Deal sizes remain healthy even as number of VC deals plummets

The number of VC deals dropped considerably in Europe, falling from 2,419 deals in Q4’23 to 1,798 deals in Q1’24. This decline was particularly noticeable at later deal stages, with the number of Series D+ deals in the region dropping to just eleven. While deal volume was very subdued, deal sizes remained quite healthy as VC investors focused their funds on the most promising startups. The geographic diversity of VC investments also held strong during the quarter, with eight jurisdictions in the region attracting at least one $100 million+ funding round in Q1’24, including Sweden, the Netherlands, France, Germany, the UK, Spain, Israel, and Italy.

Cleantech biggest winner in Europe

While AI attracted the largest share of investment globally, cleantech investment accounted for many of Europe’s largest deals in Q1’23, including raises by Sweden-based H2 Green Steel ($5.2 billion) and Alternative Energy Equipment ($159 million), Germany-based Sunfire ($233 million), France-based Electra ($334 million), and Germany-based Ineratec ($129 million). ESG more broadly also has continued to attract attention from VC investors, driven in part by regulatory pressures. During Q1’24, a majority of EU member states agreed to the Corporate Sustainability Due Diligence Directive (CSDDD). Once fully passed, the directive will require large companies operating in the EU to audit their supply chains for ESG related concerns, including adherence to human rights and environmental protection requirements.

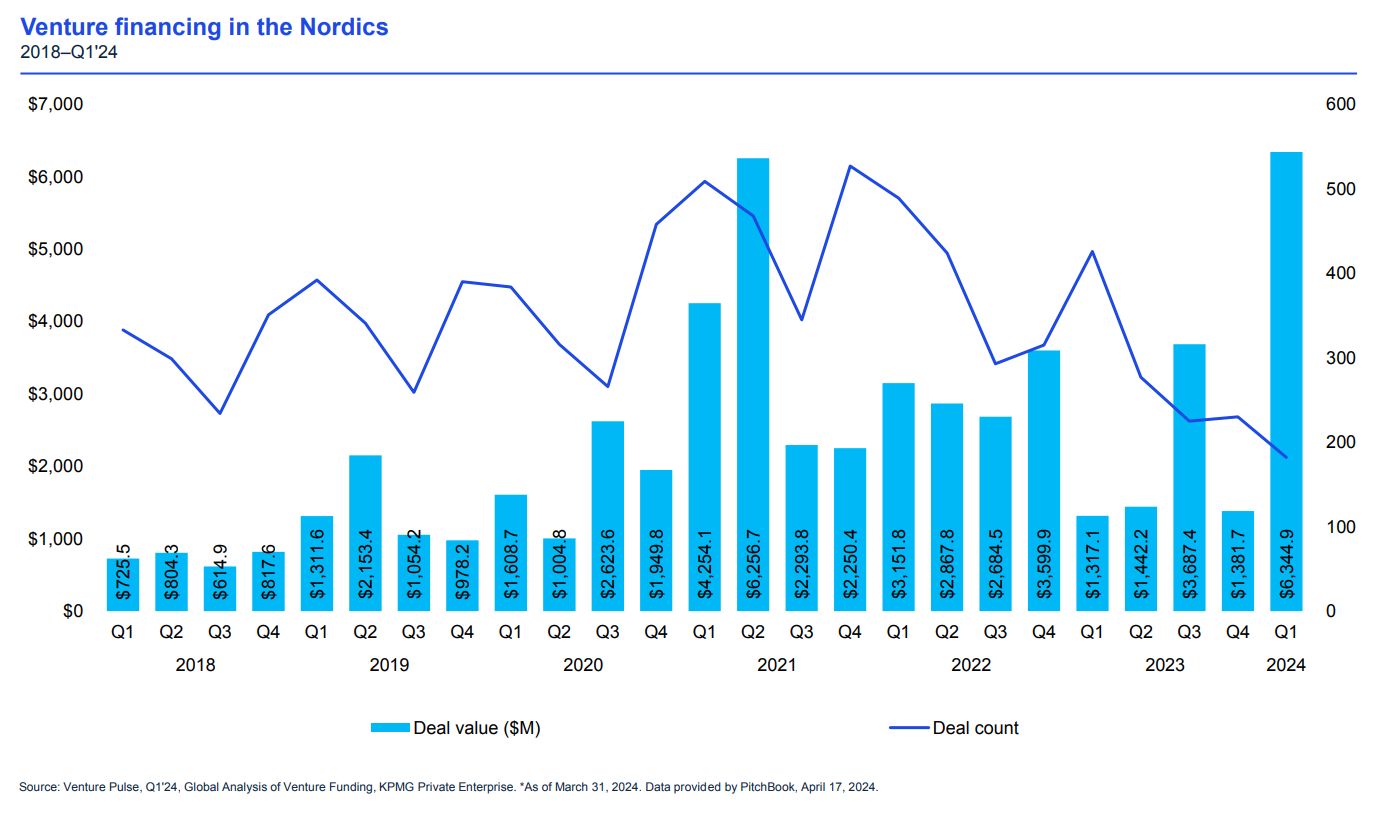

Despite $5.2 billion H2 Green Steel deal, tough market for late-stage startups in Nordic region

VC investment in the Nordic region surged in Q1’24, driven primarily by the $5.2 billion raise by clean infrastructure company H2 Green Steel in Sweden. The cleantech sector attracted the largest during Q1’24. In addition to the H2 Green Steel raise, Alternative Energy Equipment raised $129 million. While early-stage startups continue to attract a healthy level of investment in the region, companies looking to raise Series A-C funding rounds found it more challenging, particularly those in capital intensive sectors may struggle to find a lead investor for their rounds in the competition of scarce international funding.

Trends to watch for in Q2’24

Heading into Q2’24, VC investors in Europe are expected to remain very cautious as they continue to assess how ongoing macroeconomic challenges and geopolitical issues could unfold, including uncertainties related to upcoming elections in the US and Europe. VC investment in cleantech and ESG reporting is expected to remain strong given the increasing regulatory requirements in the space. Defense technologies are also expected to continue to grow on the radar of VC investors in the region. Interest in crypto has also started to rebound, which could result in an uptick in investment over the next quarter.

VC investors in Europe will likely be watching the US IPO market very closely in Q2’24 to see whether it opens up; if it does, it could have a follow-on effect on IPO and VC investment activity in Europe.

Bolstered by the $5,2 billion ($0,3 b equity, $0,3 b grants, $4,6 b debt) raise by H2 Green Steel the funding raised in the Nordics had its all-time high quarter. Looking past the H2 Green Steel deal the market was at pre-covid levels highlighting outlier years of 2021-22 and the oversupply of capital. The valuations in the US public markets have started to bounce back a bit and in general there's also more IPO activity in Europe compared to the Nordics. If we start to see successful exits there, it will likely start boosting the later-stage VC environment here as well. Until then, later-stage investment levels may remain somewhat subdued.

Investment reaches $17.9 billion invested on 1798 deals

Median deal size rises at all levels

Fundraising remains sluggish – reaching only $5 billion in Q1’24

UK sees slow start to the year

Down-rounds decrease

Top 10 deals spread among 7 countries