The semiconductor opportunity for Ireland

As the global semiconductor industry booms, Ireland has significant opportunities to play a part on the world stage. Our Strategy team take a look at Ireland's potential as a semiconductor hub.

As the global semiconductor industry booms, Ireland has significant opportunities to play a part on the world stage. Our Strategy team take a look at Ireland's potential as a semiconductor hub.

Ireland already occupies a sizeable portion of advanced semiconductor manufacturing and research and development in a European context, however maintaining and growing this presence is fast becoming a national and European priority. To support and grow Ireland’s Silicon Isle reputation will require a collaborative focus from both industry and regional leaders.

Global semiconductor demand is surging as consumers and businesses adopt the latest offerings in generative artificial intelligence (Gen AI), cloud computing, data centres, electric vehicles, and aerospace. At the same time, semiconductor producers and governments are scrambling to diversify and protect supply chains from a historic low point of semiconductor manufacturing in Europe and the United States.

KPMG research shows increasing geographical diversity is the number one supply chain priority companies plan to achieve over the next three years, and 2023 saw the EU announce its commitment, via the EU CHIPS act, to produce 20% of global semiconductors by 2030. These ambitions are likely to drive compound European annual growth more than 6% in the coming two decades, tripling the European semiconductor market from today’s ~€55bn by 2040.

This sense of urgency is being felt by the Irish semiconductor sector through strategic investments in new wafer fabrication facilities, targeted FDI (Foreign Direct Investment) and the ongoing creation of a National Semiconductor Strategy for Ireland.

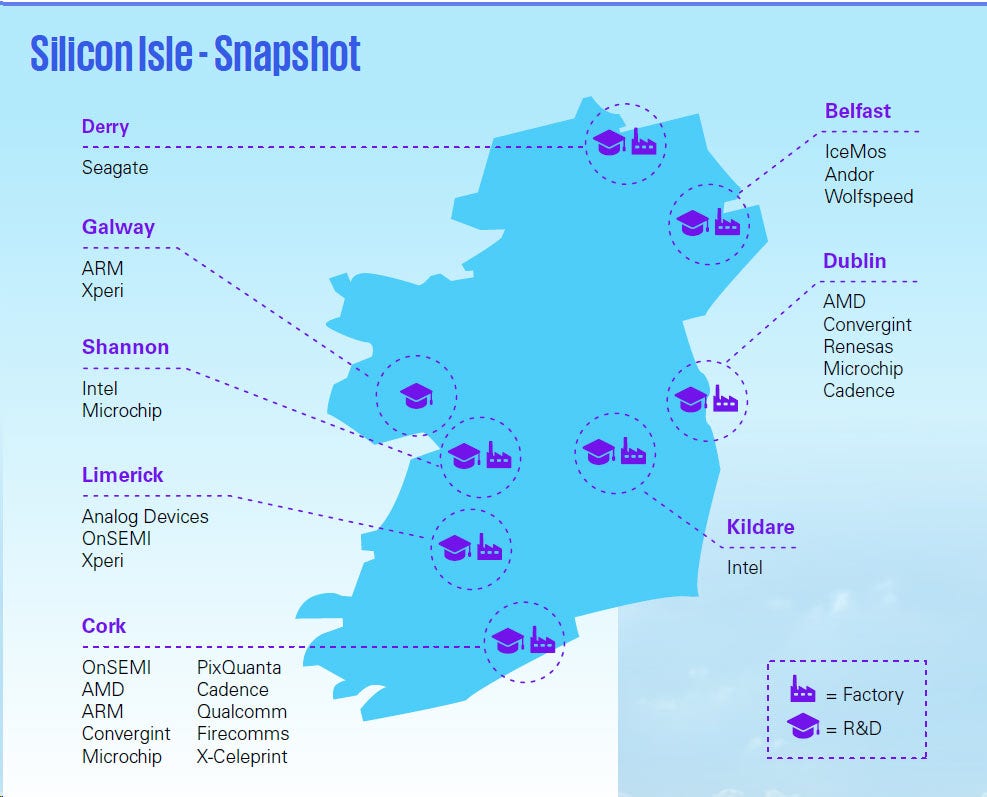

Exactly where this strategy will focus is yet to be determined, but key island wide strengths in leading edge chip manufacturing as well as specific developing expertise in photonics and semiconductor design is likely to play a role.

Ireland, with its existing production base and developed electronics sector, has a huge opportunity to capitalise on Europe’s chip production ambitions. Ireland’s semiconductor industry – with €15.5bn revenue in 2023 – is well-established, employing some 20,000 people.1

This gives Ireland a platform from which to build opportunities across the semiconductor value chain, including in a wide range of ancillary industries such as MedTech, industry 4.0, and ICT (Information and Communications Technology). With the right strategy the Irish market can support up to 34,500 new roles by 2040 promising a cascade of wider economic benefits.2

Ireland’s ability to retain a key presence in the semiconductor sector is not guaranteed. Many stakeholders in industry and academia have commented that without a cohesive strategy to protect existing industry and nurture innovative technology, Ireland may fall behind other European nations.3

To maximise Ireland’s role in the European semiconductor boom will require a proactive, government-led strategy to encourage foreign and domestic investment, nurture innovation and address growth bottlenecks along with sectoral weaknesses. This is likely to necessitate a range of incentives, especially aimed at fulfilling a meaningful skills strategy as well as continuing leadership in niche R&D.

From an investor perspective, Ireland has a clear value proposition as a destination for capital. As a pivotal player in the European growth of semiconductor manufacturing and R&D in recent decades, Ireland is a credible player in R&D, foundry operations and can expand offerings in outsourced assembly and test services (OSAT) and advanced packaging.

Ireland has a proven track record of attracting foreign direct investment (FDI) and supporting indigenous technology research and development, including foreign acquisitions. Its workforce quality in both design and manufacturing functions is competitive with the US, Asia and the rest of Europe, and its openness to global trade and stability have made it attractive to many global operators seeking low-trade restrictions and access to Europe.

There is a significant interest in emerging technologies across Europe. Tyndall National Institute (Tyndall) in particular has a strong interest in the transition to the chiplet model, which could open an opportunity for Ireland to become one of the global locations of choice to develop and fabricate low to medium volume, high value, semiconductor-based SiP products.

“Such products do not easily fit into the existing supply chain as it is currently built for single large volume chips, and based primarily on silicon. As a result, there is a challenge to accommodate next generation products that require the integration of chiplets fabricated from different materials and where the product volumes can be modest when compared to those for which the current supply chain is designed around” notes Patrick Morrisey of Tyndall.

This may be an unexploited opportunity Ireland has yet to capture, where Ireland could leverage existing significant semiconductor sector, leading edge expertise and technology in areas such as heterogenous integration and advanced packaging, to establish one of the world’s leading locations to develop and manufacture high value SiP products for sectors such as MedTech, space and energy.

At the same time, Ireland faces challenges related to the availability of talent and the affordability of manufacturing. These constraints are a common theme across many global locations for semiconductor R&D and manufacturing, requiring specific government and industry collaboration to address.An area where there is particularly strong potential at a European level is backend processing, in particularly advanced packaging, assembly and test.

These steps in the semiconductor production process are less developed in Europe compared to Asian hubs, owing mainly to higher labour costs across Europe. This labour cost gap is being narrowed with targeted government supports across Europe and US. Other factors such as electricity, water and land availability are often cited by multinational companies as limiting growth potential.

MNCs are now working with governments to invest in enhanced process efficiencies, with a particular focus on water recovery and utlising greener energy sources. Ireland is proactive in this space with existing industry support for renewables and water restoration.

The semiconductor value chain is highly dispersed, and a strategic approach to the future of the sector should take account of where Ireland’s advantages truly lie.

Talent is universally recognised by industry stakeholders as the leading constraint they face, with 52% of European semiconductor companies stating this is the biggest risk they face.4

Solving the talent gap requires a multi-pronged response to address both immediate and longer-term needs, including (in the short term) cross training between industries, short courses, and expanded opportunities for researchers, PhDs, and post doctorates, as well as an adequately funded educational framework for second level, vocational training, and university education for the longer term.

At a European level the EU Chips Act hopes to address this gap by upskilling half a million workers to enable the EU’s 2030 doubling of manufacturing goal4. In an Ireland context university collaboration with industry, such as Microelectronic Circuits Centre Ireland (MCCI) and the Tyndall, have a critical part to play in engaging in early-stage research, as well as transitioning PhDs and researchers into their sector to grow the talent pool of microelectronic engineers.

Investment in Leaving Certificate and Post Leaving Certificate (PLC) course education will also be critical to ensure a complete talent pipeline across semiconductor manufacturing and research and development.

Energy and infrastructure are a concern on a global level, with many countries focusing on industry collaboration to collectively solve constraints. Many manufacturers of semiconductors are striving for elevated levels of water efficiency – which itself has resulted in significant R&D in the water treatment and processing sector. Equally semiconductor manufacturers are actively seeking locations which offer renewable energy and the ability to work alongside communities and other industries, rather than potentially competing for finite resources.5

Incentives may be necessary to unlock priority FDI, e.g., capital expenditure (capex) refund incentives are proving attractive at a global level. However, there is caution over balancing incentives (often running to billions of euros or dollars) with wider economic benefits. Such incentives may have a place in making the market more investable, not only for the major OEMs (Original Equipment Manufacturer) but for venture capital, private equity, and other investors, all of whom are taking a greater interest in the sector.

Investment firms including Brookfield, Apollo, and asset manager Ardian’s Europe-focused semiconductor fund, have all been active in co-investing in semiconductor R&D and manufacturing facilities in recent years.6 7 8

Capturing the growth opportunity in semiconductors is worth much more to Ireland than the value of the semiconductor market alone. Semiconductors are a key enabler for growth and innovation in a wide range of other industries, many of which Ireland already has strong domestic clusters of key industries including ICT, MedTech, Industry 4.0, sustainable and green technologies and aerospace.

There are clear synergies to exploit between Ireland’s semiconductor industry and these clusters, which can benefit hugely from an expanded domestic semiconductor base, and vice versa.

With such a wide range of benefits on offer across the economy, there is a clear need to understand how these clusters are evolving, to matchmake their R&D requirements with those of the semiconductor industry, co-develop infrastructure and talent pipelines, and forge partnerships to align with existing sector strategies and regulation.

Ireland’s ICT sector, with over 106,000 employees, thrives on its symbiotic ties with the semiconductor industry. Nurturing this relationship is crucial for sustaining heightened FDI and global competitiveness. Key areas of overlap encompass AI (Artificial Intelligence), advanced connectivity (e.g., 5G/6G), IoT (Internet of Things), and quantum computing.

Ireland’s MedTech sector, valued at €13bn and constituting 8% of total annual exports, is closely intertwined with the semiconductor industry. Supporting cross-sector investment is vital. Key areas of overlap include wearable sensors, as well as implantable, diagnostic, and imaging devices.

Semiconductors are driving Ireland’s transition into the Fourth Industrial Revolution, reshaping its economy from advanced manufacturing to frontier technologies. Key areas of overlap encompass cloud computing, blockchain, analytics, machine learning, AI, VR/AR testing, robotics, and additive manufacturing.

Ireland leads Europe’s renewable revolution, targeting 80% of electricity from renewables by 2030, with semiconductors set to play a pivotal role. Irish and MNCs semiconductors in Ireland are enabling a new wave of precision agriculture through advanced image and data processing, more global efficient communications through photonics and facilitating enhanced maintenance scheduling of grid generation and network assets.

Source: - Analog Devices, 2024 - Origin Enterprises, Origin Digital

Semiconductor demand is predicted to grow steadily for the foreseeable future, and Ireland is well positioned to capitalise on this significant growth opportunity. Strategic initiatives such as incentivising R&D partnerships, cross-training programs, infrastructural investment, and targeted incentives can further bolster Ireland’s position to not only meet but exceed its share of European and global semiconductor growth in the coming decades.