Why is materiality material?

With recent updates to regulatory and voluntary sustainability standards, materiality and well-known practices to apply it are on the move. For years, companies prioritized sustainability topics based on business significance and importance to stakeholder decision-making – a process known as a materiality assessment. Matrices were preferred over lists and an increasing number of companies started to interview external stakeholders, complementing their understanding of why a topic is societally relevant.

However, both regulatory and voluntary sustainability standard-setters have now either implemented or proposed significant changes to these traditional single materiality assessments. ‘Double materiality’ is making waves and our understanding of what counts as a material sustainability topic and how it should be determined are in flux.

When to report on double materiality?

The intention of double materiality is to broaden our understanding about how ESG (environmental, social, and governance) matters impact companies’ enterprise value creation (financial materiality) and how companies impact the world we live in (impact materiality). In sustainability jargon, it combines the notions of SASB and GRI on what warrants a material sustainability topic to give strategic direction, focus company resources, and report to stakeholders.

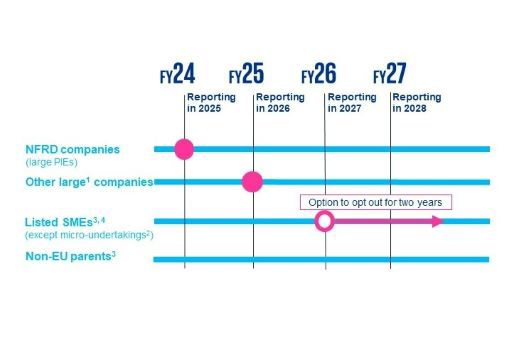

In the Nordics, and more widely within the EU, the double materiality requirement applies to companies already subject to NFRD (Non-Financial Reporting Directive) from financial year 2024 onwards according to draft CSRD’s (Corporate Sustainability Reporting Directive’s) ESRSs (European Sustainability Reporting Standards). Other large companies not presently subject to NFRD are expected to report on double materiality starting 2025 and listed SMEs, small and non-complex credit institutions and captive insurance undertakings starting 2026. However, practical guidance on how to apply double materiality is still pending at EU-level.

When and to whom would the ESRSs apply?

Of the voluntary reporting standards, GRI has given guidance in its updated Universal Standards on how to assess the significance of impacts to the economy, environment, and people, including impacts on their human rights (impact materiality) in line with the upcoming requirements. Companies reporting with reference to or in accordance with GRI must apply the Universal Standards in all reports published on or after 1 January 2023, whereas companies disclosing via SASB Standards need to wait and see whether IFRS Foundation will propose changes to the standards’ definition of materiality.

Different regulations and standards’ definitions of materiality

| Organisation | Definition of materiality |

| ESRS 1 (Exposure draft, 2022) | “Double materiality is a concept which provides criteria for the determination of whether a sustainability matter has to be included in the undertaking’s sustainability report. Double materiality is the union (in mathematical terms, i.e., union of two sets, not intersection) of impact materiality and financial materiality. A sustainability matter meets therefore the criteria of double materiality if it is material from either the impact perspective or the financial perspective or both perspectives.”1 |

| GRI (2016) | “-- reflect a reporting organisation’s significant economic, environmental and social impacts; or that substantively influence the assessments and decisions of stakeholders. -- In sustainability reporting, materiality is the principle that determines which relevant topics are sufficiently important that it is essential to report on them. Not all material topics are of equal importance, and the emphasis within a report is expected to reflect their relative priority."2 |

| GRI (2021) | “-- topics that represent the organization’s most significant impacts on the economy, environment, and people, including impacts on their human rights.”3 |

| Sustainability Accounting Standards Board (SASB) |

“-- sustainability disclosure topics that are reasonably likely to significantly impact the financial condition, operating performance, or risk profile of the [--] company.”4 |

1https://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FSiteAssets%2FED_ESRS_1.pdf

2https://www.globalreporting.org/standards/media/1036/gri-101-foundation-2016.pdf

3https://globalreporting.org/pdf.ashx?id=12453&page=7

4https://help.sasb.org/hc/en-us/articles/360060351771-How-does-SASB-s-definition-of-materiality-compare-to-that-of-other-disclosure-frameworks-

Why should your company assess its sustainability impacts now?

Materiality assessment enables a strategic approach and is a needed tool for companies identifying and managing their sustainability impacts. Although we see that it will take time for good practices related to double materiality processes to develop, we find that it is crucial that companies start assessing their impacts as soon as possible to be able to meet the reporting expectations and regulatory requirements in time.

Strategic sustainability management and reporting are ongoing processes that need to be planned, executed, and implemented with care. They cannot be rushed overnight because sustainability is not a one-size-fits-all exercise – aspects such as business and value chain operations, geographical presence, and stakeholder activity can tilt scales easily in one direction or the other.

Also, looking at the most impactful sustainability topics holistically can unearth opportunities, challenges and risks worth acting on as well as lead sustainability strategies, measurement, and disclosure on a path of impact. The pressing challenges of our time, such as climate change adaptation and social inequalities, cannot be solved without companies ramping up positive impacts and reducing negative ones.

Similarly, turning a blind eye to which sustainability impacts create or erode enterprise value is equivalent to throwing away critical resources of time, money and effort. The time for impact is now and double materiality is here to guide you on an impactful path.

What’s your plan for applying materiality in your business?

Contact us

Contact our professionals to discuss how we can help you to evaluate your material impacts and create a more impactful future together.

Kirsi Saaristo

Advisory Manager, Corporate Sustainability & Sustainable Finance

+358405170051

firstname.lastname@kpmg.fi