The European Commission has unveiled its proposal for the first omnibus package aimed at simplifying the Corporate Sustainability Reporting Directive (CSRD), the Corporate Sustainability Due Diligence Directive (CSDDD), and the EU Taxonomy. This proposal introduces several key changes to the CSRD that could significantly impact sustainability reporting across the EU.

Key changes to the CSRD

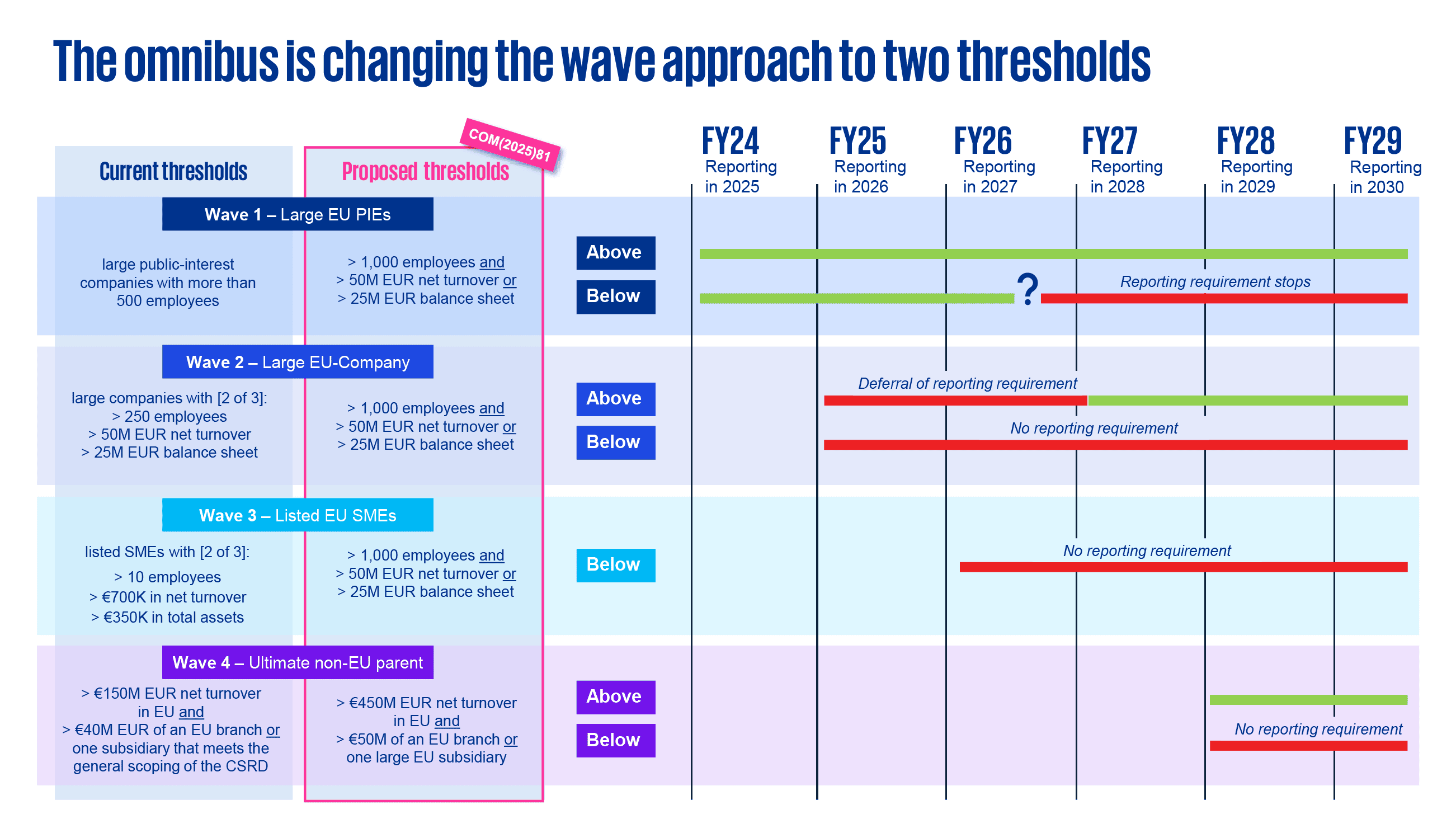

- Reporting requirements: The new proposal specifies that the reporting requirements will apply only to large undertakings with more than 1,000 employees (i.e undertakings that have more than 1,000 employees and either a turnover above EUR 50 million or a balance sheet above EUR 25 million).

- Voluntary reporting standard for smaller companies: For companies that will no longer be within the scope of the CSRD (those with up to 1,000 employees), the Commission plans to adopt a voluntary reporting standard by delegated act. This standard would be based on the Voluntary Standard for SMEs (VSME) developed by EFRAG.

- Simplified reporting: The Commission would revise the delegated act establishing the European Sustainability Reporting Standards (ESRS) to substantially reduce the number of data points, clarify ambiguous provisions, improve consistency with other legislation, and streamline reporting requirements.

- No sector-specific standards: The proposal will remove the empowerment for the Commission to adopt sector-specific standards, simplifying the regulatory framework.

- Assurance requirement changes: The proposal eliminates the possibility for the Commission to propose a shift from a limited assurance requirement to a reasonable assurance requirement, maintaining the current standards.

- Postponement of reporting requirements: The package proposes a two-year delay in the implementation of reporting requirements for large companies yet to start implementing the CSRD and for listed SMEs (Waves 2 and 3). This extension aims to provide co-legislators with time to agree on the proposed substantive changes.

- Limiting EU taxonomy reporting obligations: The proposal also seeks to limit the EU Taxonomy reporting obligations to the largest companies that fall within the scope of the CSDDD.

Looking ahead

The proposals presented by the European Commission mark the beginning of an important legislative process at the EU level. It is crucial to closely monitor the further development of this process, as the contents are far from finalized. The coming months will reveal how these regulations will evolve and what impact they will have on sustainability reporting and corporate due diligence obligations.

For more information, you can read the full press release on the proposal of the first omnibus package here.

How can KPMG support you?

Beyond the regulatory obligations, climate resilience and ESG impact mitigation remain key to preserving and creating value in sustainable businesses. KPMG can support you in achieving your long-term sustainability ambition. Reach out to our experts to learn more.