The publication of the first two IFRS® Sustainability Disclosure Standards1 is a key milestone in the International Sustainability Standards Board (ISSB)’s vision – to create a global baseline for investor-focused sustainability reporting that local jurisdictions can build on.

Better information can lead to better economic decisions. These standards are designed to meet the needs of all companies. They provide a clear idea of what companies need to report on to meet the needs of global capital markets, providing investors with globally comparable information.

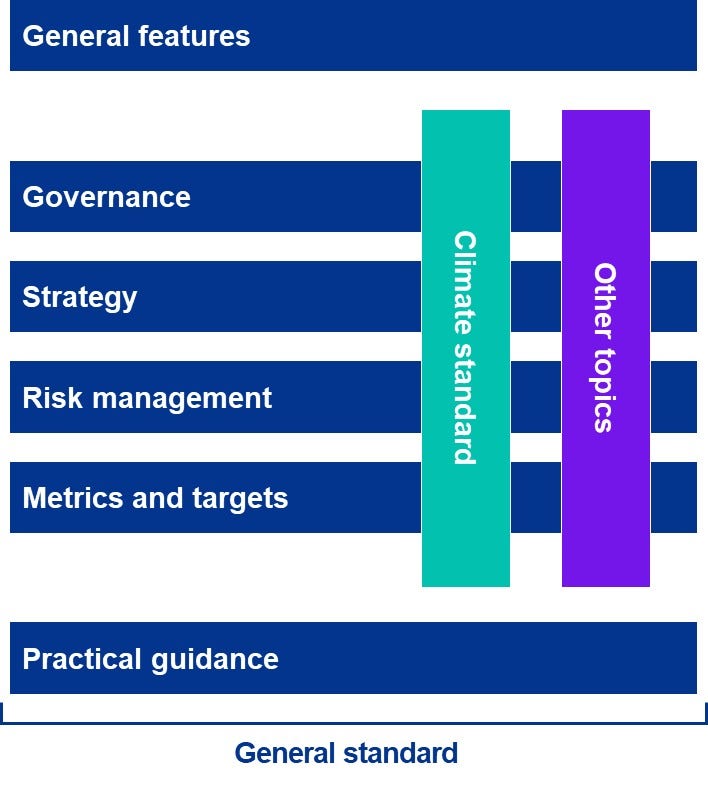

Adopting these standards will signify an important change in status, as they will increase the prominence and connectivity of sustainability reporting within the main financial filings. It is important to engage now to understand what this new global baseline will look like and to assess how your company needs to adapt.