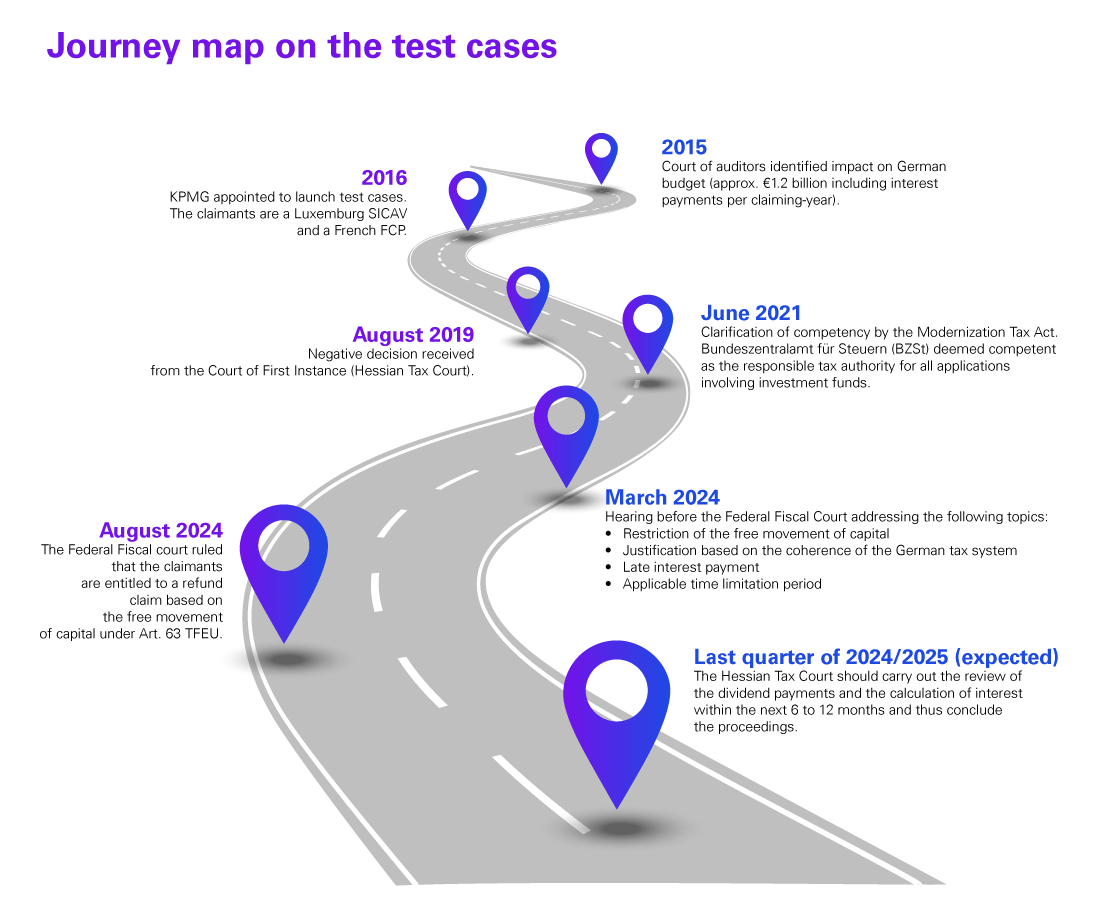

On 21 August 2024 the German Federal Fiscal Court (BFH) issued its judgement on the KPMG test cases (IR 01/20, IR 02/20) on the refund of dividend withholding tax to foreign investment funds for refund years prior to 2018. The claimants, which were represented by KPMG, obtained the following positive decisions:

I. Dividend Withholding Tax is to be refunded based on the free movement of capital under Art. 63 TFEU

BFH ruled that the claimants (investment funds: a Luxembourg SICAV and a French FCP) are entitled to a refund claim based on the free movement of capital under Art. 63 TFEU.

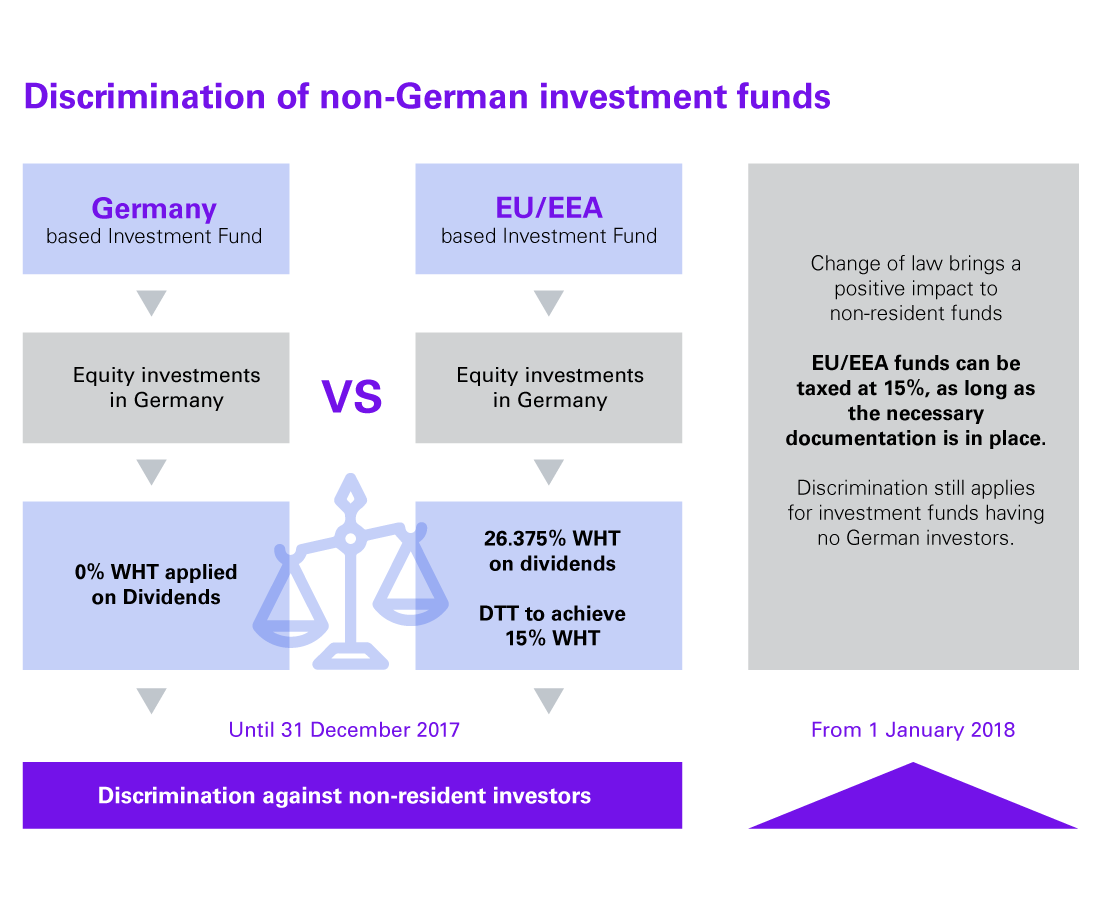

BFH considered that the German legislation was discriminatory as Section 11 of the German Investment Tax Act (InvStG) exempts German funds from tax on German dividend income for the dividend years 2004 to 2017, while foreign funds had to pay a withholding of at least 15% on German source dividends. In addition, BFH rejected the justification of the coherence of tax law, which was still affirmed by the lower tax court (Hessian Tax Court), and which intended to take investor (fund unit holder) taxation into account, since Section 11 InvStG does not make the tax exemption of German funds dependent on the subsequent taxation of investors.

II. Limitation period is four years

The BFH concluded that the general German limitation period of four years after the end of the year in which the dividend was received, or the dividend withholding tax was paid, applies.

III. Late interest of 0.5% per month is generally payable on the refund amount

BFH also awarded late interest to the foreign investment funds. German legislation provides that the refund amounts for the entire period in which the dividend withholding tax was not available to the claimant are subject to late interest of 0.5% per month from the interest claim under EU law in accordance with the national German regulations.

For refund years prior to 2012, the late interest period is to begin six months after the date on which the refund application was submitted to the competent tax office, and for refund years from 2012 onwards with the levy of dividend withholding tax when the dividend was received. The BFH did not need to decide in the present cases whether the interest rate should also be set at 0.5% per month (or 0.015% due to statutory adjustments) for periods from 2019 onwards. KPMG considers that there are good arguments for the interest rate to also be 0.5% per month from 2019 onwards.

IV. Further procedure

The judgement of the lower court (Hessian Tax Court) was overturned, and the proceedings were referred back to the Hessian Tax Court of first instance so that the tax court can:

- Finally clarify whether the claimant was effectively subject to withholding tax (e.g., sufficient proof of withholding tax and dividend vouchers, beneficial ownership of the funds on dividend ex-date), and

- Carry out the complicated calculation of the refund interest based on the BFH decisions.

The Hessian Tax Court should carry out the review of the dividend payments and the calculation of interest within the next 6 to 12 months and thus conclude the proceedings.

It is likely that the Federal Tax Office (BZSt) will only process the applications for refunds on a large scale once the two proceedings have been concluded by the Hessian Tax Court and will request the relevant evidence for this purpose. Only then will the conditions for a refund (verification of dividends) be fully clarified. Regarding the actual implementation of the next steps, we are actively consulting with the German tax authorities, among others.

V. Recommendations

Further to the BFH’s judgement, we recommend the following:

- Correspondence: Keep track of any correspondence received from the German Tax authorities. As the BZSt is already processing individual refund applications from investment funds for refund years prior to 2018, it is important for applicants to pay attention to any correspondence they receive from the German tax authorities. To prevent legal setbacks, the general deadline of one month must be strictly observed. In case of doubt, it should be assumed that the deadline of one month starts as of the date stated in the letter from the German tax authorities.

- Time limitation period: Verify whether the claims have been filed with the competent authority within the four years’ time limitation period.

- Claim documentation: To obtain a refund, evidence will be key. It is important that the claim documentation contains inter alia proof that the fund was effectively subject to German withholding tax, is the beneficial owner of the dividends and has not performed any securities lending or other similar transactions.

- Late interest payment: Ensure that late interest payment is requested in the claim.

We would be pleased to further discuss the impact of this judgement and the recommended steps. Please feel free to contact us.