Despite new challenges, CEOs confident in growth through transformation

Key insights from the KPMG 2016 CEO Outlook

KPMG’s 2016 Global CEO Outlook reveals that CEOs are increasingly confident in achieving growth in the next 3 years. Despite having realistic concerns with their current readiness to face emerging challenges, CEOs are confident they can transform their companies for the future.

Highlights

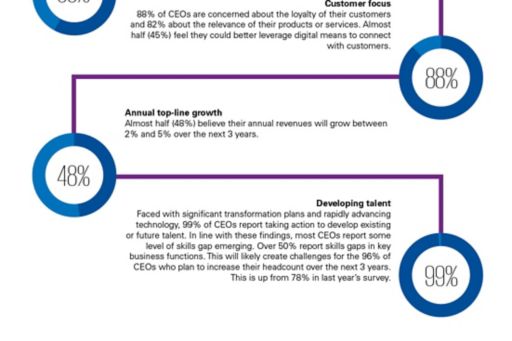

The force and speed with which technological innovation is moving through the economy is creating an inflection point for the business sector, say the vast majority of CEOs surveyed. So great will be the impact, that 41 percent of CEOs expect to be running significantly transformed companies in 3 years’ time. That response rate is up from 29 percent who felt that way a year ago. In addition, 82 percent of those surveyed are concerned whether their company’s current products or services will even be relevant to customers 3 years from now.

A significant majority of CEOs recognize the important need to foster a culture of innovation, respond quickly to technological opportunities and invest in new processes. But most CEOs recognize that they are now handling issues that they have never grappled with before.

Global CEOs of the largest corporations have indicated they are prepared to handle this period of unprecedented change with realistic expectations and a healthy dose of confidence. They are increasingly optimistic that they can transform their organization to enable it to capture the opportunity that the future holds. This confidence is apparent in their hiring plans and projected top-line growth over the next 3 years.

Highlights of KPMG’s 2016 Global CEO Outlook

KPMG’s 2016 Global CEO Outlook study provides a vivid image of global CEOs’ expectations for business growth, the challenges they face and their strategies to chart organizational success over the next 3 years. Key findings include:

About the survey

The survey targeted 1,268 CEOs in 10 key markets (Australia, China, France, Germany, India, Italy, Japan, Spain, UK and US) and 11 key industry sectors (automotive, banking, infrastructure, insurance, investment management, life sciences, manufacturing, technology, telecommunications, retail/consumer markets and energy/utilities). A third of the respondents have more than US$10 billion in annual revenue, with no responses from companies with annual revenues lower than US$500 million.

© 2024 KPMG Bağımsız Denetim ve Serbest Muhasebeci Mali Müşavirlik A.Ş., şirket üyelerinin sorumluluğu sundukları garantiyle sınırlı özel bir İngiliz şirketi olan KPMG International Limited ile ilişkili bağımsız şirketlerden oluşan KPMG küresel organizasyonuna üye bir Türk şirketidir. Tüm hakları saklıdır.

Küresel KPMG ağının yapısı hakkında detaylı bilgi için kpmg.com/governance adresini ziyaret edebilirsiniz.