the Renewed Tax Agreement also introduces a number of provisions that are broadly consistent with those found in Taiwan’s other comprehensive income tax agreements. These amendments strengthen the consistency of the Renewed Tax Agreement and bring its contents more closely into line with prevailing international standards on tax agreements. The updates cover

(i) the taxation of shipping and air transport profits derived from source territory,

(ii) clarification of the transfer pricing adjustment mechanism for associated enterprises,

(iii) taxation of gains from the transfer of unlisted shares or comparable interests where more than 50% of their value is attributable to immovable property in the source territory, and

(iv) sunset provisions applicable to the indirect foreign tax credit and the deemed‑paid tax credit.

For ease of reference, the key amendments and their practical implications are summarized below.