European Debt Sales - Slovenia

European Debt Sales - Slovenia

An in-depth look into how the loan sale market performed in 2015 in Slovenia.

“The quality of the loan books within the Slovenian banking sector is gradually improving, though NPLs remain a concern.“ – Bostjan Malus, Partner, Head of Deal Advisory, KPMG in Slovenia

The Slovenian loan sale market is still in its infancy, with only a few transactions successfully executed in the market to date. However, investor interest in Slovenia is growing, with two transactions brought to market in Q4 2015.

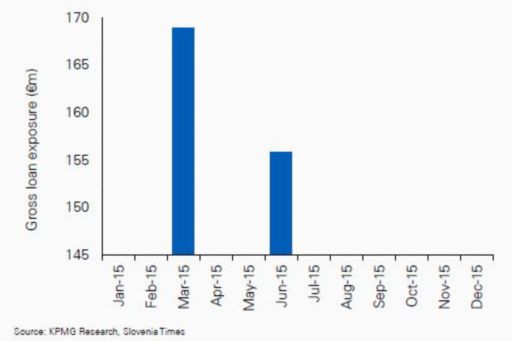

BAMC (DUTB)1, the Slovenian bad bank formed in 2014, signed its first transaction since its inception with the sale of a portfolio of claims of four companies to Bank of America Merrill Lynch. It is expected that BAMC will be bringing further portfolios to market in the coming year due to the success and interest the first sale attracted.

Other developments

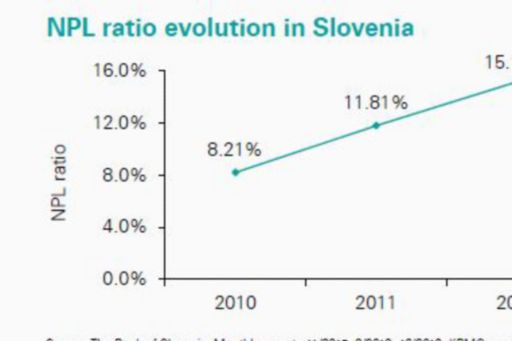

In 2013, the unemployment rate increased to 8.9 percent, leading to a growth in consumer NPLs, particularly in state-owned banks. In 2015, the unemployment rate stood at 9.3 percent, and the overall NPL ratio stood at 11.5 percent. In December 2013, BAMC (DUTB)1 was formed to transfer the NPLs of the state-owned banks (which amounted to €5 billion in 2014) to the “bad bank” in order to find a more efficient solution to deleveraging. A large portion of these banks’ non-performing assets were transferred into BAMC, allowing the banks to be recapitalised with sufficient capital to continue performing and supporting lending to the Slovenian economy.

Looking forward & KPMG predictions

Further loan sales are expected to be in the pipeline for 2016. BAMC will be selling approximately 10 percent of their assets in 2016, as mandated by the “Act regulating measures of the Republic of Slovenia for strengthening banks’ stability”, where it stipulates that BAMC should annually enforce 10 percent of their weighted average transferred assets.

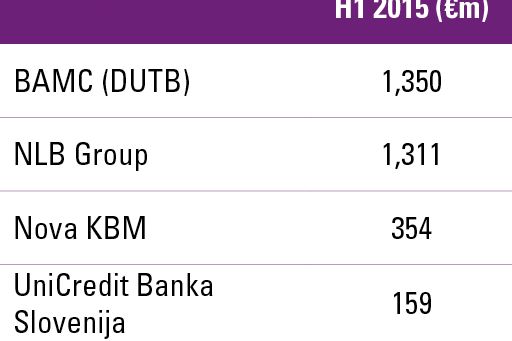

Investor interest and liquidity for NPLs in 2016 will be heavily dependent on the success of the sale of the portfolios brought to market in 2015 by NLB (Project Pine) and Nova KBM. While the portfolio sales have attracted interest from a range of international investors, some investors have expressed concern about the pricing expectations of these sellers.

© 2025 Copyright owned by one or more of the KPMG International entities. KPMG International entities provide no services to clients. All rights reserved.

KPMG refers to the global organization or to one or more of the member firms of KPMG International Limited (“KPMG International”), each of which is a separate legal entity. KPMG International Limited is a private English company limited by guarantee and does not provide services to clients. For more detail about our structure please visit https://kpmg.com/governance.

Member firms of the KPMG network of independent firms are affiliated with KPMG International. KPMG International provides no client services. No member firm has any authority to obligate or bind KPMG International or any other member firm vis-à-vis third parties, nor does KPMG International have any such authority to obligate or bind any member firm.